Detail guide on every question you have on filing of Income tax returns in 2016

Here we are going to reply all question, doubt and queries related to filing of income tax return. We have tried to answer almost all issues still you can ask your queries via comments or via email at shaifaly.ca@gmail.com

Q-1 How I can file and verify my return offline and online ?

There are 4 ways to file your income tax return you can file your return either

By filling in paper form and submitting it in income tax department manually or

By filling it electronically (HTML file generated via Utility) under digital signature or

By uploading data online (HTML file generated via Utility) and the verify ITR V electronically or

By uploading data online (HTML file generated via Utility) and then verify it by sending signed copy of ITV to Bangalore

Q-2 How to determine if I am required to file ITR online?

As per the provisions of Income tax some assesse are required to file their return in online mode only. They can’t file it in paper form and are mandatorily required to file online Income tax return. Following taxpayers shall file their return of income only through e-filing mode:

- From the assessment year 2015-16 an individual is required to file Income tax return online in case:

- They have any amount of refund claim.

- Their total income is more than Rs. 500,000.

- They are required to file the Income tax return electronically but they may file it with Digital signature or by using electronic verification code.

- An Individual whose age is 80 years or more is exempted from filing their Income tax return in electronic form.

- Every company shall furnish the return of income electronically under digital signature. In other words, for corporate taxpayer e-filing with digital signature is mandatory.

- A firm or an individual or a Hindu Undivided Family (HUF) whose books of account are required to be audited under section 44AB shall furnish the return of income electronically under digital signature. In other words, in such a case, e-filing with digital signature is mandatory.

- A resident assessee having any assets (including financial interest in any entity) located outside India or signing authority in any account located outside India or income from any source outside India shall furnish the return of income electronically with or without digital signature or by using electronic verification code.

- Taxpayers claiming relief under section 90, 90Aor 91 shall furnish the return of income electronically with or without digital signature or by using electronic verification code.

- A person who is required to file ITR – 5 shall file the same electronically with or without digital signature. However, a firm liable to get its accounts audited under section 44AB shall furnish the return electronically under digital signature.

- A taxpayer who is required to furnish a report of audit under sections 10(23C)(iv), 10(23C)(v), 10(23C)(vi), 10(23C)via), 10A, 10AA, 12A(1)(b), 44AB, 44DA, 50B,80-IA, 80-IB, 80-IC, 80-ID, 80JJAA, 80LA, 92E, 115JBor 115VW or to give a notice under section 11(2)(a) shall furnish the return electronically.

- Return Form ITR- 3 is to furnish electronically in the following modes:

- by furnishing the return electronically under digital signature;

- by transmitting the data in the return electronically under electronic verification code

- by transmitting the data in the return electronically and thereafter submitting the verification of the return in Return Form ITR-V

- Return Form ITR-4 is to be furnish electronically in the following modes:

- by furnishing the return electronically under digital signature;

- ) by transmitting the data in the return electronically under electronic verification code

- by transmitting the data in the return electronically and thereafter submitting the verification of the return in Return Form ITR-V

Related Topic:

Section 154 of Customs Act:Incorrect filing of Bill of Entry

However, where the books of accounts are required to be audited under section 44AB, the return is required to be furnished in the manner provided at (i) i.e. e-filing with digital signature.

- Return Form ITR – 7 is to be furnished electronically in the following modes :

- By furnishing the return electronically under digital signature;

- By transmitting the data in the return electronically under electronic verification code

- By transmitting the data in the return electronically and thereafter submitting the verification of the return in Return Form ITR-V

However, a political party shall compulsorily furnish the return in the manner mentioned at (i) above. Where the Return Form is furnished in the manner mentioned at (iii), the assessee should print out two copies of Form ITR-V. One copy of ITR-V, duly signed by the assessee, has to be sent by ordinary post to Post Bag No. 1, Electronic City Office, Bangalore-560100 (Karnataka). The other copy may be retained by the assessee for his record.

Q-3 How to find out the appropriate form of Income Tax Return I need to file?

ITR -1 or Sahaj

There are different ITR forms for different assesse. Before filing your Income tax return you are required to decide the appropriate form for filing return. Let us discuss all the forms one by one.

ITR:1 or Sahaj:

First Income tax return form is ITR 1 also called Sahaj. This form can be used by following Assessee

- Sahaj can be used only by individuals. Other entities like Company, HUF, partnership etc can’t use this form

- Sahaj can be used only in case individual assesse total income have any or all of the following income

- Income from Salary or pension; or

- Income from onehouse property; or

- Income from other sources

But in following cases ITR 1 can’t be used even by an individual.

- When his/her total income include income from more than one house property.

- In case when income of another person like minor child, spouse is required to be clubbed with the income of individual assesse then those clubbed incomeshould also be under the same headse salary/pension, income of house property, income from other source(other than lottery and income for race horses)

- When his/her total income includeincome from 1) Winning of lottery or 2) Income from race horses or both.

- When his/her total income include income to be chargeable to tax under the head income from capital gains.

- When his/her total income include agriculture incomeof more than Rs.5000.

- When his/her total income include income from Profits and gains from business or professionin simple words any business income.

- When his/her total income include lossfrom the head income from other sources.

- Who claim relief u/s 90(Double taxation relief when Double taxation avoidance agreement exists) or u/s 91(Double taxation relief when Double taxation avoidance agreement (DTAA) doesn’t exist.)

- Any resident individual have any assets including financial assets located outside India.

- Any resident individual having signing authorityfor any account located outside India.

- Any resident individual having any incomefrom any sourceoutside India.

Who can file their ITR in form ITR-2A

Form ITR-2A

- ITR 2A can be used by individuals as well as an HUF.

- ITR 2A can be used for income from Salary/pension, income from house property and income from other sources.

- ITR 2A can be used for income of winning from lottery and income from race horses.

- In case assesse is liable for clubbing of income of another person in above categories ITR 2A can be used.

- But ITR 2A can’t be used in case of income from Capital gains, income from business or profession.

- ITR 2A can’t be use to claim relief of section 90,90A or 91.

- ITR2A can’t be use in case assesse is having any income from outside India, or any asset (including financial assets) and in case assesse is having signing authority in any account outside India.

When we can use form ITR 2 to file income tax return

Form ITR 2 can be used in following cases

- When assesse have income from salary/pension, house property(any number or house property) , income from capital gains, Income from other sources including income from lottery and from horse races

- When income of another person is also required to be clubbed in the income of assesse then if that income falls in above heads then also ITR 2 can be used.

- ITR 2 can’t be used by a person having income from profits and gains from business or profession.

When to use form ITR 3 to file income tax return

- Form ITR 3 is to be used by an individual or HUF who are partner in any partnership firm. Their taxable income under profits or gains of business or profession include only the salary, commission, interest, bonus or partner’s remuneration from the firm plus share from partnership firm (which is exempt).

- In case they have any other income under profit or gains from business or professions form ITR 3 will not applicable.

- In case they have only exempt income of share from partnership firm they will use form ITR 3 (not2)

- In other words partners of partnership firms will use form ITR 3 but their income under Profits and gains from business or profession should have only receipts from partnership.

- In case they have their own proprietorship also then ITR 3 will not applicable.

When to use form ITR 4S (Sugam) to file income tax return

- ITR 4S also known as Sugam is used by assesse whose income is calculated under presumptive taxation scheme.

- ITR 4S can be used by Individual/HUF/Partnership firm (but not by LLP)

- ITR 4S can be used by assesse having income computed under the provisions of section 44AD(presumptive taxation where income for business is taken as 8% of gross turnover and income of profession is taken as 50% of total gross receipts) and 44AE (Presumptive taxation of transporters), income from salary or pension, income from house property (excluding the carry forward losses),income from other sources(excluding income from lottery and race horses)

- ITR4S can’t be used by assesse having income of house property from more than one house.

- Assesse having income from lottery or income from race horses.

- Assesse having income chargeable under the head income from capital gains.

- Assessee having agriculture income of more than Rs. 5000.

- Whose total income for the year includes income from profession as referred to in section 44AA(1).

- Whose total income for the year includes income from agency business or income in the nature of commission or brokerage

- Who claims relief undersection 90, 90Aand/or section 91

- Who is a resident and ordinarily resident and has any assets (including financial interest in any entity) located outside India or signing authority in any account located outside India

- Section 44AA gives an option to assesse who don’t want to avail benefit of presumptive taxation to pay tax on their calculated income if they maintain proper books of accounts. In case assesse opt to not to pay tax on presumptive basisbut maintain books of accounts and pay tax on calculated income then form ITR4S will not be used for filing their return.

ITR 4:

ITR 4 is to be used by individual or HUF who are doing business or profession in proprietorship. Anyone except them can’t use this form

Form ITR-5 can be used by person other than individual/HUF and company. In other words form ITR -5 will be used by firm, LLP, AOP, BOI, Artificial juridical person, cooperative society and local authority.

Form ITR 6 can be used by a company to file their ITR but a company who claims exemption u/s 11(i.e. charitable or religious) can’t use form ITR -6

Form ITR-7 can be used by person need to file their ITR u/s 139(4A)(Trust inocme) , 139(4B)(income of political parties), 139(4C)(Scientific research) ,139(4D)(university/college, news agency etc.), 139(4E), 139(4F)

Q-4 Where I will be able to find the form I need to file?

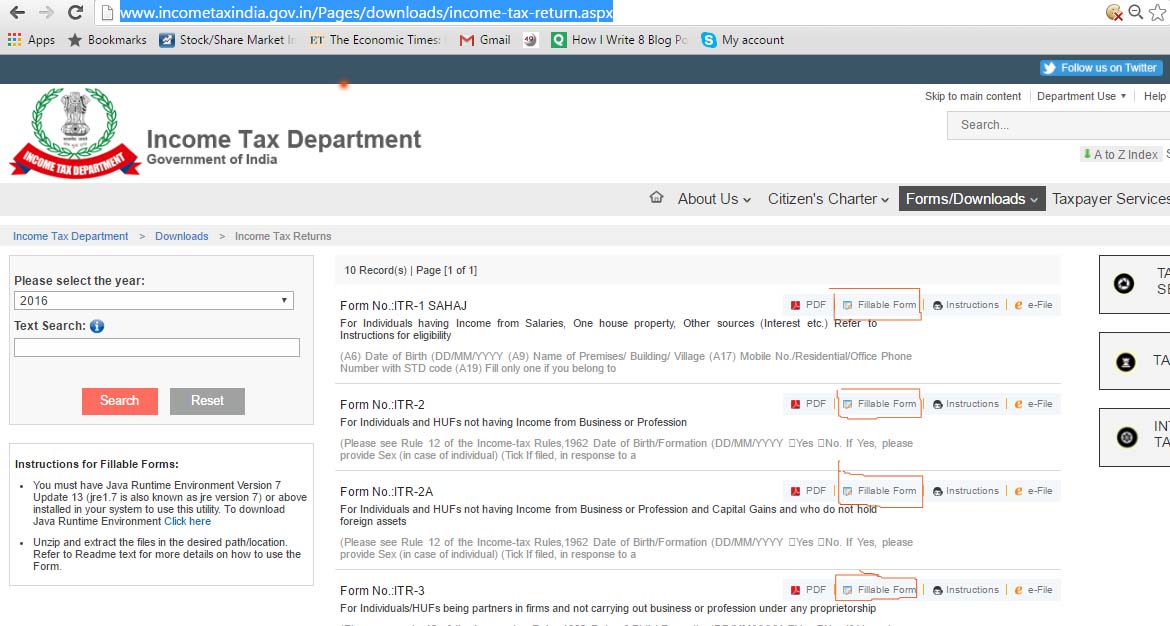

All return utilities are available at the website of Income tax India. You will be able to download the requisite forms from there. It will be in form of Excel utility. You can fill this excel utility easily and then check if it is correctly filled or not. You can also calculate the amount of tax or refund after filing the entire details. Following is the link of income tax department website providing the forms of all ITR.

http://www.incometaxindia.gov.in/Pages/downloads/income-tax-return.aspx

You will find this page after clicking on above link. Here you need to click on Fillable form (as outlined by brown color). A zip file will be downloaded, unzip it and you will find the utility. Now click on enable content in formula bar. Your utility is ready to use.

Q-5 Important information I need to fill in form?

Q-5 Important information I need to fill in form?

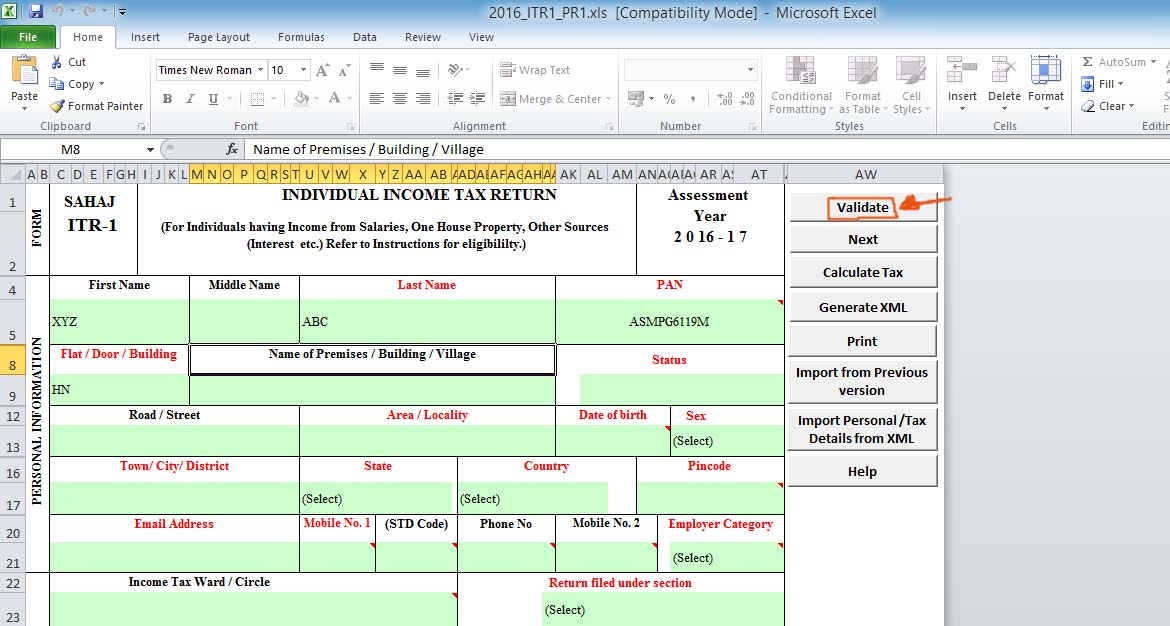

- You need to fill all of the details in your ITR form like name, address, PAN, date of birth.

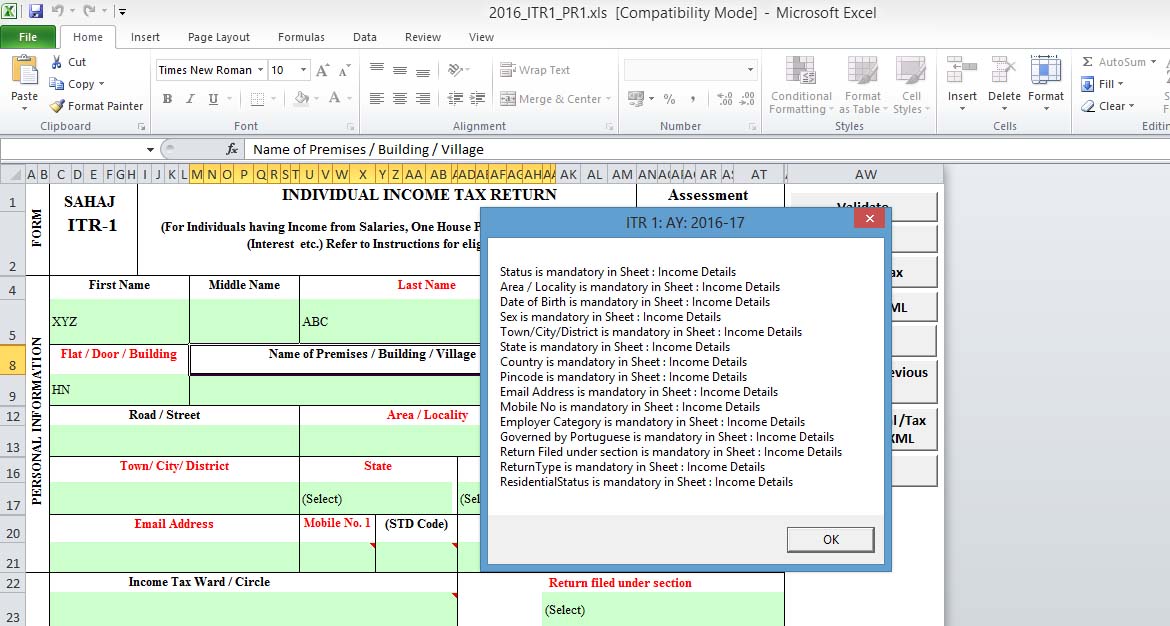

- Utility available of income tax department’s website is very easy to use and even if you skipped any important field it will show you the list of discrepancies. Click on validate after filing basic information.

A box with list of discrepancies will show up once you will click on validate.

When all of the fields will be properly filled it will show ‘sheet is ok’. Now you can proceed to calculate your taxes. Click on calculate taxes and it will calculate the final figure of tax payable or refund.

There is some information which is important to provide correctly. In most of the cases assesse have to suffer because of these mistakes while filing income tax return.

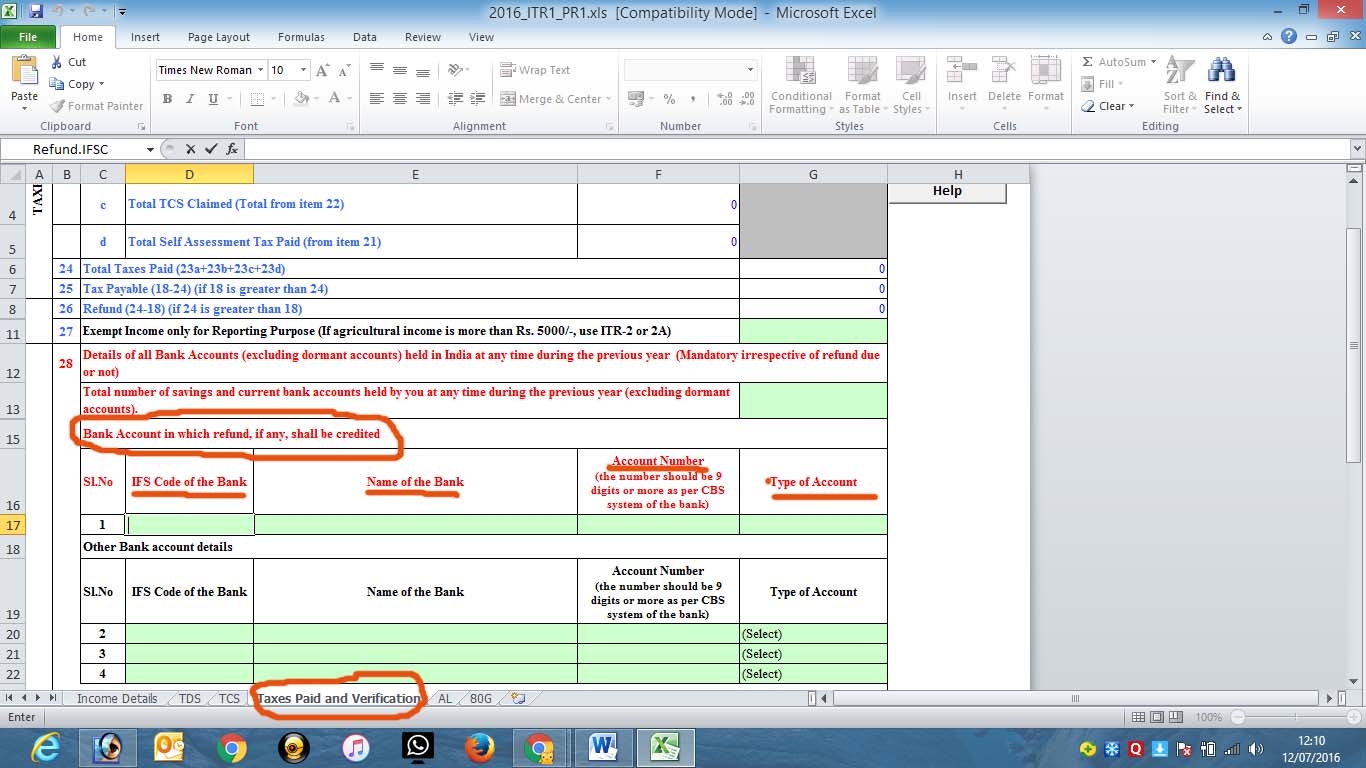

a) Bank account details: You need to fill details of your bank account. This information should be filled carefully specially in case of refund. If you will fill the wrong information your refund may be delayed. You can find this field in “taxes paid and verification”. See image below

- b) Address: It is important to fill your address correctly. When refund amount is more than Rs.50, 000 then instead of transferring it directly to your bank account, income tax department send cheaque of the amount at your address. If your address will not be correct you may have to face problem as cheque will be returned or may be delivered at incorrect address. This will delay your refund process and will waste your time and resources in follow up.

- c) TDS details: TDS details should be filled accurately. It is better to keep a print of your form 26AS and then fill the details. Before filing the Income Tax return checks if you have taken all the figures into account on which TDS has been deducted and deposited. If there is any income skipped then fill it. You also need to verify id TDS deducted on all of your receipts is appearing in your form 26AS, if any amount is missing then communicate with the concerned person and make sure that all amounts of TDS deducted from your receipts are duly deposited with correct information.

- d) PAN: Fill correct PAN while filing your details in ITR form. Incorrect PAN may cause delay in your assessment.

- e) Interest on savings account: Most of the time we forget to enter this figure as it is small and is exempt up to a limit. But recently Income tax department has asked all the tax payers to take it seriously and fill details of interest income on savings account, RD and FD’s while filing ITR.

- f) Foreign income: In case you have any foreign income, mention that income in your return. You may also be eligible for relief under DTAA if some taxes have been deducted in the country of origin.

Q-6 Do I need to send the hard copies of my documents supporting the information in my return?

Income tax return forms are paperless forms. You don’t need to send any document or proof either in hard copy or soft copy. It is advisable to maintain a file and keep the copies of all documents so that they can be referred in future. You will have to produce them in case of scrutiny.

In cases where audit report is required to be filed along with return soft copies of documents will be submitted as attachment.

Q-7 If I need to file Income Tax Return even if I have loss?

If you want to carry forward your losses you will have to file your ITR that too before due date as if you will file return after due date you won’t be able to carry forward your losses and will have to pay tax on future profits without adjustment of losses.

Q-8 If I need to file return even if taxes payable by me are already paid via advance tax and TDS.

TDS paid on your behalf will only be adjusted against your tax payable when there will be assessment of your income. Assessment will take place only after you will file the return.

Consultant