SABKA VISHWAS (Legacy Dispute Resolution) Scheme, 2019

A voluntary dispute resolution scheme called as Sabka Vishwas (Legacy Dispute Resolution) Scheme 2019 has been introduced by the Government for resolution of the Legacy disputes under Central Excise, Service Tax etc.

(Incorporating clarification and procedure vide Circular 1071/4/2019-CX8. dated 27/08/2019)

APPLICATION OF SCHEME TO INDIRECT TAX ENACTMENTS

- The Scheme has now been notified and will be operationalized from 1st September 2019. The Scheme would continue till 31st December 2019.

- The most attractive aspect of the Scheme is that it provides substantial relief in the tax dues for all categories of cases as well as full waiver of interest, fine, penalty, In all these cases, there would be no other liability of interest, fine or penalty. There is also a complete amnesty from prosecution.

- This Scheme shall be applicable to the following enactments,

(a) the Central Excise Act, 1944 or the Central Excise Tariff Act, 1985 or Chapter V of the Finance Act, 1994 (Service Tax) and the rules made thereunder;

(b) 26 other enactments –CESS like ; the Sugar Cess Act, 1982; the Tobacco Cess Act, 1975 , Jute Manufacturers Cess Act, 1983; (subsumed in GST)

(c) Any other enactment as may be notified.

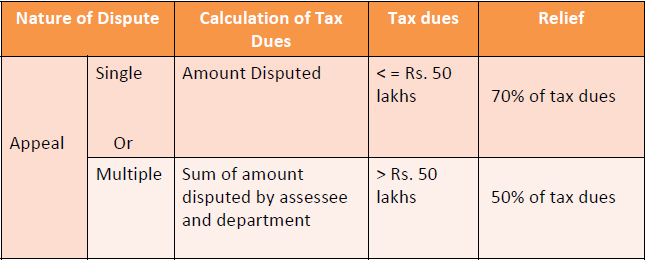

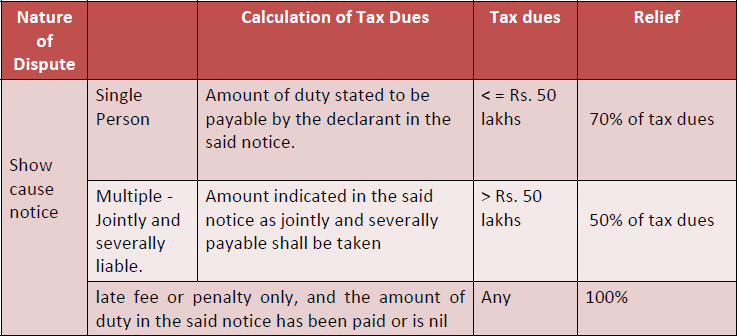

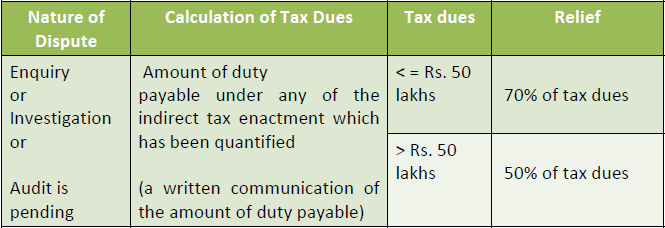

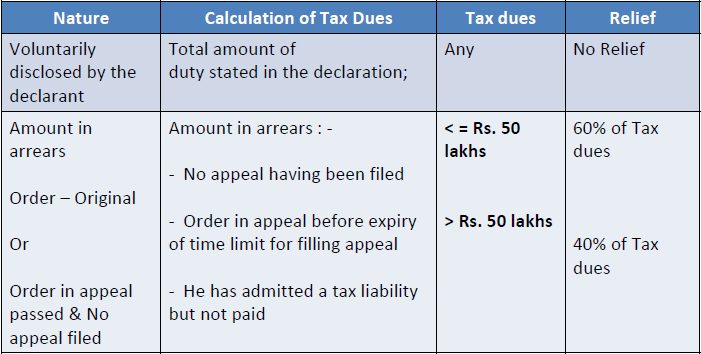

FOR THE PURPOSES OF THE SCHEME- “TAX DUES” & “RELIEF”

It is important to understand the calculation of “Tax Dues” , since relief under the scheme will be calculated on the “Tax Dues” – Let us understand the concept

“Amount payable” means the final amount payable by the declarant as determined by the designated committee and as indicated in the statement issued by it, in order to be eligible for the benefits under this Scheme and shall be calculated as the amount of tax dues less the tax relief;

(Hence no interest, late fee, and penalty payable in any of the case eligible for relief under scheme.)

Download the full ppt on SABKA VISHWAS (Legacy Dispute Resolution) Scheme, 2019, below:

IMPORTANT POINTS TO NOTE

- It may be noted, in this context, that the relevant stage of dispute or pendency thereof would be examined as of June 30, 2019 for eligibility under the Amnesty Scheme

- The relief calculated under sub-section (1) shall be subject to the condition that any amount paid as predeposit at any stage of appellate proceedings under the indirect tax enactment or as deposit during enquiry, investigation or audit, shall be deducted when issuing the statement indicating the amount payable by the declarant:

- Provided that if the amount of predeposit or deposit already paid by the declarant exceeds the amount payable by the declarant, as indicated in the statement issued by the designated committee, the declarant shall not be entitled to any refund.

- In certain matters, tax may have been paid by utilising the input credit, and the matter is under dispute. In such cases, the tax already paid through input credit shall be adjusted by the Designated Committee at the time of determination of the final amount payable under the Scheme.

- It is clarified that a declarant cannot opt to avail benefit of scheme in respect of selected matters. In other words. the declarant has to file a declaration for all the matters concerning duty liability covered under the show cause notice.

- Scope of discretion has been kept to the minimum by linking the relief under this scheme to the duty amount which is already known to both the Department and the taxpayer in the form of a show cause notice/order of determination or a written communication. The calculation of relief itself will be automated. Even in case of voluntary disclosure, no verification will be carried out by the Department.

INELIGIBLE PERSON

(a) who have filed an appeal before the appellate forum and such appeal has been heard finally on or before the 30th day of June, 2019;

(b) who have been convicted for any offence punishable under any provision of the indirect tax enactment for the matter for which he intends to file a declaration;

(c) who have been issued a show cause notice, under indirect tax enactment and the final hearing has taken place on or before the 30th day of June, 2019;

(d) who have been issued a show cause notice under indirect tax enactment for an erroneous refund or refund;

(e) who have been subjected to an enquiry or investigation or audit and the amount of duty involved in the said enquiry or investigation or audit has not been quantified on or before the 30th day of June, 2019; (Written communication must)

(f) a person making a voluntary disclosure,—

(i) after being subjected to any enquiry or investigation or audit; or

(ii) having filed a return under the indirect tax enactment, wherein he has indicated an amount of duty as payable, but has not paid it;

(g) who have filed an application in the Settlement Commission for settlement of a case;

(Exception: Application rejection by the Commission or abates due to order of the Commission not being passed within the prescribed time , any pending appeals, reference or writ petition filed against or any arrears emerging out of the orders of Settlement Commission are eligible for the scheme)

(h) persons seeking to make declarations with respect to excisable goods set forth in the Fourth Schedule to the Central Excise Act, 1944 (excisable products of tobacco or tobacco substitutes)

Important Clarification – Circular 1071/4/2019-CX8. dated 27/08/2019

- A declaration under this Scheme will not be a basis for assuming that the declarant has admitted the position, and no fresh show cause notice will be issued merely on that basis.

- The Scheme is not available to an applicant who has been issued a show cause notice relating to refund or erroneous refund. It has potential to lead to an interpretation that such persons will not be able to opt for the Scheme for any other dispute as well, since the restriction is on ‘the person’ in place of ‘the case’. It is clarified that the exception from eligibility is for ‘the case’ and not ‘the person’. In other words, if a person has been issued a show cause notice for a refund/erroneous refund and, at the same time, he also has other outstanding disputes which are covered under this Scheme, then, he will be eligible to file a declaration(s) for the other case(s). Same position will apply to persons covered under Sections 125(1)(a), (b), (c), (e) and (g).

PROCEDURAL ASPECTS

- A declaration shall be made in such electronic form as may be prescribed. It will be fully automated through www.cbic-gst.gov.in to ensure transparency , detailed procedure awaited.

- Designated committee shall verify the correctness of the declaration made by the declarant under section 124 in such manner as may be prescribed.

- There shall be two Designated Committees of two officers each in a Commissionerate to process the declarations received thereunder (for this purpose Audit Commissionerates are to be left out). The Designated Committees have been set up based on the amount of tax dues.

- If duty demanded is more than Rs. 50 lakhs, the same will fall under the purview of a Committee consisting of Principal Commissioner/Commissioner and Additional/Joint Commissioner. (it is, hereby, clarified that this duty demand is before applying the tax-relief.)

- The members of the Committee will be nominated by jurisdictional Principal Chief Commissioner/Chief Commissioner and Principal Director General/ Director General, DGGI, as the case may be.

- Designated committee shall issue in electronic form, estimate/statement, indicating the amount payable by the declarant. – When estimate of committee and declarant matched -60 days / not matched- 30 Days from the date of receipt of the said declaration.

- The entire process of filing of declaration to communication of Department’s decision and to payment gets completed within 90 days. This is important as there is no scope for extension of the time period for the sub-processes or the complete process.

- Designated committee shall give an opportunity of being heard to the declarant, if he so desires, before issuing the statement indicating the amount payable by the declarant. (One adjournment may be Granted)

- The declarant shall pay electronically through internet banking, the amount payable as indicated in the statement issued by the designated committee, within a period of thirty days from the date of issue of such statement.

- Where the declarant has filed an appeal or reference or a reply to the show cause notice against any order or notice giving rise to the tax dues, before the appellate forum (upto Tribunal), other than the Supreme Court or the High Court, then, notwithstanding anything contained in any other provisions of any law for the time being in force, such appeal or reference or reply shall be deemed to have been withdrawn.

- The declarant shall file an application before such High Court or the Supreme Court for withdrawing such writ petition, appeal or reference and after withdrawal of such writ petition, appeal or reference with the leave of the Court, he shall furnish proof of such withdrawal to the designated committee.

EFFECT OF CERTIFICATE OF DISCHARGE

Discharge certificate issued with respect to the amount payable under this Scheme shall be conclusive as to the matter and time period stated therein, and–

(a) the declarant shall not be liable to pay any further duty, interest, or penalty with respect to the matter and time period covered in the declaration;

(b) the declarant shall not be liable to be prosecuted under the indirect tax enactment with respect to the matter and time period covered in the declaration;

(c) no matter and time period covered by such declaration shall be reopened in any other proceeding under the indirect tax enactment.

Issue of the discharge certificate with respect to a matter for a time period shall not

Preclude the issue of a show cause notice

– Same matter for a subsequent time period

– Different matter for the same time period

– any material particular furnished subsequently found to be false, within a period of one year of issue of the discharge certificate, presumed declaration was never made.

RESTRICTIONS OF SCHEME

(1) Any amount paid under this Scheme,—

(a) shall not be paid through the input tax credit account under the indirect tax enactment or any other Act;

(b) shall not be refundable under any circumstances;

(c) shall not, under the indirect tax enactment or under any other Act,—

(i) be taken as input tax credit; or

(ii) entitle any person to take input tax credit, as a recipient, of the excisable goods or taxable services, with respect to the matter and time period covered in the declaration.

(2) In case any predeposit or other deposit already paid exceeds the amount payable as indicated in the statement of the designated committee, the difference shall not be refunded.

GSTIND GLOBAL SOLUTIONS LLP - LETS UNDERSTAND GST.