FAQ’s on rectification of orders in GST

Rectification may be misjudged with the rectification of returns. So first thing I would like to clarify is that here we are going to discuss about the rectification of orders already passed by the GST department.

1- What are the provisions of rectification of orders in GST?

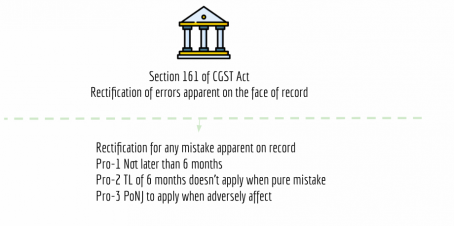

Ans- Section 161 of CGST Act covers the provisions related to the rectification in GST. The provision as given is law is reproduced here.

Q-2 Can we file rectification for dispute with the authorities?

Ans- No, the purpose of rectification is to rectify the “errors apparent on the record”. It is not a mechanism to settle any dispute or to adjudicate.

e.g.- A got an order where the amount of demand was written as Rs. 647000 in place or Rs. 4,67000. Although as per calculation the amount was 4,67000 but the officer did a typing mistake and write it incorrectly. In this case one can go for rectification.

On the other hand where the officer rejected the ITC as it was not visible in 2A , you cant go to rectification but should go for appeal.

Q-3 What is the time limit for rectification?

Ans-

The rectification shall be applied within a period of three months from the date of issue of such decision or order or notice or certificate or any other document, as the case may be:

Q-4 What is the time limit to pass a rectification order?

Ans- As per the provisions of section 161 of CGST Act-

Rectification shall be done within a period of six months from the date of issue of such decision or order or notice or certificate or any other document:

Provided further that the said period of six months shall not apply in such cases where the rectification is purely in the nature of correction of a clerical or arithmetical error, arising from any accidental slip or omission.

Q-5 Whether the time limit of appeal will merge with the time limit of rectification?

Ans- The time limit of appeal cant be extended in case of rectification. If the order of rectification is received within the time limit of appeal, one can go for appeal. But if it is received later no appeal cant be filed. Although there were some judgments in easllier law allowing the time. But they will have only referrer value in GST.

Q-6 What is difference between an appeal and rectification?

Ans-

1- Appeal is for difference of facts or interpretation of law whereas the rectification is only for mistakes apparent on record. Where there is no dispute related to the facts or law.

2- They have different time limits.

3- In case of appeal you need to deposit the amount of pre deposit. In case of rectification no such depositis required.

CA