Original Copy GST AAR of Pew Engineering Pvt Ltd

Original Copy GST AAR of Pew Engineering Pvt Ltd

In the GST AAR Pew Engineering Pvt Ltd, the applicant has raised the query regarding, whether the Principal Supply will be the supply of the Twin Pipe Air Brake Systems or the supply of services of fitting these goods to the wagons, and what should be the appropriate classification of the supply and rate of tax. Following is the GST AAR of Pew Engineering Pvt Ltd.

Order:

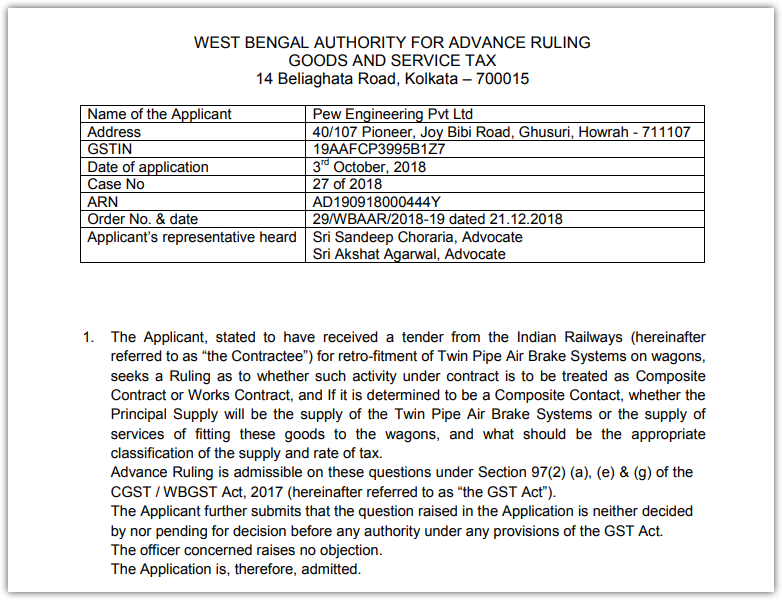

1. The Applicant, stated to have received a tender from the Indian Railways (hereinafter referred to as “the Contractee”) for retro-fitment of Twin Pipe Air Brake Systems on wagons, seeks a Ruling as to whether such activity under contract is to be treated as Composite Contractor Works Contract, and If it is determined to be a Composite Contact, whether the Principal Supply will be the supply of the Twin Pipe Air Brake Systems or the supply of services of fitting these goods to the wagons, and what should be the appropriate classification of the supply and rate of tax. Advance Ruling is admissible on these questions under Section 97(2) (a), (e) & (g) of the CGST / WBGST Act, 2017 (hereinafter referred to as “the GST Act”).

The Applicant further submits that the question raised in the Application is neither decided by nor pending for decision before any authority under any provisions of the GST Act.

The officer concerned raises no objection.

The Application is, therefore, admitted.

2. The Applicant submits that the scope of work conforms to the requirements of the Railway Technical Bulletin. The materials will be supplied by the Applicant as per the RDSO specifications and shall be subject to inspection by RDSO / RITES

The Actual fitment and testing shall be made at the wagon workshop with manpower, tools, spares, and machinery provided by the Applicant.

The Contractee will, however, provide some equipment and electricity, free of cost. The work shall be executed as per specifications/drawings of the RDSO.

Nominated officers of the Contractee shall do an on-site inspection of fabrication and assembly at various stages of the work in progress and also the final inspection of the complete wagon before issuance of the completion/inspection certificate for each wagon. The Applicant shall provide the necessary facilities for the inspection.

Scrap generated during fabrication and assembly work shall be retained by the Contractee.

Download the GST AAR of Pew Engineering Private Limited, by the clicking the below image:

3. The Applicant argues that the contract is a single indivisible contract for a Composite Supply, where the supply of goods (i.e. the twin pipe air brake systems) is the Principal Supply constituting about 90% of the contract value, and, hence, should be treated as the predominant element of the supply.

The service of fitting the brake to the wagon, the Applicant submits, is ancillary to the supply of these goods.

4. The contract is for retro-fitment of twin pipe air brake system on wagons. Retro-fitment of twin pipe air brake system involves the supply of goods, the air brake system, and supply of service for fabrication and assembling of the air brake system on the wagons. The term retro-fitment indicates the wagons that have otherwise been in operation are being upgraded by the fitment of the twin pipe air brake system. Section 2(119) of the GST Act defines “works contract” as “a contract for building, construction, fabrication, completion, erection, installation, fitting out, improvement, modification, repair, maintenance, renovation, alteration or commissioning of any immovable property wherein transfer of property in goods (whether as goods or in some other form) is involved in the execution of such contract”

Since clearly, Twin Pipe Air Brake Systems are not immovable property, any contract involving the supply and installation of the same cannot be covered under Section 2(119) of the GST Act, as “works contract”

5. Again, the Contractee makes payment for completed wagons on a monthly basis. Failure to meet the monthly target for turning out completed wagons is liable to attract penalty. No payment is made separately for the supply of goods.

Also, the provision for on account payment based on the progress of work indicates that the supply of goods is inseparably linked with the supply of service. Mere delivery of the Twin Pipe Air Brake Systems is not sufficient to discharge of a contractual obligation. Work is measured based on its assembling and fitting on the wagon. In fact, the contract is not only for the supply of the air brake system but also for its retro-fitment. It is, therefore, evident that the two supplies, as far as the terms of this contract, are naturally bundled in the ordinary course of business.

6. In the context of the contract, the supply of the service of fitting the Twin Pipe Air Brake Systems to the wagon cannot be made unless the goods have already been supplied. The supply of services of the fitting is, therefore, dependent upon and ancillary to supply of the Twin Pipe Air Brake Systems.

Predominant supply is, therefore, of the Twin Pipe Air Brake Systems, which constitutes the essence of the contract.

7. Section 2(30) of the GST Act defines “composite supply” as “a supply made by a taxable person to a recipient consisting of two or more taxable supplies of goods or services or both, or any combination thereof, which are naturally bundled and supplied in conjunction with each other in the ordinary course of business, one of which is a principal supply”

Again, Section 2(90) of the GST Act defines “principal supply” as “the supply of goods or services which constitutes the predominant element of a composite supply and to which any other supply forming part of that composite supply is ancillary”. It is, therefore, clear from the discussion above that the contract referred to by the Applicant is that of a composite supply within the meaning of Section 2(30), where the Twin Pipe Air Brake Systems are the Principal Supply as defined under Section 2(90) Ibid. The entire contract value is, therefore, taxable at the rate applicable for the supply of Twin Pipe Air Brake Systems.

8. Twin Pipe Air Brake System is classifiable under Tariff Head 8607 21 00 [Parts of Railway…Air Brakes and part thereof] which is taxable @ 5% under Serial No. 241 of Schedule I of Notification No. 01/2017 – CT (Rate) dated 28/06/2017 with no benefit of refund of the unutilized input tax credit (as per TRU Clarification issued under F.No.354/1/2018-TRU dated 25/01/2018).

In view of the foregoing, we rule as under

RULING:

The Applicant’s contract for retro-fitment of Twin Pipe Air Brake System on Railway Wagons is to be treated as Composite Supply, where the Twin Pipe Air Brake System is the Principal Supply.

Twin Pipe Air Brake System is classifiable under Tariff Head 8607 21 00 and is taxable @ 5% [in terms of Serial No. 241 of Schedule I of Notification No. 01/2017 – CT (Rate) dated 28/06/2017] with no refund of the unutilized input tax credit [as clarified in TRU Clarification issued under F.No.354/1/2018-TRU dated 25/01/2018].

This Ruling is valid subject to the provisions under Section 103(2) until and unless declared void under Section 104(1) of the GST Act.

Source: http://www.wbcomtax.nic.in/GST/GST_Advance_Ruling/29WBAAR2018-19_20181221.pdf

Consultant