Original copy of GST AAR of M/s. Guru Cold Storage Pvt Ltd

Original copy of GST AAR of M/s. Guru Cold Storage Pvt Ltd

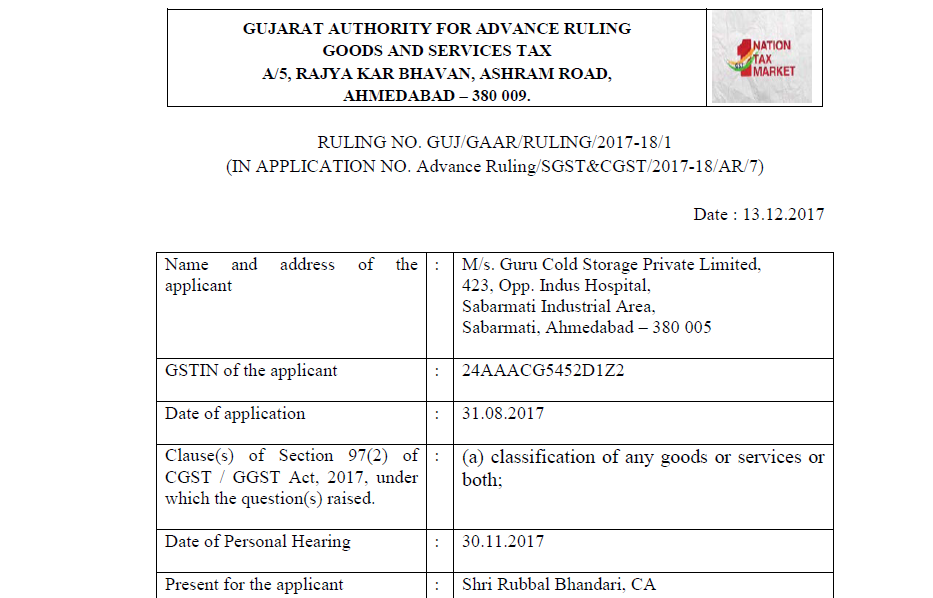

In the GST AAR of M/s. Guru Cold Storage Pvt Ltd, the applicant has raised the query regarding the classification of goods according to Notification No. 12/2017-CTR. Following is the GST AAR of M/s. Guru Cold Storage Pvt Ltd:

Order:

The applicant, M/s. Guru Cold Storage Pvt. Ltd., has referred to notification No.11/2017-Central Tax (Rate) dated 28.06.2017, which inter-alia provides rate of tax as NIL for ‘support services to agriculture, forestry, fishing, animal husbandry’, and submitted that in their opinion, ‘Agricultural Produce’ includes all cereals, pulses, fruits, nuts and vegetables, spices, copra, sugar cane, jaggery, raw vegetables fibers such as cotton, flax, jute, indigo, unmanufactured tobacco, betel leaves, tendu leaves, rice, coffee and tea but does not include manufactured products such as sugar, edible oils, processed food and processed tobacco, and intra-state support services to agricultural produce by way of loading, unloading, packing, storage or warehousing of agriculture produce is chargeable at NIL rate.

It is further submitted that as per their understanding of the provisions of the CGST Act and the SGST Act (Gujarat), there is no tax on agricultural produce unless the goods are branded with the registered trademark. Thus, the services related to storage of the goods mentioned above, either in bulk packing or small or retail packing with or without name or brand name, which is not registered under the Trade Mark Act, 1999 where no further processing is done or such processing is done which does not alter its essential characteristics but makes it marketable for primary market shall be charged at NIL rate as the same has not been branded with a registered trademark.

2. The applicant has raised the following question for advance ruling :-

“Whether all cereals, pulses, spices, copra, jaggery (Gur), groundnuts (with or without shell), groundnut seeds, turmeric dried and ginger dried (soonth), cashew, almond, kismis, jardalu, anjeer (fig), date, ambli foal are covered under the definition of ‘Agriculture Produce’ as defined under Notification No. 11/2017-Central Tax (Rate) dated 28.06.2017.

If the answer to the above point is affirmative, then whether the taxability of goods mentioned above point changes if they are received for storage either in bulk packing or small or retail packing with or without name or brand name which is not registered under the Trade Mark Act, 1999 where no further processing is done or such processing is done which does not alter its essential characteristics but makes its marketable for primary market.”

Download the GST AAR of M/s. Guru Cold Storage Pvt Ltd, by clicking the below image:

3. The Goods and Services Tax & Central Excise Commissionerate, Ahmedabad North submitted that the products mentioned by the applicant in his application are produce out of cultivation of plants but become marketable after some further processing which is generally done by the processor, not by a cultivators or producer, therefore all the above products do not cover under the definition of ‘Agricultural Produce’ as defined under the Notification No. 11/2017-Central Tax (Rate) dated 28.06.2017. It is also submitted that as all the above products are not covered under Notification No. 11/2017-Central Tax (Rate) dated 28.06.2017, the reply of point (b) of application is not relevant.

4. We have considered the submissions made by the applicant in their application for the advance ruling as well as at the time of the personal hearing on 30.11.2017. We have also considered the views of GST & Central Excise Commissionerate, Ahmedabad North.

5.1 The issue involved mainly pertains to Sl. No. 24 of Notification No. 11/2017-Central Tax (Rate) dated 28.06.2017 issued under the Central Goods and Services Tax Act, 2017 (hereinafter referred to as the ‘CGST Act, 2017’) and corresponding Notification issued under the Gujarat Goods and Services Tax Act, 2017 (hereinafter referred to as the ‘GGST Act, 2017’) or the Integrated Goods and Services Tax Act, 2017. The relevant part of Sl. No. 24 of the said Notification is reproduced below –

| Sl. No. | Chapter, Section or Heading | Description of Services | Rate (Percent.) | Condition |

| (1) | (2) | (3) | (4) | (5) |

| 24 | Heading 9986 |

i) Support services to agriculture, forestry, fishing, animal husbandry. Explanation. – “Support services to agriculture, forestry, fishing, animal husbandry” mean – (i) Services relating to cultivation of plants and rearing of all life forms of animals, except the rearing of horses, for food, fibre, fuel, raw material or other similar products or agricultural produce by way of— (a) ………; |

Nil | – |

5.2 Further, as per explanation (vii) under Para 4 of the said Notification –

(vii) “agricultural produce” means any produce out of cultivation of plants and rearing of all life forms of animals, except the rearing of horses, for food, fibre, fuel, raw material or other similar products, on which either no further processing is done or such processing is done as is usually done by a cultivator or producer which does not alter its essential characteristics but makes it marketable for primary market.”

5.3 Similarly, the GST rate for services relating to agricultural produce by way of loading, unloading, packing, storage or warehousing of agricultural produce is NIL as per Sl. No. 54 of Notification No. 12/2017-Central Tax (Rate) dated 28.06.2017 and corresponding Notification issued under GGST Act, 2017.

6.1 It is observed that ‘pulses (commonly known as ‘Dal’) are obtained after de-husking or splitting or both, which processes are usually not carried out by farmers or at farm level but are carried out by the pulse millers. Therefore, pulses (de-husked or split) are not agriculture produce. However, whole pulse grains such as whole gram, rajma etc. are covered in the definition of agricultural produce. Processing of sugarcane into jaggery changes its essential characteristics. Thus, jaggery is also not an agricultural produce. The processed dry-fruits (processed cashew nuts, almonds, raisin (kismis), apricot (jardalu), fig (anjeer), date etc.) fall outside the definition of agriculture produce given in the aforesaid Notification.

6.2 The processed spices, including processed turmeric and processed ginger fall outside the definition of agriculture produce. However, turmeric and ginger on which no further processing is done or such processing is done as is usually done by a cultivator or producer which does not alter its essential characteristics but makes it marketable for primary market would fall within the definition of agriculture produce.

6.3 In case of tamarind, the tamarind pod is cracked open, string (fibre) are removed and kernel is taken out. Thus, the resultant tamarind (ambali foal) also do not fall under the definition of agriculture produce. The processed groundnuts does not fall under the definition of agriculture produce. Similarly, copra will also fall outside the definition of agriculture produce. However, groundnuts with shell, on which no further processing is done or such processing is done as is usually done by a cultivator or producer which does not alter its essential characteristics but makes it marketable for primary market would fall within the definition of agriculture produce.

6.4 The term ‘cereal’ refers to various crops, such as wheat, paddy, maize, barley etc. If no further processing is done on such ‘cereals’ or such processing is done as is usually done by a cultivator or producer which does not alter its essential characteristics but makes it marketable for primary market, then the same would fall within the definition of agriculture produce given in the aforesaid Notification and exemption would be available to their loading, unloading, packing, storage or warehousing. However, if any processing is done on such ‘cereal’ as is not usually done by a cultivator or producer, then it will fall outside the definition of agriculture produce given in the aforesaid Notification.

7. We also observe that the applicability of Goods and Services Tax on warehousing of agricultural produce has been clarified vide Circular No. 16/16/2017-GST dated 15.11.2017 issued by the Government of India, Ministry of Finance, Department of Revenue, Central Board of Excise & Customs (Tax Research Unit)

Ruling:

8. In view of the foregoing, we rule as under –

Pulses (commonly known as ‘Dal’) (de-husked or split), jaggery, processed dry fruits such as processed cashew nuts, raisin (kismis), apricot (jardalu), fig (anjeer), date, tamarind (ambali foal), shelled groundnuts/groundnut seeds, and copra is not agriculture produce as defined under Notification No. 11/2017-Central Tax (Rate). ‘Cereal’ on which any processing is done as is not usually done by a cultivator or producer will fall outside the definition of agriculture produce.

Processed spices including processed turmeric and processed ginger (soonth), are not agriculture produce as defined under Notification No. 11/2017-Central Tax (Rate). However, groundnuts with shell, turmeric, and ginger on which no further processing is done or such processing are done as is usually done by a cultivator or producer which does not alter its essential characteristics but make it marketable for the primary market would fall within the definition of agriculture produce.

Whole pulse grains such as whole gram, rajma etc. and ‘cereal’ on which no further processing is done or such processing is done as is usually done by a cultivator or producer which does not alter its essential characteristics but makes it marketable for primary market, fall under the definition of agriculture produce as defined under Notification No. 11/2017-Central Tax (Rate).

Consultant