Original copy of GST AAR of KPH Dream Cricket Pvt. Ltd.

Original copy of GST AAR of KPH Dream Cricket Pvt. Ltd.

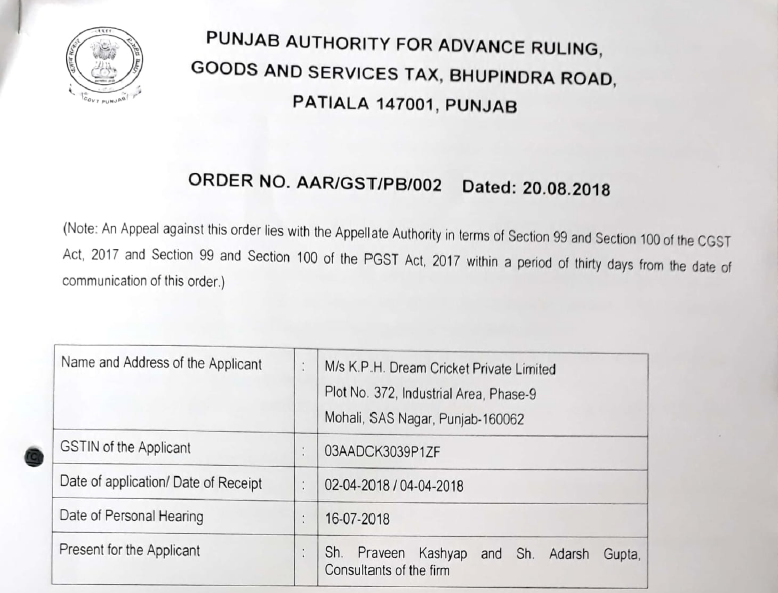

In the GST AAR of KPH Dream Cricket Private Limited. Applicant has raised the query regarding the nature of the “Complimentary Tickets”. Whether they are considered as supply or not. The GST AAR of KPH Dream Cricket Private Limited is as follows:

Order:

M/s K.P.H Dream Cricket Private Limited, Plot No. 372, Industrial Area, Phase-9, Mohali, SAS Nagar, Punjab-160062 hereinafter referred to as ‘applicant’ had submitted an application for advance ruling in form GST ARA-01 vide his letter dated 02.04.2018 received on 04.04.2018 seeking to know

1. Whether free tickets given as “Complimentary Tickets” falls within the definition of supply under CGST Act, 2017 and thus, whether the applicant is required to pay GST on such free tickets?

2. Whether the applicant is eligible to claim Input Tax Credit (for short “ITC”) in respect of complimentary tickets?

In this regard, comments from the concerned officer i.e. Assistant Commissioner of State Taxes, S A S Nagar, Mohali were sought. The concerned officer vide his letter dated 24-05-2018 stated that free tickets given as ‘Complimentary Tickets” fall within the definition of supply under CGST Act, 2017 and thus, the applicant is required to pay GST on such free tickets and applicant is also eligible to claim Input Tax Credit in respect of complimentary tickets. A personal hearing of the applicant in this regard was held on 16.07.2018 before the Advance Ruling Authority, Punjab on which date Sh, Praveen Kashyap and Sh, Adarsh Gupta, Consultants of the firm appeared on behalf of the applicant. The questions raised by the applicant were discussed at length. The consultants requested for adjournment for submission of documents. On their request, the case was adjourned with the directions to submit written submission by 30-07-2018 The applicant has sent written submission through e-mail received on 30-07-2018, which is reproduced as under:

Written submissions & synopsis by the Applicant in respect of the application for Advance Ruling:

1. That, M/s KPH Dream Cricket Private Limited (for shod “applicant” or “KPH”). having its registered office at Plot No 372 Industrial Area Phase-9, Mohali, SAS Nagar, Punjab-160062 is a franchisee of Board of Control for Cricket in India (for short “BCCl”) for the purpose of establishing and operating a cricket team to participate in Indian Premier League T20 cricket tournament (for short IPL”), under the title of “Kings XI Punjab”.

2. That IPL is a domestic professional Twenty-20 cricket tournament in India, organized by BCCI-IPL every year under the gaming rules as prescribed by the BCCI-IPL and International Cricket Council (ICC).

3. The Applicant has participated in a bid invited by the BCCI and after being successful in the said bid, entered into a Franchise Agreement, the Appellant has been permitted to establish and operate the team ‘Kings XI Punjab’.

4. Furthermore, the Applicant to participate in IPL with other franchisees wherein few matches are held at each franchisee’s home ground During the financial year 2018-19, the Appellant will participate in IPL Including the matches held at their home grounds in Mohali (Punjab) and Indore (Madhya Pradesh).

5. The applicant proposes to provide “Complimentary tickets” on account of courtesy/public relationship/promotion of business where no flow of consideration from the recipient/holder.

6. The applicant has filed an application under section 97 of Central Goods & Services Tax Act 2017 (for short “CGST Act”) seeking an advance ruling.

The questions for which advance ruling is sought are –

a. Whether free tickets given as “Complimentary Tickets” falls within the definition of supply under CGST Act, 2017 and thus, whether the applicant is required to pay GST on such free tickets?

b. Whether the applicant is eligible to claim Input Tax credit (for short “ITC”) in respect of complimentary tickets?

In furtherance to our justification stated in our above stated application for Advance ruling, the Applicant wishes to submit following additional submissions with a request to be taken into consideration to decide the matter.

ADDITIONAL SUBMISSIONS

7. The Goods and Services Tax (GST) regime has introduced a concept of ‘supply’ as a taxable event and done away with the erstwhile taxable events of sale, service, manufacture etc. This inter-alia require fresh thoughts for treatment of various transactions and events.

8. While the term ‘free supply’ is not defined under GST law or the erstwhile indirect tax laws, a ‘free supply’ as the name suggests is a supply of goods or services without any consideration (Monetary or Kind) We find it pertinent here to understand the treatment of free supply under pre-GST regime:-

a. Free supply of goods was not taxable as Value Added Tax (VAT)/ Central Sales Tax (CST) was chargeable only on ‘sales’ The term ‘Sales’ was defined under the Sale of Goods Act, 1930 which was followed to State VAT laws to mean a transfer of goods for a consideration.

b. Free supply of services was not chargeable to Service Tax as Service Tax was liable to be paid on the gross amount charged for services, and the term ‘service’ was defined to mean an activity provided by one person to another for consideration.

Under the GST regime, treatment of free supply has undergone a change on following grounds –

• Firstly, the treatment of free supplies made to related and unrelated parties differ.

• Secondly, even though GST was contemplated to treat goods and services a like, provisions relating to credit of free supplies of goods differ from those relating to credit of free supply of services.

Free supply and its taxability under GST

9. Under GST, the incidence of tax is ‘.supply’ The term ‘supply’ has been defined in an inclusive manner under Section 7 of the CGST Act. What this effectively means is that the definition is not exhaustive, and there may be some supplies which are not specified within the definition of the term.

10. The term ‘supply’ is defined to include all forms of sale, transfers, exchanges, barters etc. made or agreed to be made for a consideration in the course or furtherance of business. However, supplies between related persons or distinct persons (different offices of the same entity) in the course or furtherance of business even if not for a consideration are supplies (in terms of Schedule I to the CGST Act). As a result, free supplies between unrelated persons, cannot be said to ‘supplies’, therefore, not taxable. Whereas free supplies between related persons are ‘supplies’ and therefore, taxable.

11. The term ‘related persons’ has been defined in the explanation to Section 15 of the CGST Act. The said definition of term ‘related persons’ reads as under:-

” (a) persons shall be deemed to be “related persons” if-

(i) such persons are officers or directors of one another’s businesses;

(ii) such persons are legally recognized partners in business;

(iii) such persons are employer and employee;

(iv) any person directly or indirectly owns, controls or holds twenty-five per cent or more of the outstanding voting stock or shares of both of them;

(v) one of them directly or indirectly controls the other;

(vi) both of them are directly or indirectly controlled by a third person;

(vii) together they directly or indirectly control a third person; or

(viii) they are members of the same family;

(b) the term “person” also includes legal persons;

(c) persons who are associated in the business of one another in that one is the sole agent or sole distributor or sole concessionaire howsoever described, of the other, shall be deemed to be related.”

On perusal of above cited definition of the term ‘related person’, one may safely conclude that the applicant and the ticket holder (recipient) cannot be covered under any entry and thus cannot be said to a related person.

12. In light of the above stated legal provisions and discussion, it is view of the applicant that the activity of providing complimentary tickets without any consideration on account of courtesy/public relationship/business promotion would not fall under the definition of supply as given under Section 7 of the CGST Act, 2017 and Schedule I of CGST Act, 2017 and thus not exigible to GST.

Input tax credit

13. One of the major advantages sought to be achieved from implementation of GST is the removal of cascading effect by facilitating seamless flow of credit. The “statement of Objects and Reasons” to the Constitution (122nd Amendment) Bill, 2014, enacted as the Constitution (101st Amendment) Act, 2016 categorically includes elimination of cascading effect This would be achieved by providing for the availment of Input tax credit to the purchasing dealer in respect of the tax charged by the supplying dealer.

14. With a view to avoiding the cascading effect of taxes and build-up of tax costs, the government has consciously streamlined the credit restrictions applicable under the GST regime Section 17(5) specifically restricts credit of input tax on goods disposed of by way of free samples. It is relevant to note that the manner in which this provision has been drafted. when read along with credit reversal formula. suggests that credit is restricted only where such goods are disposed as is, and not necessarily in cases where such goods are incorporated into a final product which is disposed free of cost. Therefore, it appears that credit relating to traded goods supplied free of cost is restricted. whereas credit relating to manufactured goods supplied free of cost may not restricted.

15. As regards free supply of services, the CGST Act does not prescribe any credit restriction Therefore, in view of the applicant even though the output (free supplies of) services are not taxed, there is no need for reversal of input tax credit.

Download the GST AAR of KPH Dream Cricket Pvt. Ltd. By clicking the below image:

Consultant