Bharti Airtel Ltd Vs. UOI :Taxpayer can rectify GSTR 3b

Case Covered: Bharti Airtel Ltd Vs. UOI :

- Case of Bharti Airtel Ltd Vs. UOI , argued by Advocate Tarun Gulati in Delhi high court. In this case, taxpayers are allowed to rectify GSTR 3b in the month to which it pertains. para 4 of circular no, 26/26/2017 was read down. The original scheme of GST had a mechanism of filing GSTR 1,2,3. In that mechanism, the taxpayers were eligible to rectify the return in the month to which it pertains. Then GSTR 3b introduced. There was no provision in GSTR 3b to rectify and the mechanism of 2 and 2A was not in place. It was hard for the taxpayer to know their actual ITC. It also caused hardship in many cases, where there were huge mistakes in the amount. EIther ITC or sales were misreported. A simple example can be adding an additional zero in tax liability. It can create a huge liability. In the same manner, the taxpayer also ended up in the excess payment of 923 Crores.

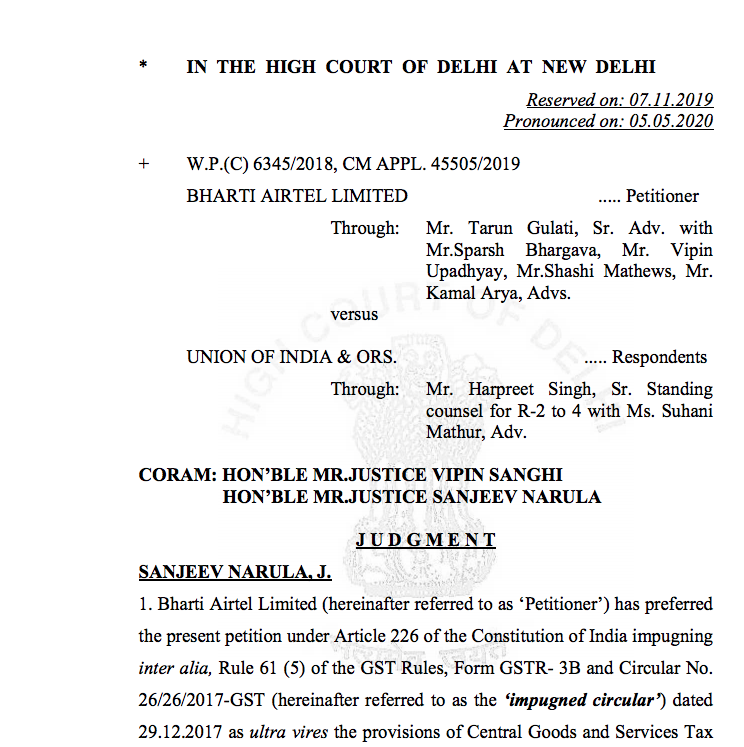

- 26/26/2017-GST (hereinafter referred to as the ‘impugned circular’) dated 29.12.2017 as ultra vires the provisions of Central Goods and Services Tax Act, 2017 (CGST Act) and contrary to Articles 14, 19 and 265 of the Constitution of India.

The Petitioner alleges that there has been excess payment of taxes, by way of cash, to the tune of approximately Rs. 923 crores.

Observation of honorable Delhi high court:

“Thus, in light of the above discussion, the rectification of the return for that very month to which it relates is imperative and, accordingly, we read down para 4 of the impugned Circular No. 26/26/2017-GST dated 29.12.2017 to the extent that it restricts the rectification of Form GSTR-3B in respect of the period in which the error has occurred. Accordingly, we allow the present petition and permit the Petitioner to rectify Form GSTR-3B for the period to which the error relates, i.e. the relevant period from July 2017 to September 2017. We also direct the Respondents that on the filing of the rectified Form GSTR-3B, they shall, within a period of W.P.(C) 6345/2018 Page 25 of 25 two weeks, verify the claim made therein and give effect to the same once verified. “

The crux of the case: Bharti Airtel Ltd Vs. UOI

In this case honorable Delhi high court accepted the Respondents have also not been able to expressly indicate the rationale for not allowing the rectification in the same month to which the Form GSTR-3B relates. The taxpayer should be allowed to rectify the GSTR 3b in the month to which it pertains.

SVN05052020CW63452018_210244

Download the judgment:

SVN05052020CW63452018_210244

Consultant