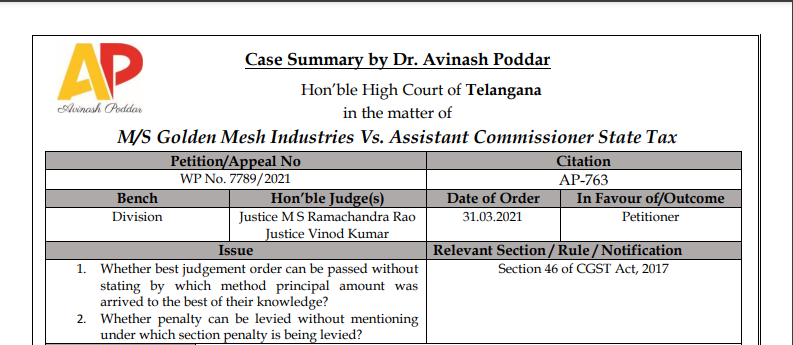

Telangana HC in the case of M/s Golden Mesh Industries Vs. Assistant Commissioner State Tax

Case Covered:

M/s Golden Mesh Industries

Vs.

Assistant Commissioner State Tax

Issue:

- Whether the best judgement order can be passed without stating by which method the principal amount arrived at the best of their knowledge?

- Whether penalty can be levied without mentioning under which section penalty is being levied?

Brief Facts of the Case:

- The Petitioner did not file the GSTR-3B for the month of November 2018.

- On 29.01.2019 notice u/s, 46 of CGST Act was issued to the petitioner.

- Petitioner did not comply with the notice and did not file its return.

- On 27.12.2019 assessment order was passed by the Assistant Commissioner State Tax to the best of his knowledge by making a demand of Rs. 1,50,000 each under the head of SGST, CGST and IGST. Amount of Rs. 1,50,000 was arrived by multiplying the average monthly SGST of Rs. 50,000 by 3.

- A penalty of 100% of the tax amount was levied upon the petitioner but the section under which penalty was levied was not mentioned in the order.

- As aggrieved by the abovementioned order, Petitioner has filed a writ petition in the Hon’ble High court of Telangana.

Related Topic:

Patna HC in the case of Pankaj Sharma V/s UOI

Brief Arguments by Petitioner/ Appellant:

Learned counsel for the petitioner contends that though the 1st respondent is entitled to do the best judgment in the absence of filing of GSTR-3B, the method adopted by 1st respondent in multiplying by 3 times the monthly SGST tax of Rs. 50,000/- to determine the tax liability is arbitrary and not based on any principle.

He also contended that 100% penalty has been levied without indicating under which provision of the Act the same has been levied.

Brief Arguments by Respondents:

Learned Assistant Government Pleader attached to the Office of the learned Advocate General appearing for respondents is unable to point out what is the principle followed by the 1st respondent is doing best judgment assessment in the manner indicated above i.e. multiplying 3 times the monthly average SGST, and adopting it as a basis for assessing the petitioner to tax for the month of November 2018. He also could not indicate under which provision of law 100% penalty is levied on the petitioner.

Related Topic:

Delhi HC in the case of Anju Jalaj Batra Versus National E-Assessment Centre

Judgement/ Ratio (in brief):

In this view of the matter, since the impugned order appears to be prima facie arbitrary and contrary to the provisions of the Telangana GST Act, 2017, the impugned order is set aside; the matter is remitted back to the 1st respondent for fresh consideration; the 1st respondent shall issue notice to the petitioner indicating the method of assessment under the best judgment assessment provision contained in Section 62 of the said Act; grant a personal hearing to the petitioner; and then pass a reasoned order both with regard to levy of tax but also with regard to interest and penalty afresh within eight (8) weeks from the date of receipt of a copy of this order.

In view of setting aside of the impugned order dt.27-12-2019 passed by 1st respondent, consequential attachment orders/garnishee orders issued by respondent Nos. 1 to 3 are also set aside.

The Writ Petition is allowed as above. No costs.

Consequently, miscellaneous petitions, pending if any shall stand closed.

Head Note/ Judgement in Brief:

Whether best judgement order can be passed without stating by which method principal amount was arrived at the best of their knowledge. NO. Whether penalty can be levied without mentioning under which section penalty is being levied. NO

Authors View:

The first issue in this was that the best judgement assessment was done by the learned Assistant Commissioner. The manner in which the amount was calculated was not having any proper base and explanation. The officer has also imposed a 100% penalty in the order but the section that was invoked for the imposition of penalty was not specified. Therefore, the Hon’ble Court was pleased to set aside the order of assessment and remanded the case back to the officer asking for a fresh assessment to be done in 8 weeks.