Time limit to file Applications in GST tribunal

Time limit to file Applications in GST tribunal extended

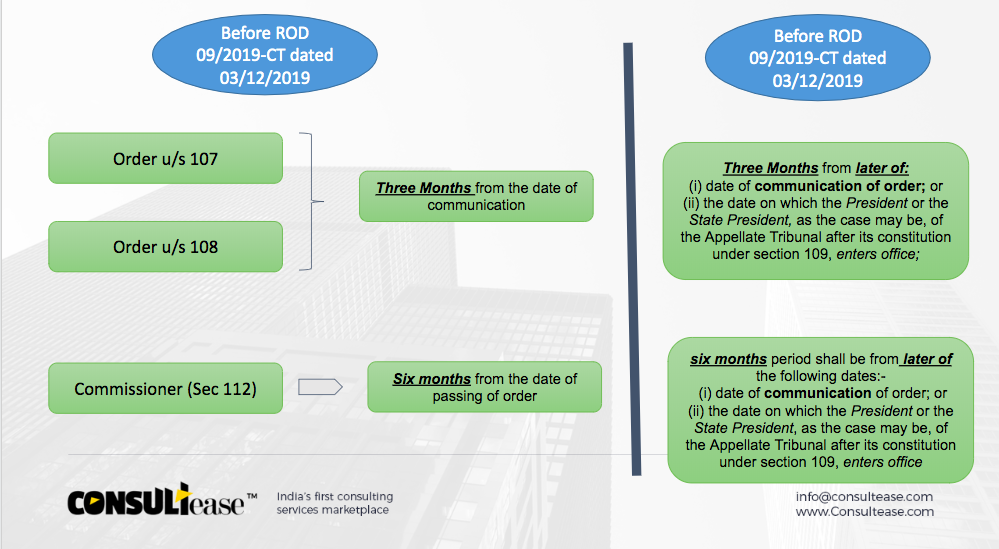

S.O.(E).––WHEREAS, sub-section (1) of section 112 of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereafter in this Order referred to as the said Act) provides that any person aggrieved by an order passed against him under section 107 or section 108 of this Act or the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act may appeal to the Appellate Tribunal against such order within three months from the date on which the order sought to be appealed against is communicated to the person preferring the appeal;

AND WHEREAS, sub-section (3) of section 112 of the said Act provides that the Commissioner may, on his own motion, or upon request from the Commissioner of State tax or Commissioner of Union territory tax, call for and examine the record of any order passed by the Appellate Authority or the Revisional Authority under this Act or the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act for the purpose of satisfying himself as to the legality or propriety of the said order and may, by order, direct any officer subordinate to him to apply to the Appellate Tribunal within six months from the date on which the said order has been passed for determination of such points arising out of the said order as may be specified by the Commissioner in his order;

AND WHEREAS, section 109 of the said Act provides for the constitution of the Goods and Services Tax Appellate Tribunal and Benches thereof;

AND WHEREAS, for the purpose of filing the appeal or application as referred to in subsection (1) or sub-section (3) of section 112 of the said Act, as the case may be, the Appellate Tribunal and its Benches are yet to be constituted in many States and Union territories under section 109 of the said Act as a result whereof, the said appeal or application could not be filed within the time limit specified in the said sub-sections, and because of that, certain difficulties have arisen in giving effect to the provisions of the said section;

NOW, THEREFORE, in exercise of the powers conferred by section 172 of the Central Goods and Services Tax Act, 2017, the Central Government, on the recommendations of the Council, hereby makes the following Order, to remove the difficulties, namely:–

1. Short title.––This Order may be called the Central Goods and Services Tax (Ninth Removal of Difficulties) Order, 2019.

2. For the removal of difficulties, it is hereby clarified that for the purpose of calculating,- (a) the “three months from the date on which the order sought to be appealed against is communicated to the person preferring the appeal” in sub-section (1) of section 112, the start of the three months period shall be considered to be the later of the following dates:-

(i) date of communication of order; or

(ii) the date on which the President or the State President, as the case may be, of the Appellate Tribunal after its constitution under section 109, enters office;

(b) the “six months from the date on which the said order has been passed” in sub-section (3) of section 112, the start of the six months period shall be considered to be the later of the following dates:-

(i) date of communication of order; or

(ii) the date on which the President or the State President, as the case may be, of the Appellate Tribunal after its constitution under section 109, enters office.