Original GST AAR of Segoma Imaging Technologies India Private Limited

Original GST AAR of Segoma Imaging Technologies India Private Limited

In the GST AAR of Segoma Imaging Technologies India Private Limited, the applicant has raised the query regarding the nature of the supply provided by them. The Applicant has provided the photography session on the request of the party (outside India). But the service is to be provided on the goods which were in India at the time of supply of services.

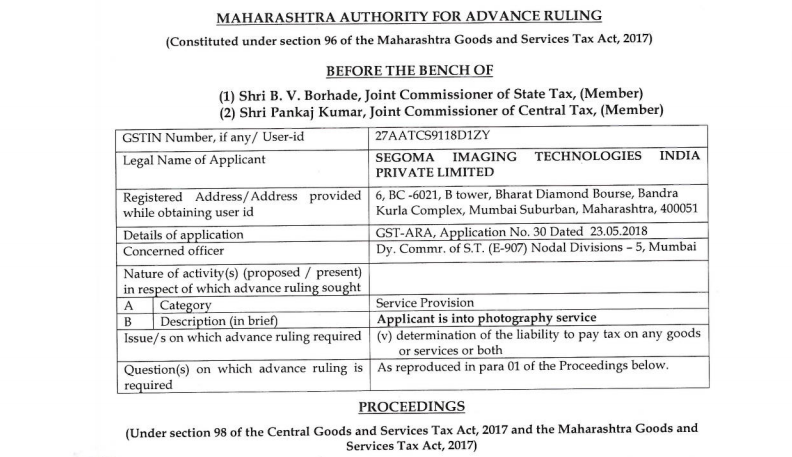

Following is the GST AAR of Segoma Imaging Technologies India Private Limited:

Order:

(Under Section 98 of the Central Goods and Services Tax Act, 2017 and the Maharastra Goods and Services Tax Act, 2017)

The present application has been filed under section 97 of the Central Goods and Services Tax Act 2017 and the Maharashtra Goods and Services Tax Act, 2017 [hereinafter referred to as “the CGST Act and the MGST Act”] by SEGOMA IMAGING TECHNOLOGIES INDIA PRIVATE LIMITED, the applicant, seeking an advance ruling in respect of the following questions.

1. Whether the supply of photography service is liable to SGST under the Maharashtra Goods and Service Tax Act, 2017 (MGST Act, 2017) and CGST under Central Goods and Service Tax Act, 2017 (CGST Act) or IGST under Integrated Goods and Service Tax Act, 2017 (IGST Act, 2017)

2. Or is it a zero rated “export” supply within the meaning of Section 2(23) r/w Section 2(6) of the IGST Act, 2017?

At the outset, we would like to make it clear that the provisions of both the CGST Act and the MGST Act are the same except for certain provisions, ‘therefore, unless a mention is specifically made to such dissimilar provisions, a reference to the CGST Act would also mean a reference to the same provision under the MGST Act. Further to the earlier, henceforth for the purposes of this Advance Ruling, a reference to such a similar provision under the CGST Act / MGST Act would be mentioned as being under the “GST Act”.

02. FACTS AND CONTENTION – AS PER THE APPLICANT

The submissions, as reproduced verbatim, could be seen thus-

STATEMENT OF THE RELEVANT FACTS HAVING A BEARING ON THE QUESTIONS : Point 15 Statement of relevant facts having a bearing on questions raised,-

- Segoma Imagining Technologies India Pvt Ltd (hereinafter referred as Segoma India) is Indian private limited company set up under Indian Companies Act.

- Segoma India is 100% Subsidiary of Segoma Ltd (hereinafter referred as Segoma Israel) which is based in Israel.

- Segoma Israel is subsidiary of R2Net which is based in US. R2Net has agreement with customers for listing Diamonds online on website www dot jamesallen dot com.

- As per agreement between R2 Net and customers of R2Net, R2NET lists on the system only those diamonds that are photographed with R2Net’s proprietary Diamond Display Technology. Customer agrees to send its diamonds and/or gemstones to be photographed in R2Net’s photography centers on a regular basis.

- R2Net has appointed Segoma Israel for photography service. Intern, Segoma Israel has made agreement with Segoma India to do photography service.

- Customers of R2Net give diamond on returnable basis to Segoma India. Segoma Israel does not have role in receiving diamond. Segoma India issues memo of receipt of diamonds to customers of R2Net. Segoma India takes photos of diamonds and upload photos of diamond on software of Segoma Israel.

- Segoma India charges Segoma Israel for providing above service of photography. Segoma Israel makes payment in convertible foreign exchange to Segoma India.

- Segoma India does not give copy of photos to customers of R2Net and does not charge any fees to customers of R2Net. R2Net has given link of software through which Customer can view photos but they cannot download photo from software.

Segoma India currently catering to Indian customers of R2Net only.

STATEMENT CONTAINING APPLICANTS INTERPRETATION OF LAW IN RESPECT OF THE UESTIONS RAISED –

Export of service

1.1. As per section 16 of Integrated Goods and Service Tax Act, 2017 (hereinafter referred as “IGST Act”), zero rated supply means any of following supplies of goods or services or both namely;(a) export of goods or services or both

1.2. Condition of export of service

As per section 2(6) of IGST Act, “export of services” means the supply of any service when,-

i. The supplier of service is located in India

ii. The recipient of service is located outside India

iii. The place of supply of service is outside India

iv. The payment for such service has been received by the supplier of service in convertible foreign exchange; and

v. The supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with explanation 1 in section 8 of IGST Act

1.3. Testing of conditions

- Condition 1: Based on above facts, Segoma India is located in India.

- Condition 2: Segoma Israel is located outside India.

- Condition 3: Based on above facts, diamonds are physically required to do photography service. Section 13(3)(a) of IGST Act, states that the place of supply of service supplied in respect of goods which are required to be made physically available by the recipient of services to the supplier of services in order to provide the service shall be the location where the services are actually performed. Segoma India performs photography service in India. However, diamonds are not owned by Segoma Israel. As per section 13(3)(a) of IGST Act recipient of services should make available physically goods to service provider. However, in above transaction of photography, diamonds are made available by third party. Segoma Israel does not have role in receiving diamond. Segoma India issues memo of receipt of diamonds to customers of R2Net. Accordingly, section 13(3)(a) of IGST Act should not be applied in above transaction. Then as per section 13(2) of IGST Act, the place of supply of services except the services specified in sub-section (3) to (13) shall be the location of the recipient of services. Service recipient is located outside India. Accordingly, place of supply of service will be outside India.

- Condition 4: Segoma Israel makes payment to Segoma India in convertible foreign exchange.

- Condition 5: as per section 2(6)(v) of IGST Act, The supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with explanation 1 in section 8. Explanation 1 of section 8 of IGST Act, which is as follow:

- Where a person has an establishment in India and any other establishment outside India then such establishments shall be treated as establishment of distinct persons.

- A person carrying on a business through a branch or an agency or a representational office in any territory shall be treated as having an establishment in that territory.

Based on above facts, Segoma India is established under India company Act and it is not branch, agency or representational office of Segoma Isreal. So Segoma India is distinct person for section 2(6)(v) of IGST Act and not covered under explanation 1 of section 8 of IGST Act.

1.4. Conclusion on Condition of export

If all following conditions are satisfied then only transaction can be considered as export of service:

| Conditions | Satisfy or not |

| The supplier of service is located in India | Yes |

| The recipient of service is located outside India | Yes |

| The place of supply of service is outside India | Yes |

| The payment for such service has been received by the supplier of service in convertible foreign exchange | Yes |

| The supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with explanation 1 in section 8 | Yes |

Based on above, transaction satisfies all conditions of exports. So it can be considered as export of service. So based on above conclusion can be drawn that above transaction would be a zero rated “export” supply within the meaning of Section 2(23) r/w Section 2(6) of the IGST Act, 2017.

Additional submissions

Original AAR filed and argument as to why the said services qualify as export of services Point 14 Questions on which advance ruling is required,-

3. Whether the supply of photography service is liable to SGST under the Maharashtra Goods and Service Tax Act, 2017 (MGST Act, 2017) and CGST under Central Goods and Service Tax Act, 2017 (CGST Act) or IGST under Integrated Goods and Service Tax Act, 2017 (IGST Act, 2017)

4. Or is it a zero rated “export” supply within the meaning of Section 2(23) r/w Section 2(6) of the IGST Act, 2017?

Point 15 Statement of relevant facts having a bearing on questions raised

- Segoma Imaging Technologies India Pvt. Ltd (hereinafter referred as Segoma India) is an Indian private limited company set up under Indian Companies Act.

- Segoma India is 100% Subsidiary of Segoma Ltd (hereinafter referred as Segoma Israel) which is based in Israel.

- Segoma Israel is subsidiary of R2Net which is based in US

- R2Net has appointed Segoma Israel for photography service. For all over the world, Segoma Israel has made agreement with Segoma India to do photography service in India. Segoma India provides Diamond Photography Services.

- R2Net has agreement with vendors for listing Diamonds online on website www dot iamesallen dot com.

- R2Net is based in USA.

- R2Net has customer base in USA.

- As per agreement between R2Net and vendors of R2Net, R2NET lists on the system only those diamonds that are photographed with R2Net’s proprietary Diamond Display Technology or Segoma photography centres. Vendor agrees to send its diamonds and/or gemstones to be photographed in R2Net’s photography centers or segoma photography centres on a regular basis. It is at option of vendor to obtain service of photography centre R2Net’s proprietary Diamond Display Technology centres or get it done through Segoma India.

- Segoma India currently catering to Indian vendors of R2Net only. Vendors of R2Net give diamond on returnable basis to Segoma India. Segoma India issues memo of receipt of diamonds to vendors of R2Net. Segoma India takes photos of diamonds and upload photos of diamond on software of Segoma Israel. Segoma India does not give copy of photos to vendors of R2Net and does not charge any fees to vendors of R2Net. Segoma Israel does not have role in receiving diamond.

- Segoma India charges Segoma Israel for providing above service of photography on cost plus 15% mark up on principal to principal basis. Segoma Israel is having its server in Israel. Segoma Israel makes payment in convertible foreign exchange to Segoma India.

- Segoma Israel does processing on the images clicked by Segoma India. Technically, Segoma Israel reworks on the photos clicked by Segoma India by compressing 500MB heavy size images to a single Image. Segoma Israel further processes and makes the image more compatible. R2Net further processes the images after receiving from Segoma Israel.

Point 16 Statement containing the applicant’s interpretation of law and/or facts, as the case may be, in respect of the aforesaid questions (i.e. applicant’s view point and submission on issues on which the advance ruling is sought)

1. Export of service

1.1. As per section 16 of Integrated Goods and Service Tax Act, 2017(hereinafter referred as “IGST Act”), zero rated supply means any of following supplies of goods or services or both namely; –

(a) export of goods or services or both

1.2. Condition of export of service

As per section 2(6) of IGST Act, “export of services” means the supply of any service when, The supplier of service is located in India,-

i. The recipient of service is located outside India

ii. The place of supply of service is outside India

iii. The payment for such service has been received by the supplier of service in convertible foreign exchange; and

iv. The supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with explanation 1 in section 8 of IGST Act

1.3. Testing of conditions,-

- Condition 1: Based on above facts, Segoma India is located in India.

- Condition 2: Segoma Israel is located outside India.

- Condition 3: Based on above facts, diamonds are physically required to do photography service. Section 13(3)(a) of IGST Act, states that the place of supply of service supplied in respect of goods which are required to be made physically available by the recipient of services to the supplier of services in order to provide the service shall be the location where the services are actually performed.

Segoma India performs photography service in India. However, diamonds are not owned by Segoma Israel. As per section 13(3)(a) of IGST Act recipient of services should make available physically goods to service provider. However, in above transaction of photography, diamonds are made available by third party. Segoma Israel does not have role in receiving diamond. Segoma India issues memo of receipt of diamonds to vendors of R2Net. Accordingly, section 13(3)(a) of IGST Act should not be applied in above transaction.

Then as per section 13(2) of IGST Act, the place of supply of services except the services specified in subsection (3) to (13) shall be the location of the recipient of services. Service recipient is located outside India. Accordingly, place of supply of service will be outside India.

- Condition 4: Segoma Israel makes payment to Segoma India in convertible foreign exchange.

- Condition 5: as per section 2(6)(v) of IGST Act, the supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with explanation 1 in section 8. Explanation 1 of section 8 of IGST Act, which is as follow:

o Where a person has an establishment in India and any other establishment outside India then such establishments shall be treated as establishment of distinct persons,

o A person carrying on a business through a branch or an agency or a representational office in any territory shall be treated as having an establishment in that territory.

Based on above facts, Segoma India is established under Indian companies Act having PAN No. and it is not branch, agency or representational office of Segoma Israel. So Segoma India is distinct person for section 2(6)(v) of IGST Act and not covered under explanation 1 of section 8 of IGST Act.

Diagrammatic Presentation

Analysis for services provided not falling under 13(3)(a)

The place of supply of services where the Supplier or Recipient located Outside India is determined by section 13 of IGST Act.

The provisions of this section shall apply to determine the place of supply of services where the location of the supplier of services or the location of the recipient of services is outside India.

The place of supply of services except the services specified in sub-sections (3) to (13) shall be the location of the recipient of services:

Provided that where the location of the recipient of services is not available in the ordinary course of business, the place of supply shall be the location of the supplier of services.

3) The place of supply of the following services shall be the location where the services are actually performed, namely:-

(a) services supplied in respect of goods which are required to be made physically available by the recipient of services to the supplier of services, or to a person acting on behalf of the supplier of services in order to provide the services:

Provided that when such services are provided from a remote location by way of electronic means, the place of supply shall be the location where goods are situated at the time of supply of services:

Provided further that nothing contained in this clause shall apply in the case of services supplied in respect of goods which are temporarily imported into India for repairs and are exported after repairs without being put to any other use in India, than that which is required for such repairs;

On analysis of above.

As mentioned earlier,

Section 13 (3) of IGST Act, 2017: (a) Services supplied in respect of goods which are required to be made physically available by the recipient of services to the supplier of services (or his agent) in order to provide the services.

The Diamond Vendors who are the owners of the diamonds make them available through delivery challan to Segoma India for photographs which is on Principal to Principal basis and not as an agent of R2net.

R2Net enters into agreement with diamond vendors in India and as per the clause 2.4 between R2Net and diamond vendors as below

“R2NET lists on the System only those diamonds that are photographed with its proprietary Diamond Display Technology-Segoma. Vendor agrees to send its diamonds and/or gemstones to be photographed in R2Net’s or Segoma photography centres on a regular basis”. Segoma has no relation with diamond vendors or R2Net it only provides photography services to Segoma Israel as per agreement with Segoma Israel.

Photography of Diamonds is a service in respect of goods which are required to be made physically available by recipient of service (directly to Segoma Israel).

Section 2 (93) of CGST Act, 2017: Recipient of Supply of goods or services or both, means-

(a) Where a consideration is payable for the supply of goods or services or both, the person who is liable to pay that consideration;

(b) Where no consideration is payable for the supply of goods, the person to whom the goods are delivered or made available, or to whom possession or use of goods is given or made available; and

(c) Where no consideration is payable for the supply of service, the person to whom the service is rendered, and any reference to a person to whom a supply is made shall be construed as a reference to the recipient of the supply and shall include an agent acting as such on behalf of the recipient in relation to the goods or services or both supplied.

Hence to conclude on the recipient of service as per the above provisions Segoma Israel will be recipient of service under Section 2 (93) (a).

Conclusion:

As per section 13(3)(a) of IGST Act recipient of services should make available physically goods to service provider. In service of photography, diamonds are made available by vendors in India and payment is made by Segoma Israel who does not have role in receiving diamond. Segoma India receives goods on delivery challan and issues memo receipt for photography to the vendors which is returned after photography to vendor. Accordingly, section 13(3)(a) of IGST Act cannot be applied in above transaction.

Segoma India is not agent of R2Net

As per Section 2(13) of IGST Act, 2017

“intermediary” means a broker, an agent or any other person, by whatever name called, who arranges or facilitates A the supply of goods or services or both, or securities, between two or more persons, but does not include a person who supplies such goods or services or both or securities on his own account;

As per above definition “Intermediary” does not include a person who supplies the goods or services on his own account.

Segoma India provides photography services to Segoma Israel and Segoma Israel has contract to provide service to R2Net hence Segoma India provides service on principal to principal basis to Segoma Israel on its own account. Segoma India works on Principal to Principal basis as they take the risk of loss of diamonds, damage to diamonds, theft of diamonds during there possession and in case of defective service it is a loss to them and their efforts would be wasted.

Advance Ruling Related to Intermediary Services:

1. Provision of marketing support services, call centre services, payment processing etc does not amount to provision of ‘intermediary’ services (M/s GoDaddy India Web Services Pvt. Ltd. Versus Commissioner of Service Tax. Delhi-IV)

The applicant entered into an agreement to provide marketing support services, (including direct marketing, branding activities, offline marketing), call centre services, payment processing services to its parent company. The Applicant was not all concerned about the services provided by GoDaddy US directly to their Indian Customers, which related to domain name registration, transfer services, web hosting services, designing services etc. In this case, applicant was not in receipt of any remuneration/consideration from the Indian Customers of GoDaddy US. Applicant was to only receive a fee from GoDaddy US, being the operating cost incurred by the applicant plus mark up of 13% on such costs. It was noticed that applicant was to receive the said fees from GoDaddy US, even in respect of Indian Customers, who directly remitted the service charges to GoDaddy US through International Credit Card, wherein applicant is not in the picture. This fact further shows that the applicant is not providing any service to Indian Customers and hence could not be said to be an intermediary for the purpose of POPS rules.

Reimbursements of salary and other emoluments of employees under deputation contracts with Group companies is not a service itself. Incidentally it can inferred that mere presence of three parties involved (individual, group company and subsidiary company) does not make the service as an intermediary service (M/s North American Coal Corporation India Pvt. Ltd. V. Commissioner of Central Excise, Pune-III)

In this case, certain employees of the US Company were sent on deputation to its Indian subsidiary. The salary payment of US Company’s employee was continued to be paid in the US and were recovered from the Indian company. The issue was on the levy of service tax on such recoveries by the US Company. The Advance Ruling authority held that the agreement is very clear to suggest that so long as individual is serving in India, he will be treated to be the employee of the applicant (i.e. Indian company) though his interests as the employee of NAC, US, insofar as the social security interests are concerned, will be taken care of by NAC, US. It is trite that he does not get the salary from NAC, US when he is offering services to NAC, India in that behalf, the benefits are mutually exclusive, at least so far as, they are concerned with the salary. The only obligation on NAC, US is regarding the social securities which are not reimbursed by NAC, India to NAC, US – merely because the social security of Mr. Sloan while he is in India is being taken care of by the NAC, US. The service of the individual with NAC, India cannot be viewed otherwise in view of the clear language of the provisions of law. There shall be no liability to pay service tax on the salary and the allowances payable by the applicant to the employee in terms of the dual employment agreement and such salary will not be eligible to levy the service tax as per the provisions of the Finance Act.

Customer support and payment processing services provided by the service provider does not make the service provider an intermediary, as Iong as the services are provided on own account. (M/s Universal Services India Pvt. Ltd. v.The Commissioner of Service Tax, Gurgaon, Ruling No. AAR/ST/07/2016 in Application No. AAR/44/ST/14/2014)

In this case, the applicant proposed to assist WWD US with the processing of payments made by their customers in India through their internet banking facilities/ credit cards. The detailed facts were as follows – WWD US would provide its services and products to customers in India through its website. In respect of such services, the customers would make the payment to WWD US online. For making such payment, in case the customers used an international credit card, they would be making a payment directly to WWD US in US Dollars. The applicant would provide payment processing facilities in India and collect money from the customers of WWD US in India and remit the same to WWD US. Towards this, the applicant proposes to open a separate bank account in India wherein the payment collection gateway company appointed by the applicant will deposit the money so collected from the customers of WWD US. The applicant would charge a fee equal to the operating costs incurred by the applicant plus a mark-up of 13% on such costs. The applicant is not authorized to enter into any contract or arrangement on behalf of WWD US or which bind it in any manner whatsoever. WWD US will directly contact and provide services to customers in India. The Advance Ruling Authority held that from the facts, the applicant would not be receiving any fees in respect of processing the payments of the customer remitted directly through the payment gateway. Since the service is being provided on own account, the service is not covered by Rule 9 (intermediary services) but covered under Rule 3 of the POPS rules, 2012. The Advance Ruling Authority relying on the CBEC Education Guide dated 20th June 2012 issued by Ministry of Finance, Department of Revenue, Tax Research Unit (‘TRU’) held that normally a service receiver is the person is legally entitled to receive the service and is therefore obliged to make payment of the service received whether or not he actually makes the payment or someone else makes the payment on his behalf. In the facts of the present case, even though the applicant processed the payment of the customer, the service was being rendered to WWD US who was legally entitled receive the service and obliged to make payment for the same. Hence as per above it is amply clear that Segoma India does not fall under intermediary.

03. CONTENTION – AS PER THE CONCERNED OFFICER dt.23.08.2018

The submission, as reproduced verbatim, could be seen thus-

It is Submitted that, Issue on which advance ruling is required:-

M/s. Segoma Imaging Technologies India Private Limited has given elaborative submission before maharashtra Authority for Advance Ruling. He has asked ruling on whether the transaction is taxable under GST Acts or not.

I wish to submit few points before Authority in relation to submission by dealer.

Under heading “Question of Law”, the dealer has sought ruling from Authority that whether Transactions summarized in “Brief Facts” fall under Export of Services under Section 2(6), attracting Zero rated Tax under Section 16(1)(a) of IGST Act 2017.

Section 2(6) of IGST Act states

(6) “export of services” means the supply of any service when,-

i) the supplier of service is located in India;

(ii) the recipient of service is located outside India;

(iii) the place of supply of service is outside India;

(iv) the payment for such service has been received by the supplier of service in convertible foreign exchange; and

(v) the supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with Explanation 1 in section 8.

- As per Section 97(2) of CGST MGST Act 2017, The question on which the advance ruling is sought under this Act, Whether a transaction is Export of Services or not is dependent upon the fact as to whether Supply of Services is out of India or Not. Consequently, if the MAAR proceeds ahead with examination and consideration of this fact, discussion and findings on aspect of place of supply will be inevitable.

The Act limits AAR to decide issued earmarked for it under Section 97(2) of MGST/CGST Act. Therefore, where a question also involves examination of place of Supply (which is not amongst the issued which can be decided by AAR), the question cannot be taken by the authority for lack of jurisdiction.

(Ref:- Decision by Haryana Authority for Advance Ruling HAR/HAAR/R/2018-19/6).

- Secondly, we may refer to submission by dealer under heading Rules of Interpretation (Page No-6, point No-ii) which argues about “consideration must yield to clear & express provisions of the law”. Also, as per point No vi and vii, dealer has quoted that -“legislature is presumed to have made no mistakes and legislature intends to say, what it has said.”

B. Without prejudice to above, I would like to attract your attention to following provisions of Section 13 (3) of IGST Act which says:

The place of supply of the following services shall be the location where the services are actually performed, namely:-

(a) Services supplied in respect of goods which are required to be made physically available by the recipient of services to the supplier of services, or to a person acting on behalf of the supplier of services in order to provide the services:

Provided that when such services are provided from a remote location by way of electronic means, the place of supply shall be the location where goods are situated at the time of supply of services:

Provided further that nothing contained in this clause shall apply in the case of services supplied in respect of goods which are temporarily imported into India for repairs and are exported after repairs without being put to any other use in India, than that which is required for such repairs.

C. The dealer has contended in point No.15 that ” As per Agreement between R2Net and Vendors, R2NET lists on the system ONLY those diamonds that are photographed” …………….

- “Segoma India currently catering to Indian vendor’s f R2Net only”.

- “Vendors of R2Net give diamond on returnable basis to Segoma India”

- Point 2.4 of Operating Policy of R2Net categorically describes R2Net lists on the system ONLY those diamonds that are photographed with its proprietary Diamond Display Technology-Segoma”

It is to note that Segoma India does NOT have liberty to photograph and upload images of any other dealer. The diamonds are only those which are made available after privity of contract between Vendors and R2Net. Thus, it is cleared from above facts, that the Recipient has Constructive control over making diamonds physically available for Supply of Services and hence fall under Section 13(3) (a) of IGST Act 2017.

D. Dealer has claimed to be a distinct person and out of ambit of Explanation 1 of Section 8 of IGST Act. The very section says:

Explanation l.-For the purposes of this Act, where a person has,

(i) an establishment in India and any other establishment outside India;

(ii) an establishment in a State or Union territory and any other establishment outside that State or Union territory; or

(iii) an establishment in a state or Union territory and any other establishment being a business vertical registered within that State or Union territory, then such establishments shall be treated as establishments of distinct persons.

As per agreement copy submitted by dealer, M/s. Segoma India is Service provider, wholly owned subsidiary of Service recipient. M/s. Segoma Limited and Segoma India are “fixed establishment” as per section 2(7) of IGST Act 2017. Thus it does not satisfy the condition V of Section 2(6) IGST Act 2017.

E. Also the Tax invoice shows that M/s. Segoma Limited has been charged in Indian Rupees and has received consideration in foreign currency, figures of which do not match. It is contravention with condition (iv) of Section GST 2(6) of IGST Act 2017.

Hence dealer’s application cannot be maintained under heading with question of law that whether said transaction is Export of Services or not. Dealer’s application may please be rejected.

In addition, the location of Supplier is in Mumbai. Thus, the type of supply should be Intra-state. Hence he is liable to pay CGST+SGST for supply of Services as per section 13(3) (a).

Additional submissions of Applicant in connection with contention of officer dt 23.08.2018—

1. Learned Deputy Commissioner of State Tax (E-907) has quoted incomplete Para no 2.4. The original quote from the agreement is reproduced herein below

“R2NET lists on the system only those diamonds that are photographed with its proprietary Diamond Display Technology- Segoma. Vendor agrees to send its diamonds and/or gemstones to be photographed in R2Nets’s or Segoma photography centers on a regular basis.”

Whereas the point 2.4 of the operating policy is quoted incomplete by Learned Deputy Commissioner of State Tax (E-907 as follows

“R2NET lists on the system only those diamonds that are photographed with its proprietary Diamond Display Technology- Segoma.”

We would like to invite the attention of your Honor that there are two distinct persons, one is R2Net’s proprietary Diamond Display Technology having presence at New York and other Segoma photography centers having presence all over world. Hence, it is aptly clear that it is at the option of the vendors where to send the diamonds for photography. The diamonds are made available by vendors of R2Net in India and not by any’ means by the R2Net. Segoma India provides service to Segoma Israel and hence Segoma Israel is the recipient and not R2Net.

As per section 13(3)(a) of the IGST Act, 2017

The place of supply of the following services shall be the location where the services are actually performed, namely: (a) services supplied in respect of goods which are required to be made physically available by the recipient of services to the supplier of services, or to a person acting on behalf of the supplier of services in order to provide the services.

Therefore, as per above extract of section 13(3)(a) of the CGST Act, it is very clear that goods are not made available by R2Net.In fact, diamonds for photography are provided as per vendors convenience. There is no control of R2Net for providing the diamonds for photography to Segoma or R2 Net’s proprietary firm. As per above clause, R2Net is not providing the diamonds nor it is recipient of the service or even have any control to provide the diamonds to Segoma India for photography. Also, it is very pertinent to note that Segoma India does not deliver photographs to Indian vendors. Therefore, place of supply of services is not covered by section 13(3)(a) and transaction qualifies as export of services.

2. Learned Deputy Commissioner of State Tax (E-907) believes that Segoma India does not satisfy the condition V of Section 2(6) of IGST Act, 2017 i.e. conditions to qualify as export of services.

We therefore would like to submit to your Honor that as per section 2(6)(v) of IGST Act,

“the supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with explanation 1 in section 8”.

Explanation 1 of section 8 of IGST Act, which is as follows:

- Where a person has an establishment in India and any other establishment outside India then such establishments shall be treated as establishment of distinct persons.

- A person carrying on a business through a branch or an agency or a representational office in any territory shall be treated as having an establishment in that territory. Based on above facts, Segoma India is established under Indian companies Act having separate PAN number and it is not branch, agency or representational office of Segoma Israel. So Segoma India is distinct person for section 2(6)(v) of IGST Act and not covered under explanation 1 of section 8 of IGST Act.

There is no question of fixed establishment of as per 2(7) of the IGST Act, 2017.

2. Learned Deputy Commissioner of State Tax(E-907) believes that Segoma Limited has been charged in Indian Rupees and has received consideration in foreign currency, figures of which do not match thus Segoma India is in contravention with condition(iv) of section 2(6) of IGST Act 2017.

In the above context we would like to submit as under:

Following are the conditions for the export “export of services” means the supply of any service when,-

(i) the supplier of service is located in India;

(ii) the recipient of service is located outside India;

(iii) the place of supply of service is outside India;

(iv) the payment for such service has been received by the supplier of service in convertible foreign exchange; and

(v) the supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with Explanation 1 in section 8;

The condition here stated is that payment received by the supplier of service should be in convertible foreign exchange. The said condition is correctly satisfied. The sample FIRC and invoices are submitted in the earlier submission on 31st July 2018.

According to the above analysis it may be concluded that Segoma India is providing services to Segoma Israel. segoma Israel is the recipient of the services. The place of supply of services shall be the location of the recipient of service i.e. Israel and hence qualifies as export of services.

04. HEARING

The case was taken up for Preliminary hearing on dt. 03.07.2018 with respect to admission or rejection of present application when Sh. Pathik Shah, C.A. alongwith Sh. Mukhtar Shaikh, Asstt. manager appeared and made contentions for admission of application as made in their ARA. jurisdictional Officer, Sh. Manoj Ohekar, Dy. Commissioner of S.T. (E- 907) Nodal Division – 5, Mumbai appeared and stated that they would be making written submissions in due course.

The application was admitted and called for final hearing on 31.07.2018, Sh. Madhukar P. Khandekar, C.A. along with Sh. Rajesh Mehta, C.A. Sh. Mukhtar Shaikh, Asstt. Manager, Sh. Dharmesh Padnabhan, Vice President and Sh. Gaurav Shetty, Employee of the company appeared and made oral and written submissions. Jurisdictional Officer, Sh. Manoj Ohekar, Dy. Commissioner of S.T. (E- 907) Nodal Division – 5, Mumbai appeared and made written submissions.

Download the Original GST AAR of Segoma Imaging Technologies India Private Limited. By clicking the below image:

05. OBSERVATIONS

We have gone through the facts of the case. The issue was heard at length from both the sides. In this application the questions that are raised for decision by the applicant relate to taxability of a transaction of supply of photography service by the applicant to their overseas recipient. Before we deal with the issue it is necessary first to understand the relationship between the parties and the nature of transaction. Applicant (in short Segoma India) is accompany set up under Indian Companies Act. Applicant is 100% subsidiary of Segoma Ltd (in short Segoma Israel) which is based in Israel. Segoma Israel is also subsidiary of R2Net based in USA, (in short R2Net). The transaction in question follows following sequence. As per the agreement between R2Net and its customer, R2Net lists on the system only those diamonds that are photographed with R2 Nets Display Technology. For the purpose of photography service R2Net has appointed Segoma Israel who in turn made agreement with Segoma India to do photography service. As per the terms of agreement customers of R2Net send their diamonds and or gem stones to be photographed to Segoma India who issues memo of receipt of diamonds to customers of R2Net. At last Segoma India takes photos of diamond and upload photos of diamond on software of Segoma Israel. It is this transaction between Segoma India and Segoma Israel of providing photography service which is claimed as a zero rated export supply within the meaning of section 16 of the IGST Act and exempt from levy of tax. It is the view point of the applicant that impugned transaction of photography service satisfies all the conditions of export of services within the meaning of section 2(6) and section 16 of the IGST Act.

In view of their submissions we are required to ascertain whether applicant satisfies all the conditions simultaneously as mentioned in Section 2(6) of the IGST Act. In this case admittedly the location of the provider of services is in India and the location of the recipient of service is in Israel and therefore we take this opportunity to discuss whether the supply of service by the applicant in this case satisfies all the provisions of section 2(6) of the IGST Act, to be treated as an export of services and to qualify as ‘zero rated supply within the meaning of section of 16 of the IGST Act. A supply of service must satisfy simultaneously all conditions of section 2(6) of the IGST Act to be considered as export of service, which are reproduced as below:-

”Section 2(6) “export of services” means the supply of any service when,-

(i) the supplier of service is located in India;

(ii) the recipient of service is located outside India;

(iii) the place of supply of service is outside India;

(iv) the Payment for such service has been received by the supplier of service in convertible foreign exchange; and

(v) the supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with Explanation 1 in section 8;”

There is no doubt that the supply of service in the present case satisfies conditions at (i) and (ii) of Section 2(6) of the IGST Act. However as stated above, to qualify as an ‘export of services’ all the conditions must be satisfied simultaneously and therefore we now take upon ourselves to discuss whether applicant satisfies (iii), (iv) and (v) of section 2(6) of the IGST Act.

As per condition at (iii) above, which pertains to place of supply of service and that the place of supply of service shall be outside India. Section 13 of the IGST Act contains provisions for determining the place of supply of services where the location of the supplier of the services or the location of the recipient of services is outside India.

The place of supply of service shall be determined as per the provision contained in section 13 of the IGST Act. The said section has been divided into two parts. The subsections (3) to (13) provides for determination of place of supply of service, for service other than those listed in sub-sections (3) to (13). In the instant case and from the perusal of transactions we are of the opinion that except subsection (3) all other subsections are irrelevant for the purpose of determination of place of supply and therefore we restrict ourselves to the provisions of subsection (3) of section 13 of the IGST Act which is as under: Section 13(3) The place of supply of the following services shall he the location where the services are actually performed, namely:-

(a) services supplied in respect of goods which are required to be made physically available by the recipient of services to the supplier of services, or to a person acting on behalf of the supplier of services in order to provide the services:

Provided that when such services are provided from a remote location by way of electronic means, the place of supply shall be the location where goods are situated at the time of supply of services:

Provided further that nothing contained in this clause shall apply in the case of services supplied in respect of goods which are temporarily imported into India for repairs and are exported after repairs without being put to any other use in India, than that which is required for such repairs;

(b) services supplied to an individual, represented either as the recipient of services or a person acting on behalf of the recipient, which require the physical presence of the recipient or the person acting on his behalf, with the supplier for the supply of services.

In this transaction we find that diamonds are physically required to do photography service and this fact is not denied by the applicant. However it is the contention of the applicant that diamonds are not owned by Segoma Israel. He further submits that the recipient of services should make available physically goods to service provider and on the contrary in this case diamonds are made available by third party. Accordingly he submits that provision of section 13 (3) (a) of the IGST Act should not be applied in his case.

The main contention of the applicant for non-applicability of section 13 (3) (a) of the IGST Act regarding determination of place of supply is that the goods which are required to be made physically available must be owned or made available only by the recipient of services. This line of argument in this respect is hard to accept and is not tenable. However from the plain reading of subsection (a) of subsection 3 of section 13 of the IGST Act, we do not agree with the contention of the applicant that the goods that are required for rendering service by the supplier must be owned or made available only by the recipient of services. As per above clause, recipient of service who want to avail services has to make goods physically available on direct or indirect directions to the service provider and it does not matter who owned the goods. Accepting the proposition of law and its interpretation as made by the applicant, would clearly amount to addition of words which are absent in the provisions.

In our view where words of the statute are clear, plain and unambiguous then it must be given their ordinary meaning.

It is the cordial rule of interpretation that where the language used by the legislature is clear and unambiguous then the plain and natural meaning of the words should be supplied to the language used and resort to any rule of interpretation to unfold the intention is permissible only where there is any ambiguity. Plethora of decisions of the Apex Court are there to support the proposition, for e.g. Smt. Tarulata Shyam Vs CIT 108 ITR 345 (SC). This concept is explained in detail by the Hon. SC in M/S. Grasim Industries Ltd. vs Collector of Customs, Bombay on 4 April, 2002 in Appeal (Civil) 1951 of 1998.

The court held that –

“The elementary principle of interpreting any word while considering a statute is to gather the mens or sententia legis of the legislature. Where the words are clear and there is no obscurity, and there is no ambiguity and the intention of the legislature is clearly conveyed, there is no scope for the Court to take upon itself the task of amending or alternating the statutory provisions. Wherever the language is clear the intention of the legislature is to be gathered from the language used. While doing so what has been said in the statute as also what has not been said has to be noted. The construction which requires for its support addition or substitution of words or which results in rejection of words has to be avoided.”

Keeping in mind this proposition we are of the view that there is no need that the goods physically required for rendering services must be owned by the recipient of the services, on the other hand it is sufficient for the recipient to make them physically available to the service provider for rendering services.

Thus in this case the event of photography services pertaining to diamonds made physically available by the recipient of services to the provider of services is over and the service is clearly provided in India where the services are actually performed.

The next condition to be satisfied is that the payment for services in question must have been received in convertible foreign exchange. The condition (iv) reads as ‘the payment for such service has been received by the supplier of services in convertible foreign exchange.’ The jurisdictional officer submits that the tax invoice shows that Segoma India has charged in Indian Rupees and has received consideration in foreign currency, figures of which do not match and come to the conclusion that condition (iv) is not satisfied. As per this condition the payment received by the supplier of services should be in convertible foreign exchange. Applicant has submitted sample FIRC (Foreign Inward Remittance Certificate) and invoices and as such we find that applicant has satisfied this condition.

The condition (v) of the definition of ‘export of services’ as per section 2(6) reads as: ‘the supplier of service and the recipient of service are not merely establishment of a distinct person in accordance with Explanation 1 in section 8;’

As per this condition the supplier of service and recipient of service should be separate legal person and not mere an establishment of distinct person. In the present case, it is observed that R2Net which is based in USA and Segoma Israel is its subsidiary. Further Segoma India is a subsidiary of Segoma Israel. So also we find that as per agreement between R2Net and their customer, R2Net lists on the system only those diamonds that are photographed with its proprietary Diamond Display Technology – Segoma.

Thus applicant does not have liberty to photograph and upload images except those finalized by R2Net. In view of this it appears that applicant is carrying on business in Indian territory as a representational office of Segoma Israel and thus is covered by Explanation 1 of Section 8 of the IGST Act. Applicant’s submission in this regard is that they are established under the Indian Companies Act having separate PAN number and therefore it is not a branch, agency or representational office of Segoma Israel.

However, the statutory compliances made by an applicant in a country, in this case India, would in no way alter the status or relationship between parties as discussed above.

Thus applicant also failed to satisfy this condition as well. We have already stated that all the conditions stipulated in section 2(6) shall be simultaneously complied with in order to consider any services as export of services. As a matter of fact we have noticed that conditions at (iii) and (iv) have not been complied with, in this case and as such impugned supply is not ‘export of services’ within the scope of section 2(6) of the IGST Act.

In the case before us it is seen that the location of the supplier of service is in Mumbai and the place of supply as determined as per provisions of section 13(3) (a) of the IGST Act is also in Mumbai, a place where the services are actually performed. And therefore as per section 8(2) of IGST Act, the services shall be treated as intrastate supply and would be liable to tax under the provisions of MGST Act and CGST Act.

05. In view of the extensive deliberations as held hereinabove, we pass an order as follows

ORDER

(Under section 98 of the Central Goods and Services Tax Act, 2017 and the Maharashtra Goods and Services Tax Act, 2017)

NO. GST-ARA-30/2018-19/B-92 Mumbai Dt. 20/08/2018

For reasons as discussed in the body of the order, the questions are answered thus –

Question 1. – Whether the supply of photography service is liable to SGST under the Maharashtra Goods and Service Tax Act, 2017 (MGST Act, 2017) and CGST under Central Goods and Service Tax Act, 2017 (CGST Act) or IGST under Integrated Goods and Service Tax Act, 2017 (IGST Act, 2017)?

Answer: – Answered in the affirmative.

Question 2:- Or is it a zero rated “export” supply within the meaning of Section 2(23) r/w Section 2(6) of the IGST Act, 2017?

Answer: – Answered in the Negative

Source: https://www.mahagst.gov.in/sites/default/files/ddq/GST%20ARA%20ORDER-SEGOMA%20IMAGING%20TECHNOLOGIES%20INDIA%20PV.pdf

Consultant