Original copy GST AAR of Sanofi India limited

AAR of Sanofi India limited:

This is one of the landmark AAR for promotional items and free gifts. In AAR of Sanofi India, limited detailed discussion was made on this issue.

Order:

The present application has been filed under section 97 of the Central Goods and Services Tax Act, 2017 and the Maharashtra Goods and Services Tax Act, 2017 [hereinafter referred to as “the CGST Act and MGST Act respectively”] by M/s SANOFI INDIA LIMITED, seeking an advance ruling in respect of the

following questions:

1. Whether input tax credit is available of the GST paid on expenses incurred towards promotional schemes of Shubh Labh Loyalty Program?

2. Whether input tax credit is available of the GST paid on expenses incurred towards promotional

schemes goods given as brand reminders?

At the outset, we would like to make it clear that the provisions of both the CGST Act and the MGST Act are the same except for certain provisions. Therefore, unless a mention is specifically made to any dissimilar provisions, a reference to the CGST Act would also mean a reference to the same provision under the MGST Act. Further to the earlier, henceforth for the purposes of this Advance Ruling, the expression ‘GST Act’ would mean CGST Act and MGST Act.

Related Topic:

Original GST AAR of M/s SSSVK Cold Storage Private Limited

02 FACTS AND CONTENTION – AS PER THE APPLICANT

The submissions, as reproduced verbatim, could be seen thus-

“3.1 Statement of relevant facts having a bearing on the question(s) raised Facts of the Case :

a. Sanofi India Limited (“Sanofi” or “We” or “the Company” or “the Applicant”), in India is engaged in business of sale of pharmaceutical goods and services through group entities. Sanofi has its head office in Mumbai and manufacturing unit at Goa and Ankleshwar. Sanofi also gets its products manufactured through Third party manufacturers who manufacture goods on Contract manufacturing basis. Further Sanofi provides taxable services and is registered under GST.

b. Sanofi in its business operations incurs various marketing and distribution expenses. The said expenses are incurred with a view to promote their brand/ products and enhance its sales. Under various schemes, Sanofi distributes different products among its trade ‘channels as promotional items or brand reminders. Further, Sanofi also offers various promotional schemes such as Shubh Labh trade loyalty program, ete.

c. In case of brand reminders, products like pens, notepad, key chains, etc. are distributed for the distributors with their name embossed on it. The brand embossed on these products serve as an advertisement tool and is a brand reminder. Such products act as ‘reminder of the association

with the brand Sanofi so as to promote products of Sanofi.

d. In case of Shubh Labh trade loyalty program (Catalogue enclosed as Annexure I), the distributors/wholesalers get rewards based on the reward points earned on the basis of the quantity of goods sold by them.

Related Topic:

Original copy of GST AAR of Vservglobal Private Limited

For example, Combiflam Tablet purchased in a minimum quantity of 01 shippers/case or 14,040 tablets will be eligible for 01 reward coupon. On activation of one (01) Combiflam coupon, the wholesaler will be credited with FIFTEEN (15) reward points and confirmed via text/SMS to the registered mobile number. Further, as per the scheme catalogue, the wholesalers who have earned 35000 points will be eligible for Singapore Trip For 2 Persons; 6 Days/5 Nights, the wholesalers who have earned 24000 points will be eligible for claiming Raymond Weil 2760-St3-50001 Watch -For Men, etc.

e. In the above example, when the wholesaler opts for Raymond watch, the watch is purchased by Sanofi and provided to the wholesaler as per the agreed terms of the promotional scheme. The invoice for the said watch is raised in the name of the Sanofi and accordingly, input tax credit (‘ITC’) of the GST paid on the watch is claimed by Sanofi.

3.2 STATEMENT CONTAINING APPLICANTS INTERPRETATION OF LAW AND/OR FACTS, AS THE CASE MAYBE, IN THE CASE OF THE AFORESAID QUESTIONS:

The Applicant prefers this application for Advance Ruling under Section 97 of Central Goods and Services Tax Act, 2017 (“CGST Act”) and Maharashtra Goods and Services Tax Act, 2017 (“SGST Act”) on the question of law as to:

Q.1. Whether input tax credit is available of the GST paid on expenses incurred towards promotional schemes of Shubh Labh Loyalty Program or goods given as brand reminders?

GST Provisions

i. Before analyzing the eligibility of ITC on the type of products as mentioned above, the following are key provisions from CGST Act, 2017 which are significant to determine the eligibility of the credit –

(a) Section 2(59) of CGST Act, 2017 – “input” means any goods other than capital goods used

or intended to be used by a supplier in the course or furtherance of business

(b) Section 2(60) of CGST Act, 2017 – “input service” means any service used or intended to

be used by a supplier in the course or furtherance of business

(c) As per Section 16(1) of the said Act – “Every registered person shall, subject to such conditions and restrictions as may be prescribed and in the manner specified in section 49, be entitled to take credit of input tax charged on any supply of goods or services or both to him which are used or intended to be used in the course or furtherance of his business and the said amount shall be credited to the electronic credit ledger of such person”

Thus, credit is available for input tax paid on goods which are used for the furtherance of business.

However, as per Section 17(5)(h) of the CGST Act, 2017, “input tax credit shall not be available in respect of the following, namely: goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples.” As per the above provision, credit is not available for goods which are given as a gift and free samples.

ii. As mentioned above, in the case of brand reminders, products like pens, notepad, key chains, etc. are distributed to the distributors and doctors. The said products are embossed with Sanofi brand. The brand embossed on this product serves as an advertisement tool and is a brand reminder. Such goods act as a reminder of the association with the brand Sanofi so as to promote sales. The exhaustive list of goods distributed as brand reminders is enclosed as ‘Annexure II’.

iii. As per the provisions of the CGST Act as highlighted above, every registered person is entitled to take credit of input tax charged on any supply of goods or services or both to him which are used or intended to be used in the course or furtherance of his business.

iv. In the present case, the brand reminders are provided to the wholesalers in furtherance At business so as to promote Sanofi brand and its products. Thus, ITC should be allowed of ~ the GST paid on procurement of such products which are given to wholesalers as brand reminders. However, Section 17(5) of the CGST Act covers gifts for the purpose of ineligible credit.

v. Ona plain reading of the aforesaid provisions it can reasonably be concluded that ITC has to be reversed with respect to any goods disposed of by way of gift or free samples. However, it is important that the ambit and scope of “gifts” are understood properly.

vi. ‘Gift’ has not been defined under the CGST Act. Hence, reference will have to be made to other statutes and the jurisprudence available on the same. Gift, as per the Gift-Tax Act (18 of 1858) has been defined to mean transfer by one person to another of any existing movable or immovable property voluntarily and without consideration in money or money’s worth.

Further reference can be made to the definition of gift in Corpus Juris Secundum, Volume 38, referred with approval by the Honourable Supreme Court in the case of the case of Sonia Bhatia v. State of UP [1981 (3) TMI 250 – Supreme Court], wherein “gift” has been held to be a voluntary transfer of property by one to another, without any consideration or compensation therefor. A ‘gift’ is a gratuity and an act of generosity and does not require a consideration; if there is a consideration for the transaction, it is not a gift. In the same case, it was also held that a gift is a transfer which does not contain any element of consideration in any shape and form – Love, affection, spiritual benefit, and many other factors may enter in the intention of the donor to make a gift but these filial considerations cannot be called or held to be legal considerations as understood by law.

vii. The Australian High Court in the case of Commissioner of Taxation (Cth) v. McPhail [1968] 41 ALJR 346 held that to constitute a “gift” the property should be transferred voluntarily and not as a result of a contractual obligation. In this case a person agreed to give a donation to a school in return of school charging less fees for the education of the child of said person. Hence, the Court held that such donation cannot be termed as “gift” as it was made under a contractual obligation wherein school was required to charge lower fees against the donation made.

viii. In light of the above, one can reasonably conclude that to constitute a “gift” following elements are required to be satisfied:-

a. Supply must be made without any contractual obligation. If any supply is made under a contractual obligation it cannot be termed as a ‘gift’.

b. Supply must be made without any consideration in money or money’s worth.

Hence, supplies made out of love and affection or such other non- legal considerations can only be termed as ‘gifts’.

ix. Based on above, it is important to understand whether the brand reminders given by Sanofi free of cost to its wholesalers can be considered as a gift and thus, ITC of GST paid on the said products will be disallowed. The sample invoices for procurement of such products distributed as brand reminders are

enclosed as Annexure III.

x. As we have noted before, it is a settled law that “A “gift” is a gratuity and an act of generosity”. Given Indian traditions, Diwali gifts should more or less qualify as a ‘gift’ within that definition and thus necessitate credit reversal. However, the company may often give out various kind of articles like diaries, pen sets, calendars, paperweights, injection boxes, etc. embossed with the bold logo of its brand name/ product name so that the recipient remembers the brand of the company. Such articles would typically be low-cost articles which bear the name of the company and are purely for the promotion of its product/ brand. Clearly, giving of such articles cannot be said to be ‘a gratuity’ or ‘an act of generosity’ and to that extent, input credit vis a vis such expenses, it can be argued, does not need to be reversed.

xi. The Company is of the view that the products distributed to its wholesalers are for their brand and are in furtherance of business and thus, ITC of the GST paid on such products should be

available.

xii. The Oxford dictionary has defined the term “promotion” as an activity that supports or encourages a cause, venture or aim, the publicizing of a product, organization “of venture so as to increase sales or public awareness. Further, the term “furtherance” is defined as the advancement of a scheme or interest. In context of the term “furtherance of business” it means advancement of business of the company.

xiii. The meaning of supply made in course or furtherance of business given in the FAQ on GST released by CBEC says – No definition or test as to whether the activity is in the course of furtherance of business has been specified under the CGST Act. However, the following business test is normally applied to arrive at a conclusion whether a supply has been made in the course or furtherance of business:

a. Is the activity, a serious undertaking earnestly pursued?

b. Is the activity, pursued with reasonable or recognizable continuity?

c. Is the activity, conducted in a regular manner based on sound and recognized business principles?

d. Is the activity, predominantly concerned with the making of taxable supply for

consideration/ profit motive?

xiv. Accordingly, when the inputs and/ or input services are said to be used in furtherance of business, the use of such supplies should help in achieving the objectives of the business in a better and effective way,

thus corresponding credit is allowed. In the present case, the brand reminders are given to wholesalers with an intention to increase sales of the Company and thus given for promoting the brand and advancement of the business which is the primary objective.

xv. It is pertinent to note that, if promotional items are considered as gift and the ITC on the same is disallowed, this will have a huge impact across the businesses because in order to promote sales or to create goodwill, the companies carry out various promotional schemes including distributing goods for brand promotion.

xvi. The act of giving free supplies is similar to the promotional and advertising activities undertaken by every business which are the basic ingredients and inevitable. Moreover, when a business makes a free supply, the cost which the business has incurred is always taken into account by him in fixing the price of the rest of supplies. Thus, the business is not forbearing any loss on distribution of such goods to the wholesalers. Albeit-indirectly, the exchequer will get GST even on the value of the free supplies and there is no revenue loss as such to the government as well.

xvii. If business promotion and advertisement expenses are not specifically excluded and are considered as ‘in the course or furtherance of business’ then in view of the applicant same treatment is available for free supplies. Thus, the ITC of the GST paid on goods distributed as brand reminders should be available.

xviii. We also want the highlight entry (1) of Schedule I to the Central Goods and Services Tax Act, 2017 (‘CGST Act’). The said entry in Schedule I to the CGST Act reads the following:

“ ACTIVITIES TO BE TREATED AS SUPPLY EVEN IF MADE WITHOUT CONSIDERATION 1.Permanent transfer or disposal of business assets where input tax credit has been availed on such assets”

xix. In accordance with the aforesaid entry, a view can be taken that since the input tax credit has been availed on acquisition of such products, giving away the same for free to its customers is nothing but permanent transfer or disposal of the business assets.

xx. In this regard, the applicant wishes to submit that the products like pens, notepad, key Chains, etc. given as brand reminders cannot be termed as “business assets”. The term business asset is defined in general term as a piece of property or equipment purchased exclusively or primarily for business use. There are many different categories of assets including current and non-current, short-term and long-term, operating and capitalized, and tangible and intangible. Business assets are itemized and valued on the balance sheet, which can-bé found in the company annual report. The products such as pens, key chains, etc. are purchased and embossed with company logo so as to distribute to its customers for promotion purpose which can be said as incurring business expenses. The same can in no way be said to be permanent disposal or transfer of business assets.

xxi Further, in case of Shubh Labh Loyalty program, as mentioned above, the distributors/wholesaler get promotional items based on the reward points earned on the basis of goods sold by them. Thus, they have earned such reward points on the basis of the target achieved by them.

xxii. In the example provided above, the wholesaler who has earned 24000 points will be eligible for claiming Raymond Weil 2760-St3-50001 Watch -For Men. The said points are earned on the basis of quantity of the Sanofi products sold by the wholesaler. Thus, the rewards in the form of watch given to the wholesaler is on achieving a particular target as per the scheme and is not in the nature of gift. Infact, the wholesaler has earned the said watch on the basis of the sales target achieved.

xxiii. Based on the above, it can be concluded that in case of the Shubh Labh Scheme, the watch given to the wholesaler is not a gift as the watch is given under the contractual obligation under the scheme. It is the consideration for achieving a particular sales target and hence, input tax credit on purchase of the said watch should be available to Sanofi. Further, the said expenditure is incurred in furtherance of business so as to increase the sales.

xxiv. Regarding the point on disposal or transfer of business asset, we would like to state that on a reading of the entry 1 along with the heading of Schedule I, the disposal of the asset 5 should be a standalone/independent transaction being done without consideration – a transaction with consideration

cannot be artificially split to invent an activity without consideration within the aforesaid transaction with

consideration. In the example given above, the ‘free’ item doesn’t seem to be the one which is being disposed off without consideration, negating the applicability of the entry 1 of Schedule 1 to the CGST Act. The watch is earned on the basis of sales target achieved.

xxv. Reference herein can be made to the decision of the Hon’ble first tier tax tribunal in United Kingdom in the case of Marks & Spencer PLC, wherein under an offer M & S was providing “free wine for dine” in 10 pounds. The Tribunal held that when a ‘commercial common sense approach’ is adopted, the term ‘free’ was being used in a marketing sense, but the economic and commercial reality of the offer was that M&S was offering a package of four items for10 pounds, so the price must be allocated across all four items for VAT purposes. In the example given above, the reward in the form of watch given to the wholesaler is on achieving a particular target as per the scheme and is not without any consideration. Thus, no GST should be levied on the said transaction.

xxvi. In addition, we would like to state that even under the erstwhile tax regime, there was no such restriction on availment of input tax credit or cenvat credit on goods purchased for the purpose of distributing the same to customers for promotion in the course or furtherance of business. In this regard, we wish to highlight relevant extracts of the Maharashtra VAT Rule, 2005 and Cenvat Credit Rules, 2004:

a. Rule 52. Claim and grant of set-off in respect of purchases made in the periods commencing on or after the appointed day

(1) In assessing the amount of tax payable in respect of any period starting on or after the appointed day, by a registered dealer (hereinafter, in this rule, referred to as "the claimant dealer") the Commissioner shall subject to the provisions of rules 53, 54,55 and 55B in respect of the purchases of goods made by the claimant dealer on or after the appointed day, grant him a set-off of the aggregate of the following sums, that is to say, –

(a) the sum collected separately from the claimant dealer by the other registered dealer by “way of tax on the purchases made by the claimant dealer from the said registered dealer of goods being capital assets and goods the purchases of which are debited to the profit and loss or, as the case may be, the trading account,

(b) I paid in respect of any entry made after the appointed day under the Maharashtra Tax on the Entry of Motor Vehicles into Local Areas Act, 1987, and

(c)the tax paid in respect of any entry made after the appointed day under the Maharashtra Tax on the Entry of Goods into Local Areas Act, 2003. (d) the purchase tax paid by the claimant dealer under this Act.

(2) The set-off under this rule shall not be granted in regard to any quantum of tax if set-off under rule 51 has been claimed in respect of the same quantum of tax or if set-off has been claimed in respect of the said quantum under any earlier law. ….

b. Rule 2 (a) “capital goods” means:-

(A) the following goods, namely:-

(i) all goods falling under Chapter 82, Chapter 84, Chapter 85, Chapter 90, heading No. 68.05 grinding wheels and the like, and parts thereof falling under heading 6804 of the First Schedule to the Excise Tariff Act;

(ii) pollution control equipment;

(iii) components, spares and accessories of the goods specified at (i) and (ii);

(iv) moulds and dies, jigs and fixtures;

(v) refractories and refractory materials;

(vi) tubes and pipes and fittings thereof; and

(vii) storage tank, used-

1) in the factory of the manufacturer of the final products, but does not include any equipment or appliance used in an office; or

2) for providing output service; a

(B) motor vehicle registered in the name of provider of output service for providing taxable service as specified in sub- clauses (f), (n), (0), (zr), (zzp), (zzt) and (zzw) of clause (105) of section 65 of the Finance Act;

c. Rule 2 (k) “input” means-

(i) all goods, except light diesel oil, high speed diesel oil and motor spirit, commonly known as petrol, used in or in relation to the manufacture of final products whether directly or indirectly and whether contained in the final product or not and includes lubricating oils, greases, cutting oils, coolants, accessories of the final products cleared along with the final product, goods used as paint, or as packing material, or as fuel, or for generation of electricity or steam used in or in relation to manufacture of final products or for any other purpose, within the factory of production;

(ii) all goods, except light diesel oil, high speed diesel oil, motor spirit, commonly known as petrol and motor vehicles, used for providing any output service;

Explanation 1.- The light diesel oil, high speed diesel oil or motor spirit, commonly known as petrol, shall not be treated as an input for any purpose whatsoever.

Explanation 2.– Input include goods used in the manufacture of capital goods which are further used in the factory of the manufacturer; but shall not include cement, angles, channels, Centrally Twisted Deform bar (CTD) or Thermo Mechanically Treated bar (TMT) and other items used for construction of factory shed, building or laying of foundation or making of structures for support of capital goods;

d. Rule 2 (1) "input service" means any service,-

(i) used by a provider of taxable service for providing an output service; or

(ii) used by the manufacturer, whether directly or indirectly, in or in relation to the manufacture of final products and clearance of final products upto the place of removal, and includes services used in relation to setting up, modernization, renovation or repairs of a factory, premises of provider of output service or an office relating to such factory or premises, advertisement or sales promotion, market research, storage upto the place of removal, procurement of inputs, activities relating to business, such as accounting, auditing, financing, recruitment and quality control, coaching and training, computer networking, crédit rating, share registry, and security, inward transportation of inputs or capital goods ‘and outward transportation upto the place of removal;

xxvil. Based on above, the applicant contends even in the erstwhile regime, there was no such restr ction on availment of VAT credit on purchases made for promotion of business. Further, even under Service Tax Law, the cenvat credit was available on purchase of inputs, ihput services or capital goods which were used for furtherance of business. Thus, the input fax credit of the GST paid on purchase of such promotional items should also be available under the GST regime since the same are for furtherance of business.

xxviii, Further, the applicant does reverse the input tax credit wherever it is required by law.

For example: Recently in the applicant’s office they had kept combiflam cream free samples at their reception which can be taken by employees or any visitor to their office. The company has reversed the input tax credit in relation to the same as the free samples given are pure gift in this case and not in furtherance of business. Similarly, the company gives its products to doctors as free samples for which it does reverse the input tax credit.

xxix. Based on above, we request your good self to provide valuable opinion of eligibility of input tax credit in the above cases.

Shubh labh 2018:

Portfolio:

– Combiflam Tablet purchase in minimum quantity of 01 shipper/case or 14,040 tablets will be eligible for 01 reward coupon

– Allegra & Enterogermina purchase value of Rs 3000 will be eligible for 01 reward coupon (MT coupon)

– Combiflam ICY HOT Gel/spray purchase value of Rs 3000 will be eligible for 01 reward coupon ( ICYHOT coupon) 7

– Heritage Range is split into 2 groups- Power Range and Classic Range- Rs 3000 purchase value will be eligible for 01 reward coupon

- Power Brands – Avil Tablets, Dulcoflex, Buscogast Tablet, NU range, and festal

- Classic Brands – Avil Injectibles, Buscogast Injectibles, Soframycin, Combiflam suspension, Seacod and Proctocedyl

Reward Points:

- on activation of one (01) Combiflam coupon, wholesaler will be credited with FIFTEEN (15) reward points and confirmed via text/SMS to registered mobile number

- on activation of one (01) MT coupon, wholesaler will be credited with FIVE (05) reward points and confirmed via text/SMS to registered mobile number

- on activation of one (01) ICYHOT coupon, wholesaler will be credited with TEN (10) reward points and confirmed via text/SMS to registered mobile number

- on activation of one (01)/POWER Brand coupon, wholesaler will be credited with FIVE (05) reward points and confirmed via text/SMS to registered mobile number

- on activation of one (01) CLASSIC Brand coupon, wholesaler will be credited with THREE (03) reward points and confirmed via text/SMS to registered mobile number

Combo Points:

- Additional bonus on purchase of minimum 3 types of coupons in a calendar month will be rewarded to the wholesale account on the 1st day of the subsequent month,

- 10 bonus points will be rewarded to Blue, Silver & Gold. And 20 bonus points will be rewarded to the diamond, platinum and titanium segment

- WS will have to active minimum 3 coupons from Allegra, Power, Combiflam Tab and Icy Hot

SEGMENT BOUNDARY Bonus: Quarterly

Additional Bonus will be rewarded every Quarter to the wholesalers who will maintain the Segment boundary average for each quarter

Combiflam Volume Focus:

- Wholesalers will be rewarded additional bonus of 5 points per case on achieving the 2017 monthly base in addition, wholesalers will be rewarded 10 points per case, on registering the growth in Combiflam Cases on quarterly basis. This will be rewarded Once in a Quarter.

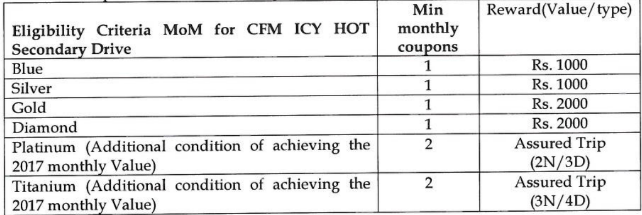

ICY HOT Secondary Focus: Driving Depth and Distribution (Jan May period)

– Wholesalers will be eligible to win assured Gift on achieving the Combiflam ICY HOT minimum purchase slab on monthly basis

- Shubh Labh 2018 is the program for registered Wholesale trade partners only. To confirm your participation for Shubh Labh 2018 you will login www.Shubhlabh.empowerreward.com OR the Shubh Labh Mobile application, and read th Terms and conditions clearly and accept them by/before 30th of Jan 2018. Your login into the program will be ‘active’ only basis your understanding and acceptance of Terms and conditions mentioned below-

Terms and Conditions

I. Program Methodology

- Your registered Mobile number will be your login and user account number for the reward program

- Coupon activation can be done from the registered mobile number/ Mobile application ONLY

- Details about Shubh Labh 2018 program participation, coupon activation, reward points summary will be accessible only on your customized web page of www.shubhlabhempower.com

- Purchase of goods to be done only from authorized locally based Sanofi distributor/s Sales/Good returns till Jan 2019 and confirmed by Sanofi distributor will attract cancellation of equal valued reward points.

- Total Purchase value to be calculated on PTR ( price to the retailer) for the issuance of reward coupons

- No exemption or additional points will be offered in the eventuality of the shortage of any products. Goods available will only be considered for the purchase orders

- Company reserves the right to modify/ discontinue the program at its own discretion

- Number of coupons permitted to be activated in Dec 2018 will remain same/equals to the average number of coupons registered during Jan-Nov 2018 for each of the portfolio types

- Sanofi reserves the right to disqualify the registered wholesaler or withdraw the benefits in the eventuality of involvement in any trade hygiene disturbance in the market/s

- Quarter Definition for each activity will be Jan-Mar, Apr-Jun, Jul-Sep & Oct-Dec

II. Portfolio applicability

- Combiflam Tablet purchase in a minimum quantity of 01 shippers/case or 14,040 tablets will be eligible for 01 reward coupon

- Allegra & Eterogermina purchase value of Rs 3000 will be eligible for 01 reward coupon (NET coupon)

- Combiflam ICY HOT Gel/spray purchase value of Rs 3000 will be eligible for 01 reward cupon ( ICYHOT coupon)

- Power Brands– Avil Tablets, Dulcoflex, Buscogast, NU range, Buscogast Tab and festal-

Rs 3000 Value purchase will be eligible for 01 reward coupon - Classic Brands– Avil Injectibles, Buscogast Injectibles, Soframycin, Combiflam suspension, Seacod and Proctocedyl- Rs 3000 Value purchase will be eligible for 01 reward coupon

III. Reward Coupon Activation

- Reward Coupon Activation Reward coupon will be termed as ‘active” only as and when wholesaler by using the &’unique code’ mentioned on the coupon with dedicated Shubh Labh call center via Toll-Free number of SMS center

- It is solely the responsibility of wholesaler to activate reward coupons of Shubh Labh 2018 via Toll-Free IVR and SMS center Or Shubh Labh Mobile Application

IV. Reward Point accumulation

- On activation of one (01) coupon of “Power Brand”, 5 base reward points will be credited in wholesalers reward account and confirmed via text/SMS to the registered mobile number

- On activation of one (01) coupon of “Classic Brand”, 3 base reward points will be credited in wholesalers reward account and confirmed via text/SMS to registered mobile number – On activation of one (01) coupon of “Allegra/Entero (MT)”, 5 base reward points will be credited in wholesalers reward account and confirmed via text/SMS to the registered mobile number

- On activation of one (01) coupon of ‘Combiflam Icy Hot’, 10 base reward points will be credited in wholesalers reward account and confirmed via text/SMS to the registered mobile number

- On activation of one coupon(01) of Combiflam tab, 15 base reward points will be credited in wholesalers reward account and confirmed via text/SMS to the registered mobile number

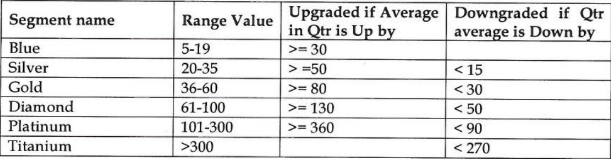

V. Segment Boundary Achievement Bonus- Quarterly

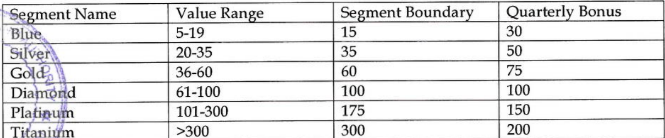

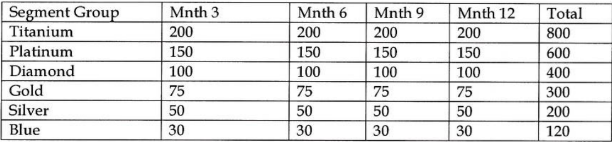

- On maintaining the segment boundary value average during the Quarter, ( Blue: 15,000/- , Silver: Rs 35,000/- Gold: Rs. 60,000/-, Diamond: Rs. 100,000/-, Platinum: 1,75,000/- and Titanium: Rs 3,50,000/-) will be eligible to earn " additional Top up" points of basis the respective segment. ( Blue : 30,Silver: 50, Gold: 75, Diamond: 100, Platinum: 150 and Titanium: 200 reward points)

- Segment boundary value achievement will be calculated Only for the Sell in of Combiflam, Power and Classic brands. Value of Allegra/Enterogermina & Cfm Icy Hot will not be considered for the segment boundary value calculation

- Segment Boundary Achievement bonus will be as mentioned below:

- Any quarter where wholesaler does not activate Reward coupons OR fails to maintain athe average value in a quarter and do not qualify for "segment boundary line" additional Bj | Beard points, will automatically DOES NOT earn Segment boundary based reward Hi. 4 } paints : ‘ j

VI. Combiflam Volume Bonus

- On achievement of SL 2017 monthly base of coupon volume for Combiflam tab, wholeseller will be eligible to earn 05 Bonus reward point every month. If Base is ZERO (“0”), No Bonus will be rewarded and Only Base points for each coupon activated will be credited to the account of wholesaler

- WS will be eligible to earn an additional 10 (Ten) reward points per Combiflam case purchased in a quarter If he/she registers growth over 2017 Qtrly base. (Qtr 2018 purchase – Qtr 2017 purchase), in terms of Coupon activation of Combiflam brand, 10 points per case will be rewarded

- If Qtr 2017 base is Zero (“0”), no bonus will be rewarded and wholesaler will be credited only the base points on each coupon activated

- The wholesaler will be able to earn the quarterly bonus even if miss on the monthly base achievement.

VII. Dynamic Segmentation

- Wholesaler will have the flexibility / option to Outperform and get upgraded to the next segment. This will be calculated on quarterly performance for each wholesaler.

- Upgrade of segment will be done Only to the very next segment irrespective of the Over performance

- Similarly, in event of Low performance in a quarter, wholesaler will get downgraded to the segment below.

Segment wise benefits will be applicable to every wholesaler basis the segment in which he/she is in. No additional bonus/arrear will be credited in case of upgrade and similarly in case of downgrade, no penalty will be charged.

VIII. Combo Bonus

- The wholesaler will be eligible to earn the additional bonus in case of purchase of any 3 types of coupons in a month, which are out of the mentioned 4- Combiflam tab, Combiflam Icy Hot, Allegra/Entero and Power Brands

- Combo bonus will be segment based- Blue, Silver and Gold segment will be eligible to earn 10 reward bonus points and Diamond, Platinum, and Titanium segment will be eligible to earn 20 bonus reward points on a monthly basis if the criteria are fulfilled.

IX. Redemption & Rewards

- Wholesaler basis his/her accumulated reward points can choose to redeem every month, quarter or at the end of program period i.e after 16th of Dec 2018.

- Redemption Request to be sent only through Website/ Mobile application

- Redemption in the form of gift items/articles will be ONLY as per the shubh Labh program catalogue provided to wholesaler.

- Sanofi India does not give any warranty/guarantee in respect of quality or merchantability of the gift articles offered under this program

- Gift articles shown in the catalog are subject to availability and images are for indicative purpose only

- Redemption will be conducted only in the form of gift items listed on the catalogue and NO form/type/kind of conversion into cash or cash equivalent will be permitted unless “deemed fit by Sanofi.

- Reward coupons to be collected Only from Sanofi representatives.

- As per the catalogue both International Domestic trip will be held basis- (a). Passport ‘will be individual wholesalers responsibility (b.) Sanofi does not/will not arrange for local transportation till the airport ( c) For both International and Domestic trips, sanofi will provide only economy class air tickets/2nd ac train tickets (d) Both International/domestic tour packages will not include excess luggage/ laundry/ ISD/STD Calls/Individual personal expenses (e). Both Domestic/ International tour will be held only basis below mentioned periods- Option 1: March- April 2017, Option 2: July- Aug 2017, Option 3: Sep-Oct 2017 Option 4: Feb-March 2018. (f) International trips will be arranged from the select HUBs only and NO travel cost will be given to reach the flying hub. Hubs will be Delhi/ Mumbai/Kolkata/Chennai. (g) Sanofi will not arrange for any accommodation in case of Transit delays/ waiting time or layover time. (h) The itinerary of the international package will start from the Flying Hub and end there only.

- Sanofi does not/will not take responsibility for arranging or confirming additional package requests even on a self-pay basis

- Sanofi reserves the right to disqualify/ withdraw the winner from the international trip in case of any hygiene issues. Only the applicable wholesaler will be allowed to travel on the trips and NO replacement will be entertained in the Lucky draw trips. in case of redemption of Trip, Wholesaler is free to nominate any person to go on the trip.

- Wholesaler shall be free not to avail of the program benefit and purchase goods less than the minimum quantity and Company shall be bound to supply such quantity ordered.

X. Shubh Labh Corner: Shelf Display

- Hiring the Window/Shelf at wholesale points of Mandi type towns Only.

- The wholesaler will have to accept the conditions and give his consent to provide a shelf (selected by Sanofi FF) exclusively for Sanofi CHC OTC in shop visibility activity. The photo will be uploaded on the Shubh Labh dashboard and the wholesaler will be credited 100 reward points on a monthly basis.

- Wholesaler point will be selected by the local Sanofi FF/CSM basis the customer footfall and the visibility of the Shel

- WS will not use that shelf for any other stocking except CHC OTC portfolio or activity

Additional submissions

- The Applicants herein were granted a hearing with regards the captioned application on 9 April 2019 by the Hon’ble Bench. On completion of the hearing the Hon'ble Members were pleased to grant liberty to the Applicants to file written submissions.

- At the outset, The Applicants repeat, reiterate and confirm what is stated in the said Application and pray that the same may be treated as part of this Written Submissions.

- In addition, the Applicants wish to place on record the following grounds:

(a) At the outset, recently a Circular bearing No. 92/11/2019-GST dated 7 March 2019 for clarifying various doubts related to the treatment of sales promotion schemes under GST has been issued by the Principal Commissioner GST. A copy of the said Circular dated 7 March 2019 is attached herewith as Annexure ‘I’.

(b) Under the said Circular Part ‘C’ deals with Buy more, save more offers. It has been clarified in the Circular that discounts offered by the Suppliers to Customers (including staggered discount under ‘Buy more, save more’ scheme and post supply/volume discounts established before or at the time of supply) shall be excluded to determine the value of supply provided they satisfy the parameters laid down in sub-section (3) of Section 15 of the said Act, including the reversal of ITC by the recipient of the supply as is attributable to the discount on the basis of document(s) issued by supplier.

(c) It is clarified in the Circular, that the supplier is entitled to avail the ITC for such input, input services and capital goods used in relation to the supply of goods or services or both on such discounts.

(d) The Applicants submit that the Shubh Labh Loyalty Scheme run by them as an incentive to their distributors/wholesalers is on similar if not identical lines.

(e) Instead of opting to give a cash discount to their distributors/wholesalers, the Applicants to make it more lucrative and aesthetically appealing, offer reward points against purchases made by the distributors/ wholesalers.

(f) The reward points attributed to distributor/wholesaler can be redeemed by them at the end of each month/quarter/year as they may wish to do.

(g) The Applicants have annexed to the Application a catalog from which the distributor/wholesaler can redeem the points so accumulated by them against the items available in the catalog.

(h) The Applicants humbly submit that it is pertinent here to note that it is completely the choice of the distributor/ wholesaler to choose any item from the catalog against the points so accumulated by them.

(i) The Applicants would like to place on record, one unique aspect of the Shubh Labh Loyalty Scheme, i.e. an Application, which has to be downloaded by the distributor/wholesaler or login through the Shubh Labh website. A unique login id and a password are generated, only after which the distributor-wholesaler can log-in and redeem the points accumulated.

(J) Another unique aspect here is that before logging into the Shubh Labh website/ app, a page of terms and conditions pop up which have to be accepted before they get accesses to the website/app. (k) The Applicants are emphasizing on this to establish that the acceptance of terms and conditions on the website/app creates a contractual obligation between the distributor-wholesaler and the Applicants herein.

(K) In fact, the Applicants would like to submit that in light of the terms and conditions which the

distributor/wholesaler accept and a contractual obligation is created between the Applicants and the

distributor/wholesaler which would enable either party to a take recourse to a civil suit or action for specific

performance of contract on failure to adhere to the terms and conditions. A copy of the PowerPoint presentation explaining the functioning of the Application is attached herewith as Annexure ‘2’.

(m) The Applicants submit that in light of the aforementioned submissions, it is contended that the articles given by the Applicants through the Shubh Labh Loyalty Scheme are in the furtherance of business and not in the manner of gift. Thus, the Applicants submit that they would be eligible to input tax credit under Section 16(1) of the CGST Act, 2017 and not hit by the bar of Section 17(5)(h) of the CGST Act, 2017.

(n) The Applicants further submit that the recent decision of the Maharashtra Authority for Advance Ruling in the case of Biostat India Limited dated 20 December 2018 would not have any bearings in the present application for the following reasons:

° In the judgment of Biostat India Limited, the AAR held that the Applicant therein failed to submit any documentation to prove that there was a contractual obligation. (in the present facts, the Applicants have reproduced in their application the entire terms and conditions, which the distributor/ wholesaler has to accept as a pre-requisite before redeeming their points)

- In the judgment of Biostat India Limited, there were only gold coins on offer on purchase of a certain quantity of seeds (in the present facts, the choice has with the distributor/ wholesaler to redeem the points garnered by him against articles of his choice)

° The transaction between the Applicants and the distributor/ wholesaler is not a barter as envisaged under Section 7 of the CGST Act. The transaction of buying medicines by the distributor/ wholesaler is a pure sale transaction, in which the medicines are supplied against payment of money. A barter would involve trading of goods against goods or goods against services or various other permutations and combinations. However, the present transaction by any stretch of imagination cannot be called a barter and is a pure sale arrangement.

Me. As pleaded earlier, the act of giving points which can be redeemed later against articles is nothing but discounts in the line of “buy more, save more” on which input tax credit is available.

° It would defeat the very purpose of Section 16(1) of the CGST Act ifit is held that where the goods are procured with levy of input tax and are supplied without tax being paid on such output supplies, the scheme of the CGST Act, provides for no input tax, except export. Infact, Section 16(1) specifically provides that ITC would be available on inputs if they are used or intended to be used in furtherance of business. Any interpretation to the contrary would render Section 16(1) of the CGST Act otiose.

° Further the circular dated 7 March 2019 referred above in regard to treatment of sales promotion schemes was not considered in the said ruling as order was issued prior to issuance of circular.

° In light of these facts, the Applicants humbly submit that they should be entitled to ITC on GSTpaid on expenses incurred towards promotional schemes of Shubh Labh Loyalty Programme and goods given as brand reminders.”

3 CONTENTION – AS PER THE CONCERNED OFFICER:

The submission, as reproduced verbatim, could be seen thus-

The applicants above referred an application under Section 98 of the Central Goods and Service Tax Act, 2017 read with Rule 104 of CGST, Rules 2017. The applicants are registered within the jurisdiction of respondents under GSTIN no 27AAACH2736F1ZU. The Applicants has filed the subject application for advance ruling on the following questions:

Whether input tax credit is available on the GST paid on expenses incurred towards promotional schemes of Shubh Labh Loyalty Program?

Comments:- No, it is observed that applicant and its group entities are a supplier of Pharmaceutical goods and services. Under Shub Labh Trade Royalty Program, the applicant claims that they offer free Singapore Trip or Raymond Weil Watch as the case may be to their wholesalers on selling a pre-determined quantity of their pharma product and the said predetermined quantity is accounted for by way of reward points. In this way, there is not dispute about the fact that applicant do not charge any price or value for the said free supply in terms of free Singapore Trip or Raymond Weil Watch as the case may be. Therefore, the said free supply is not taxable and chargeable to any GST in terms of Section 9 of the CGST Act, 2017. The said supply merit as “exempt supply” in terms of provisions of Section 2(47) read with Section 2(78) and therefore, any ITC is not available on the same in terms of inter-alia provisions of Section 17(2) of the CGST Act, 2017. Further provisions of Section 17(5)(h) specifically disallow availment and usage of any credit on goods disposed of by way of ‘gift! not withstanding anything whatsoever in sub section (1) of Section (16). Therefore, the question of availment of ITC, on the basis that subject gift were used in furtherance of their business, does not arise.

1.1 The applicant’s reliance on provisions of Schedule-I is totally misplaced because it is not their case that subject gift are covered by Schedule-I of the CGST Act, 2017. It may be seen that Schedule-I is applicable to only specified suppliers and the subject gifts by the applicant are not covered by the provisions of Schedule-I. Therefore, the applicant has no occasion to take ITC on the basis of Schedule-I which is irrelevant in their case. Applicant themselves agreed that the subject supply cannot be construed as permanent transfer or disposal of the business assets.

1.2 There is no substance in the applicant's contention that Watch given under their

Subh Labh Royalty Scheme does not merit as Gift because there is no dispute about the fact that even watchés has been given free of cost. The applicant themselves have quoted the judgment of Hon’ble Supreme Court in case of Sonia Bhatia Vs. State of UP [1981(3) TMI 250 – Supreme Court), wherein Hon’ble Supreme Court has held that a ‘gift’ is a gratuity and an act of generosity and des: not require consideration, it there is a consideration for one transaction, it is not gift’

1.2.1 The applicant is not signing any formal contract under Shubh Labh Loyalty Program, hence there is no contractual obligation under which goods are supplied.

1.2.2. In the instant case under Shubh Labh Loyalty Program, gifts like watch or reward points are given as incentive and there is no extra commercial consideration and hence since there is no commercial value assigned to the transaction it is to be construed to be Gift.

1.2.3 The applicant themselves have submitted that for anything to be considered as gift, there should not be any contractual obligation or involvement of consideration. In the instant case the applicant give free goods to wholesalers without any involvement of consideration nor is there any written contractual agreement between the company and the wholesaler. Hence, the same is to be considered as Gift. The loyalty program are given voluntarily by the Company and there is no consideration involved in the transaction. Hence it falls in the definition of Gift.

1.3 In any case, the notice is not eligible for ITC in terms of provisions of section 9(1) read with Section 17(2), Section 2(47) and section 2(78), because, there is no dispute that the applicant has made the subject supplies without any consideration on which they have paid any GST. Therefore, the value of subject free supply does not merit inclusions in value in terms of Section 15. Further, the subject supplies merit as exempt supplies of Section 2(47) and hence, the ITC is not available to applicant in terms of Section 17(2). Therefore, it may be seen that ITC is not available even without application of the provisions of Section 17(5)(h).

1.4. The applicant has contended that subject free supplies have been made in pursuance of their business. However, the fact remains that the same have been made free of cost and therefore, the same are nontaxable under Section 9 read with Section 2(78) and merits exempted supply under Section 2(47). Further, there is no provisions under Section 15 to include the cost of such free supplies in the value of taxable free samples in terms Section 15. There cannot be any dispute that the said supplies are exempted, hence credit is not allowed in terms of Section 17(2). Further, gifts has to be disallowed in terms of Section 17(5)(h) notwithstanding the fact that the subject supply has been used in course of furtherance of business in terms of Section 16(1). The provisions of Section 17(5)(h) are applicable notwithstanding the provisions of Section 16(1). Therefore, the applicant is not eligible for the ITC.

1.5 Further, the applicant has not provided any enclosures to their application including Annexure-I containing a catalog of “Subh Labh Loyalty Program’. Therefore, the department reserves the rights to be provided with all the documents and file an additional reply.

2, Whether input tax credit is available of the GST paid on expenses incurred towards promotional goods given as brand reminders?

Comments: No, it is observed that applicant and its group entities are a supplier of Pharmaceutical goods and services. Under promotional goods given as brand reminders, the applicant distribute the products like pens, notepad, key chains etc. to the distributors and doctors. The said products are embossed with Sanofi brand. In this way, there is not dispute about the fact that applicant do not charge any price or value for the said free supply in terms of free pens, notepad, key chains etc. as the case may be. Therefore, the said free supply is not taxable and chargeable to any GST in terms of Section 9 of the CGST Act, 2017. The said supply merit as ‘exempt supply’ in terms of provisions of Section 2(47) read with Section 2(78) and therefore, any ITC is not available on the same in terms of inter-alia provisions of Section 17(2) of the CGST Act, 2017. Further provisions of Section 17(5)(h) specifically disallow availment and usage of any credit on goods disposed of by way of ‘gift’ notwithstanding anything whatsoever in subsection (1) of Section (16). Therefore, the question of availing of ITC, on the basis that subject gift were used in furtherance of their business, does not arise.

2.1 The applicant’s reliance on provisions of Schedule-I is totally misplaced because it is not their case that subject gifts are covered by Schedule-I of the CGST Act, 2017. It may be seen that Schedule-I i is applicable to only specified suppliers and the subject gifts by the applicant are not, covered by the provisions of Schedule-I. Therefore, the applicant has no occasion to take ITC on the basis, of Schedule-I which is irrelevant in their case.

Applicant themselves agreed that the subject supply cannot be construed as permanent transfer or disposal of the business assets.

2.2 There is no substance in the applicant’s contention that pens, notepad, key chains etc. given under their promotional schemes goods given as brand reminders does not merit as Gift ‘ because there is no dispute about the fact that even pens, notepad, key chains, etc. have been given st free of cost. The applicant themselves have quoted the judgment of Hon’ble Supreme Court in

“case of Sonia Bhatia Vs. State of UP (1981(3) TMI 250 – Supreme Court], wherein Hon’ble Supreme Court has held that a “ gift is a gratuity and an act of generosity and does not require consideration, it there is a consideration for one transaction, it is not gift

2.2.1 The applicantis not signing any formal contract under promotional goods given as brand reminders, hence there is no contractual obligation under which goods are supplied.

2.2.2 In the instant case under promotional goods given as brand reminders, products like pens, notepad, key chains etc. are distributed to the distributors and doctors. The said products are embossed with Sanofi brand are given as incentive and there is no extra commercial consideration and hence, since there is no commercial value assigned to the transaction, it is to be construed to be Gift.

2.2.3 Also it is seen that there is no contractual obligation involved in this situation, as it is completely up to the distributors and doctors whether he will prescribe the medicines of the company or not. Doctors are not under any legal obligation to do so. As the consideration is not directly linked with the gift provided to doctors, it is to be considered as gift.

2.24 The applicant themselves have submitted that for anything to be considered as gift, there should not be any contractual obligation or involvement of consideration. In the instant case the applicant give free goods to distributors and doctors without any involvement of consideration nor is there any written contractual agreement between the company and the distributors and doctors. Hence, the same is to be considered as Gift.

2.2.5 The goods given as brand reminders are given voluntarily by the Company and there is no consideration involved in the transaction. Hence it falls in the definition of Gift. Also it is seen that there is no contractual obligation involved in this situation, as it is completely up to the doctors whether he will prescribe the medicines of the company or not. Doctors are not under any legal obligation to do so. As the consideration is not directly linked with the gift provided to doctors, it is to be considered as gift.

2.3 In any case, the notice is not eligible for ITC in terms of provisions of section 9(1) read with Section 17(2), Section 2(47) and section 2(78), because, there is no dispute that the applicant has made the subject supplies without any consideration on which they have paid any GST. Therefore, the value of subject free supply does not merit inclusions in value in terms of Section 15. Further, the subject supplies merit as exempt supplies of Section 2(47) and hence, the ITC is not available to applicant in terms of Section 17(2). Therefore, it may be seen that ITC is not available even without application of the provisions of Section 17(5)(h).

2.4 The applicant has contended that subject free supplies have been made in pursuance of their business. However, the fact remains that the same has been made free of cost and therefore, the same are nontaxable under Section 9 read with Section 2(78) and merits exempted supply under Section 2(47). Further, there is no provisions under Section 15 to include the cost of such free supplies in the value of taxable free samples in terms Section 15. There cannot be any dispute that the said supplies are exempted, hence credit is not allowed in terms of Section 17(2). Further, gifts have to be disallowed in terms of Section 17(5)(h) notwithstanding the fact that the subject supply has been used in course of furtherance of business in terms of Section 16(1). The provisions of Section 17(5) (h) are applicable notwithstanding the provisions of Section 16(1). Therefore, the applicant is not eligible for the ITC.

2.5 Further, the applicant has not provided any enclosures to their application including Annexure-III containing the sample invoices for procurement of such products distributed as brand reminders. Therefore, the department reserves the rights to be provided with all the documents and file an additional reply.

3. The additional requirements as per annexure are marked as Exhibit A to the submission.

PRAYER

Considering the facts discussed in forgoing paras it is humbly prayed that the application filed bythe applicants may not be allowed.

04. HEARING

The Preliminary hearing in the matter was held on 26.02.2019, Sh. Deshmukh Advocate for Advaita Legal, appeared and requested for admission of application as per contentions made in their application Jurisdictional Officer Sh. Mohan Raut, Supdt., appeared.

The application was admitted and called for final hearing on 09.04.2019, Sh. Deshmukh Advocate for Advaita Legal, appeared, made oral and written submissions. Jurisdictional Officer Sh. Mohan Raut, Suptt., appeared and made written submissions. We heard both the parties.

5. OBSERVATIONS AND FINDINGS:

We have gone through the facts of the case, written contention of both the parties, and

documentary evidences submitted on record. The issue put before us is in respect of admissibility of Input tax credit (ITC ) paid or deemed to have been paid on supply used as a sales promotion or brand expenses by the applicant which would be on the lines thus –

The applicant, a registered person under GST ACT is engaged in the business of sale of pharmaceutical goods and services through group entities during the course of which they incur various marketing and distribution expenses, with a view to promote their brand/ products and to enhance their sales under various schemes. The applicant distributes the different type of products among its trade channels as promotional items or brand reminders.

Applicant offers various promotional schemes and following schemes are the subject matter of present application namely:

1) Shubh Labh trade loyalty program and

2) Brand reminders products

The Broad nature of the schemes are as below:

Shubh Labh trade loyalty program: wherein the distributors/wholesalers get rewards based on the reward points earned by them on the basis of the quantity of goods sold by them. Instead of opting to give a cash discount to their distributors/wholesalers, and to make it more lucrative and aesthetically appealing, the applicant offers reward points against purchases made by the distributors/ wholesalers. These reward points can be redeemed at the end of each month/quarter/year as they may wish to do. The Applicants have annexed to the Application a Catalogue from which the distributor/wholesaler can redeem the points so accumulated by them again the items available in the catalog and it is completely the choice of the distributor/ wholesaler to choose any item from the catalog against the points so accumulated by them.

Brand reminders products: In this scheme products like pens, notepad, key chains, etc. are “attributed to the distributors or doctors with their name embossed on it to promote the brand and sales. For the supply of promotional products, applicant procured such goods by payment of tax and uses it in the course of business or furtherance of business as aforesaid. In this view applicant is asking availability of ITC paid on the goods or services procured and used for the promotional scheme. Therefore, they are seeking clarifications answers on the following questions are as below:

Question 1. Whether input tax credit is available of the GST paid on expenses incurred towards promotional schemes of Shubh Labh Loyalty Program?

Question: – 2. Whether input tax credit is available of the GST paid on expenses incurred towards

promotional schemes goods given as brand reminders?

Since both the question involved a common point of determination, hence taken together for decision in this proceeding as below:

We find that the applicant is mainly dealing and supplying of Pharmaceutical goods and services and in order to achieve sales and marketing objectives, they have launched various target based – sales incentive schemes for their distributors/wholesalers to achieve a specified target and in turn helps the company to achieve their targets. The present subject application is in respect of a sales promotion scheme known as “Shubh Labh Loyalty Program 2018″ and promotional products which has been floated by them for their customers. In the first case, their distributors/ wholesaler Customers who purchased certain products over and above a certain quantity would be entitled to get reward points. In the second scenario, applicant is giving Brand reminder products like pens, notepad, key-chains to the distributors or Doctors, which serve as an advertisement tool. The brand reminders are distributed to the distributors or doctors with their name embossed on it to promote the brand for sales. In the first scheme, the applicant sells their products to their customers who are entitled to get the reward points, on the basis quantity of goods sold by them. Both the schemes are independent of each other. In the first schemes, the products mentioned in the catalog will be procured from different suppliers, it includes different types of goods and services and since these goods /services are leviable to GST, the applicant has raised the question i.e. whether Input Tax Credit (“ITC”) can be claimed by them on procurement of the said products/services given on above said promotional basis. As per their submissions, the said products are inputs for them and GST levied on such purchase qualifies to be an input tax for the purpose of Section 16(1) read with Section 2(62) of the CGST

Act.

The jurisdictional officer has also made submissions and has a different viewpoint. He has opined that in the instant case under Shubh Labh Loyalty Program, gifts like watch or Reward Points are given as incentive and there is no extra commercial consideration and since there is no commercial value assigned to the transaction, it is to be construed to be Gift. He farther contended that under promotional goods given as brand reminders, products like pens, notepad, key chains, etc. are distributed to the distributors and doctors. The said products are embossed with Sanofi brand are given as incentive and there is no extra commercial consideration and hence, since there is no commercial value assigned to the transaction, it is to be construed to be Gift.

Taking into account applicant’s contention that the subject free supplies have been made in pursuance of their business, jurisdictional officer submit that the fact remains that the same have been made free of cost and therefore, the same are non-taxable under Section 9 read with Section 2(78) and merits to be treated as exempt supply under Section 2(47). Further, there are no provisions under Section 15 to include the cost of such free supplies in the value of taxable free samples. There cannot be any dispute that the said supplies are exempted hence credit is not allowable in terms of Section 17(2). Further, gifts has to be disallowed in terms of Section 17(5)(h), notwithstanding the fact that the subject supply has been used in course of furtherance of business in terms of Section 16(1). The provisions of Section 17(5) (h) are applicable notwithstanding the provisions of Section 16(1). Therefore, the applicant is not eligible for the ITC as the promotional products/services to be distributed as mentioned above, are not inputs and hence, GST paid on such a purchase does not qualify to be an input tax for the purpose of Section 16(1) read with Section 2(62) of the CGST Act 2017. He further found that the products are not inputs because the said Distribution of different products are not in line with the basic business model, the same products are not essential for continuity in supply and the distribution of products are not concerned with the making of taxable supply for consideration unless the distribution is looked as a hidden discount.

We find that the applicant has floated the subject scheme for the period from 2018 to Jan 2019 only, by way of which reward points which are linked with different products would be given to those customers who lifted a certain quantity of Pharmaceutical goods. The basic condition is to purchase a certain quantity of products and sale thereof. Thus it is seen that only those specific customers who fulfill the conditions would be able to avail the benefit of the subject scheme of “Shubh Labh Loyalty Program”. The applicant has submitted that the said products procured for the distribution to the wholesalers are inputs for them and GST levied on such purchases qualifies to be an input tax for the purpose of Section 16(1) read with Section 2(62) of the CGST Act.

We find that the provisions of ITC are governed by Sections 16 and 17 of the CGST Act, 2017. In.order to avail ITC, two basic provisions need to be complied with, i.e. Section 16 and Section! 1Z.' As per Section 16, a taxpayer is entitled to take credit of input tax charged on any supply of goods or services to him which are used in the course or furtherance of his business. ie. skis section disallows ITC against input goods/services used for non-business purposes. Section 17 (5) of the CGST Act deals with Blocked credits and begins with a non-obstante clause, which means even if Section 16 (1) allows ITC, Section 17(5) shall block in respect of certain cases.

Clause (h) of Section 17(5) read as,

“Notwithstanding anything contained in sub-section (1) of section 16 end sub-section (1) of section 18, input tax credit shall not be available in respect of goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples.

We will therefore first discuss whether the different promotional products in the present case can be treated as a gift or not. The word “gift” has not been defined in the CGST Act. However, the Gift-Tax Act (18 of 1858) has defined the word gift to mean transfer by one person to another of any existing movable or immovable property voluntarily and without consideration in money or money’s worth. It is seen from the definition that the transfer i.e. the gift given in such a case has to be voluntary. The applicant has submitted that they have a contractual arrangement with the customer wherein if he purchases certain amount of company’s product and uploads details of information by customer login on the companies prepared software on the website wherein specific terms and conditions are mentioned for the participation in the Subha Labha Loyalty scheme, then he will be said to have accepted the terms and conditions and is entitled to a promotional products on the basis of reward points attributed on monthly / quarterly / yearly basis. A contractual arrangement implies especially in view of the magnitude and area of the applicant’s business that, it should also be agreed by the customer in writing to such scheme floated by the applicant. We find that they have not submitted any such contract/agreement and in support of their contention, but they have only submitted a scheme of Shubh labh Loyalty is available on companies web site and interested customers can Login with details to avail the benefit of scheme from 2018 to Jan, 2019. Hence we find that the promotional products are not given to their customers under any contractual obligation and are voluntarily given on certain conditions achieved by their customers.

In the present scenario we will try to understand the word ‘gift’ in the common parlance as it is also used in the present day. There are several schemes advertised in the market by business houses which promise to give ‘assured gifts’ to their customers, for eg. In the city of Mumbai and its suburbs, various builders had floated advertisements stating that the first x numbers of buyers of flats in their residential construction projects would be given a car/100gms Gold coins, etc. Similarly, malls in Mumbai also offer assured gifts on purchase above certain amounts by their customers. Hence I the present context the word ‘gift’ has an enlarged scope according to us and has its own color. In all such cases, as in the present case, the statement that promotional goods, in this case, will be given to distributors/wholesalers who satisfy certain conditions is nothing but the assurance of giving away gifts on those conditions being achieved by the customers. At the least we can say that the condition put forth by the applicant to avail or participate in this scheme is nothing but is a measure of particular kind of promotional items meaning thereby that if wholesaler sale more products then he will be eligible for more reward points and further eligible for big offer such as Singapore Trip of 5 D/6 Days instead of Raymond Watch.

Under the GST laws the intention for non-granting/denial of setoff is envisaged in situations where there is no tax on output supply. In cases where the goods are procured with levy of input tax and are supplied without tax being paid on such output supplies, the scheme of the GST Act provides no input tax credit, except export.

Schedule – I to the CGST Act, 2017 deals with activities to be treated as supply even if made without consideration. As per Entry Number 2 to Schedule I (2), Supply of goods or services or both between related persons or between distinct persons as specified in section 25, when made in the course or furtherance of business:

Provided that gifts not exceeding fifty thousand rupees in value in a financial year by an employer to an employee shall not be treated as a supply of goods or services or both.

The above provisions and Section 17 (5) (h) stipulate that any goods disposed of, by way of gift are not eligible for ITC and that even if supply is in course or furtherance of business between related or distinct persons, it shall be considered as supply except to the extent of fifty thousand rupees in a financial year, when given by an employer to its employee.

Further under Section 17(5), no ITC on any goods can be availed, if they are given as gifts, whether or not in course of furtherance of business. As a corollary if it is considered that gifts have some commercial consideration, then GST shall be paid at the time of giving away of disposal of the same and in such cases, only ITC will be available. A "gift" is normally seen as an enticement to customers as in the subject case which would bear heavily on the customers in making the purchase of particular quantities and above or in making payments of certain values and above. This act on behalf of the applicant if it is not excluded from the scope of being a supply, then the provisions of the Valuation Rules come into play. In other words, if the giver of the gift does not pay output tax on the same then the compensation to the department would be the foregoing of the ITC on such gifts.

We now deal with one of the contention of the applicant that they have a contractual arrangement with the customer wherein if the distributor purchases certain amount of quantity of company’s product, then he shall be entitled to a get promotional products on the basis of reward point accumulated as per list of catalogue. This can be inferred as if the distributor or wholesaler of the applicant is providing services of increased sale for which consideration is in the foo of a products. As per Section 7 of the CGST Act, disposal, or the case may be, barter, mad& oF agreed to be made for a consideration in the course or furtherance of business is supply is liable to wax. We find in the present application, and as admitted by the applicant that the supply is without consideration i.e. free supply and without payment of output tax. The only conclusion, therefore, that can be drawn in the present case is that the distribution of promotional articles by the applicant is nothing but gifts and hence the transaction is covered by the provisions of Section 17(5) of the Act.

Relying on Circular issued by the Principal Commissioner GST bearing No. 92/11/2019- GST dated 7 March 2019 for clarifying various doubts related to treatment of sales promotion schemes under GST, submits that discounts offered by the Suppliers to Customers (including staggered discount under ‘Buy more, save more' scheme and post supply/volume discounts established before or at the time of supply) shall be excluded to determine the value of supply provided they satisfy the parameters laid down in sub-section (3) of Section 15 of the said Act, including the reversal of ITC by the recipient of the supply as is attributable to the discount on the basis of document(s) issued by supplier. He further submit that as per Circular, supplier is entitled to avail the ITC for such input, input services and capital goods used in relation to the supply of goods or services or both on such discounts. At last Applicants submit that the Shubh Labh Loyalty Scheme run by them as an incentive to their distributors/wholesalers is on similar if not identical lines.

We find that in the case of “ Buy more, save more offers “, the discount is offered on the same transaction of supply made from the supplier even in post supply/Volume discounts established before or at the time of supply and ITC would be applicable on the inputs purchases. But in the present case, the facts are different than the issue clarified in the above said circular. In the subject case, the applicant has not provided any discount on the transaction made to the customers. He has given the reward points on the quantity of goods purchased by the distributors/wholesalers and not on the value of the goods. Against certain accumulated of reward points, the applicant has supplied the promotional products, listed as per the catalog. Scheme explained by the circular and subject matter the present scheme we do not find similarity of facts and as such the said circular is of no help to the applicant.

To sum up ITC on “gifts” will not be available when no GST is being paid on their disposal. Just because the applicant submits that they have satisfied Section 16 (1) of the CGST Act 2017 does not mean that they are entitled to credit sinc Section 17(5) starts with “Notwithstanding anything contained in sub-section (1) of Section 16……..”. The implication is that in the subject case even if it seems, as per the applicant, that Section 16 (1) is applicable in their case and allows them credit, Section 17(5) shall block such credits.

Even though we have come to a conclusion that Input Tax Credit is not available for the expenses Incurred towards promotional schemes such as Shubh Lakh Loyalty Program and Brand Reminder Products, we find paradox in the argument of the applicant that supports our views ‘We want to invite attention to the statements made by the applicant as below: With the respect Shabh Labh Scheme based on the facts appellant submit that the watch given to the wholesaler is not a gift as the watch is given under the contractual obligation under the scheme. It is the consideration for chieving a particular sales target and hence ITC on purchases of the said watch should be available. Further applicant submits that the Brand Reminder are given to wholesaler with an intention to increase the sale of the company. Brand Reminder Products like pens, key note pad, key chains etc. are distributed to the distributers and doctors. The said products are embossed with Sanofi Brand. The Brand embossed on this products serve as advertisement and is a brand reminder that promote sales. Further at submission with heading it is stated as –

ICY HOT Secondary Focus: Driving Depth and Distribution (Jan May period)

• Wholesalers will be eligible to win assured Gift on achieving the Combiflam ICY HOT minimum purchase slab on monthly basis.

Further in the submission with heading it is stated as –

IX Redemption & Rewards

– Redemption in the form of gift items/articles will be ONLY as per the Shubh Labh program catalogue provided to wholesaler.

– Sanofi India does not give any warranty/guarantee in respect of quality or merchantability of the gift articles offered under this program

– Gift articles shown in the catalog are subject to availability and images are for indicative purpose only

– Redemption will be conducted only in the form of gift items listed on the catalog and NO form/type/kind of conversion into cash or cash equivalent will be permitted unless

deemed fit by Sanofi.

From the above contradictory submission of the applicant, if we accept the contention of the applicant that the promotional items are supplied as a contractual obligation e.g. watch is given under the contractual obligation under the scheme with an intention to increase the sale of the company, serve as an advertisement tool and brand reminder to promote sale, then in view of section 7 of the GST Act it is a supply in the nature of barter ie. supply of promotional goods against supply of services such as increased sale, advertisement of products and sales promotion. On the contrary appellant has accepted that impugned supply is without consideration. We therefore conclude that the transaction is nothing but a gift.

This conclusion is further supported by the nomenclature used by the applicant to the promotional items. As averred above in case of Redemption and Rewards it is submitted by the appellant that Redemption will be conducted only in the form of gift items listed on the catalog and NO form/ type/kind of conversion into cash or cash equivalent will be permitted unless deemed fit by Sanofi.

In this case and as observed above the applicant submits that the impugned supply is a contractual obligation but without any consideration, but in exchange of services of increase sale, advertisement, etc. Thus applicant is taking contrary view. In taxation, it is not open to a person to take a simultaneously different stand.

In view of above discussion and facts of the case, we have come to the conclusion that the Applicants should not be entitled to ITC on GST paid on expenses incurred towards promotional schemes of Shubh Labh Loyalty Programme and goods given as brand reminders.

06. In view of the extensive deliberations as held hereinabove, we pass an order as follows:

Ruling:

For reasons as discussed in the body of the order, the questions are answered thus –