Original copy of GST AAR of M/s. Bharat Petroleum Corporation Limited

Original copy of GST AAR of M/s. Bharat Petroleum Corporation Limited

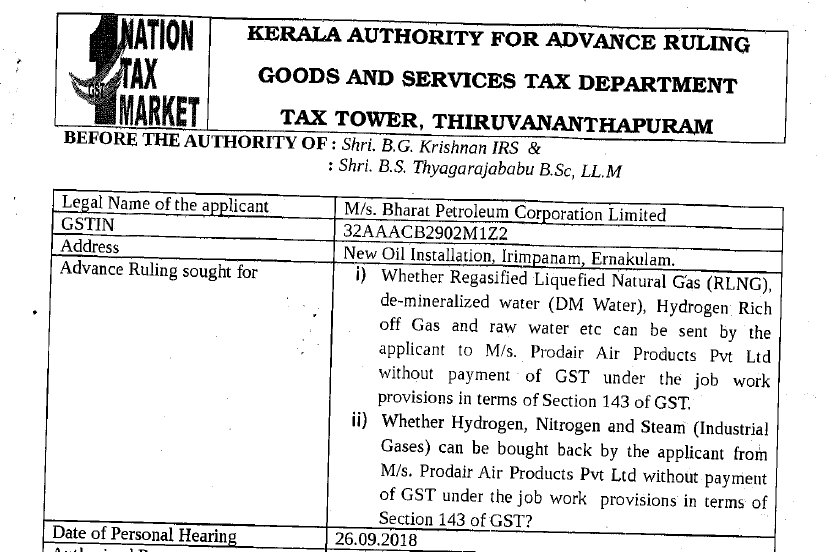

The order of GST AAR of M/s. Bharat Petroleum Corporation Limited is given on 26th September 2018. The Applicant has raised the two question in front of the ruling a authority. Following are the two questions raised:

- Whether Re-gasified Liquefied Natural Gas (RLNG), de-mineralized water (DM Water), Hydrogen Rich off Gas and raw water etc can be sent by the applicant to M/s. Prodair Air Products Pvt Ltd without payment of GST under the job work provisions in terms of Section 143 of GST.

- Whether Hydrogen, Nitrogen, and Steam (Industrial Gases) can be bought back by the applicant from M/s. Prodair Air Products Pvt Ltd without payment of GST under the job work provisions in terms of Section 143 of GST?

Order:

The applicant is a Public sector undertaking operating oil refinery and producers of several petroleum products. For carrying out the refining activity of petroleum products, the applicant requires Industrial Gases such as Hydrogen, Nitrogen and Steam. The indistrial Gases are obtained from inputs such as ‘Re-gasified Liquefied Natural Gas (RLNG), De-mineralized water (DM Water), Hydrogen Rich off Gas and raw water’. The applicant allowed M/s. Prodair Air Products Pvt Ltd to put up a facility for processing of industrial gases on Build Own Operate basis. The applicant transport the inputs for processing through pipe lines to M/s. Prodair Air Products Pvt Ltd. The applicant proposed to execute job work agreement with M/s. Prodair Air Products Pvt Ltd for processing and producing the industrial gases using the inputs provided by the applicant and send back the processed industrial gas to the applicant. The applicant sought for advance ruling on the following:

i)Whether Re-gasified Liquefied Natural Gas (RLNG), de-mineralized water (DM Water), Hydrogen Rich off Gas and raw water etc can be sent by the applicant to M/s. Prodair Air Products Pvt Ltd without payment of GST under the job work provisions in terms of Section 143 of GST.

ii) Whether Hydrogen, Nitrogen and Steam (Industrial Gases) can be bought back by the applicant from M/s. Prodair Air Products Pvt Ltd without payment of GST under the job work provisions in terms of Section 143 of GST?

The authorized representative of the applicant was heard. It is stated that applicant supply all inputs to M/s. Prodair Air Products Pvt Ltd on free of cost basis. Hence all inputs will continue to be the property of the applicant. Re-gasified Liquefied Natural Gas (RLNG) is the major input which is coming outside the ambit of the GST. Being a job work M/s. Prodair Air Products Pvt Ltd will process the inputs received from the applicant and convert them into industrial gases. They use some minor, ancillary goods to complete the processing. The applicant will have ownership over the industrial gases. As the inputs as well as outputs are transported through pipeline, there is no requirement of e-Way Bill. M/s.Prodair Air Products Pvt Ltd will collect job work or processing charge along with applicable GST @18% vide HSN 9988, manufacturing services on physical inputs owned by others. The processing charge realized by the job worker is significantly lower than the market value of industrial gases. The applicant will use the entire quantity of industrial gases for producing their output of petroleum products. As major output are not subject to GST, input tax credit availed only against the proportionate turnover of GST applicable goods.

The applicant stated that the proposed activity falls within the ambit of ‘job work’ and not manufacture. Under GST regime the scope of ‘job work’ includes manufacture as well. The HSN 9988 pertains to job work, specifically includes the words, manufacturing services on physical inputs owned by others. In the case of JSW Energy Ltd, Maharastra Appellate Authority for Advance Ruling observed that job work may include ‘manufacture’ or bringing into existence a new distinct product. Hence job work may or may not involve manufacturing. Hence it is argued that the proposed activity of movement of inputs to job worker as well as the movement of processed industrial gas from job worker to the applicant is not taxable under GST.

Download the Original copy of GST AAR of M/s. Bharat Petroleum Corporation Limited. By clicking the below Image:

The authority has examined the issues meticulously. The applicant being principal sent the goods such as Re-gasified Liquefied Natural Gas (RLNG), De-mineralized water (DM Water), Hydrogen Rich off Gas and raw water’ to M/s. Prodair Air Products for treatment or process. M/s. Prodair Air Products who is treating or processing the goods belonging to the applicant is called ‘job worker’ and the person to whom the goods belongs, i.e., applicant is called `principal’.

These inputs subject to particular process by the job worker and converted in to industrial gas and returned to the principal. It is settled position of law that job work is an activity which may or may not tantamount to manufacture. A job worker may undertake manufacturing of goods on account of others from the inputs supplied to him free of cost, and realize job work charges on return of the goods so manufactured or processed. In such a scenario the job worker alone has the liability to pay tax on the job work charges realized.

Job work is defined under Section 2(68) as any treatment or process undertaken by a person on goods belonging to another registered taxable person. The essential requirement to be fulfilled to establish a transaction as job work is the treatment or process undertaken on the goods belonging to another. Section 143 of GST Law explain the procedure to be followed in the case of job work transaction. A registered taxable person may, under intimation, send any inputs without payment of tax to a job worker for job-work and bring back inputs after completion of job work or otherwise, within one year of their being sent out, to any of the place of business without payment of tax.

The industrial gases are produced out of the major materials or inputs supplied by the applicant. The job worker uses some minor, ancillary goods to complete the process. The application of minor items by the job worker would not detract it being a job work. Therefore the processing undertaken by M/s. Prodair Air Products on the goods belong to the applicant, another registered person qualifies as job work even if it amounts to manufacture.

In the light of the discussion above, we come to the conclusion that the transport of the inputs from principal for processing through pipe lines to the premises of job worker as well as return of processed goods after job work to the principal can’t be treated as taxable supply. Based on the observations stated above, the following rulings are issued:

i) The activity of the applicant of sending Regasified Liquefied Natural Gas (RLNG), De-Mineralized Water (DM Water), Hydrogen Rich off Gas and Raw water free of cost to M/s. Prodair Air Prodcts Pvt. Ltd. For manufacture of Hydrogen, Nitrogen and Steam manufactured out of its amount to ‘job work’ as defined under Section 2(68) read with Section 143 of the CGST / KSGST Acts.

Consultant