Standard Operating Procedure (SOP) to be followed by exporters: Circular no.131/2020

Importance: (SOP) to be followed by suppliers is covered in this circular.

This is the text of circular no. 131/2017 issued by CBIC.It has prescribed the standard operating procedure for exporters in GST.

- As you are aware, several cases of monetization of credit fraudulently obtained or ineligible credit through refund of Integrated Goods & Service Tax (IGST) on exports of goods have been detected in the past few months. On verification, several such exporters were found to be non-existent in a number of cases. In all these cases it has been found that the Input Tax Credit (ITC) was taken by the exporters on the basis of fake invoices and IGST on exports was paid using such ITC.

2. To mitigate the risk, the Board has taken measures to apply stringent risk parameters-based checks driven by rigorous data analytics and Artificial Intelligence tools based on which certain exporters are taken up for further verification. Overall, in a broader time frame the percentage of such exporters selected for verification is a small fraction of the total number of exporters claiming refunds. The refund scrolls in such cases are kept in abeyance till the verification report in respect of such cases is received from the field formations. Further, the export consignments/shipments of concerned exporters are subjected to 100 % examination at the customs port.

3. While the verifications are caused to mitigate risk, it is necessary that genuine exporters do not face any hardship. In this context it is advised that exporters whose scrolls have been kept in abeyance for verification would be informed at the earliest possible either by the jurisdictional CGST or by Customs. To expedite the verification, the exporters on being informed in this regard or on their own volition should fill in information in the format attached as Annexure ‘A’ to this Circular and submit the same to their jurisdictional CGST authorities for verification by them. If required, the jurisdictional authority may seek further additional information for verification. However, the jurisdictional authorities must adhere to timelines prescribed for verification.

3.1 Verification shall be completed by jurisdiction CGST office within 14 working days of furnishing of information in proforma by the exporter. If the verification is not completed within this period, the jurisdiction officer will bring it the notice of a nodal cell to be constituted in the jurisdictional Pr. Chief Commissioner/Chief Commissioner Office.

3.2 After a period of 14 working days from the date of submission of details in the prescribed format, the exporter may also escalate the matter to the Jurisdictional Pr. ChiefCommissioner/Chief Commissioner of Central Tax by sending an email to the Chief Commissioner concerned (email IDs of jurisdictional Chief Commissioners are in Annexure B)

3.3 The Jurisdictional Pr. Chief Commissioner/Chief Commissioner of Central Tax should take appropriate action to get the verification completed within next 7 working days.

4. In case, any refund remains pending for more than one month, the exporter may register his grievance at www.cbic.gov.in/issue by giving all relevant details like GSTIN, IEC, Shipping Bill No., Port of Export & CGST formation where the details in prescribed format had been submitted etc.. All such grievances shall be examined by a Committee headed by Member GST, CBIC for resolution of the issue

5. It is requested that suitable trade notices may be issued to publicize the contents of this circular. Difficulty, if any, in implementation of this Circular may please be brought to the notice of the Board. Hindi version would follow.

Related Topic:

CBIC Issued SOP For Physical Verification

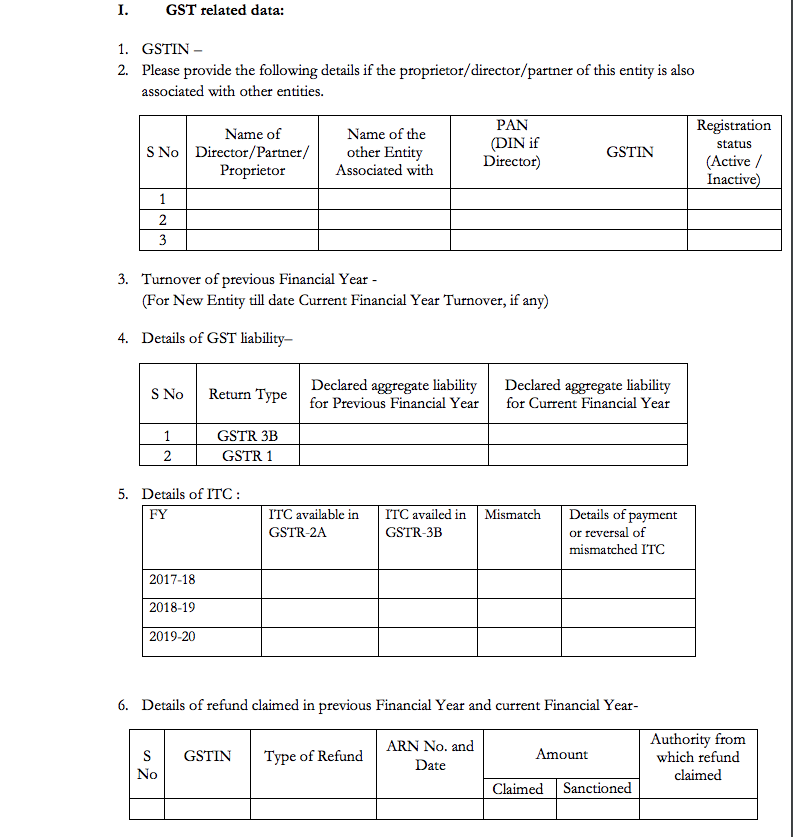

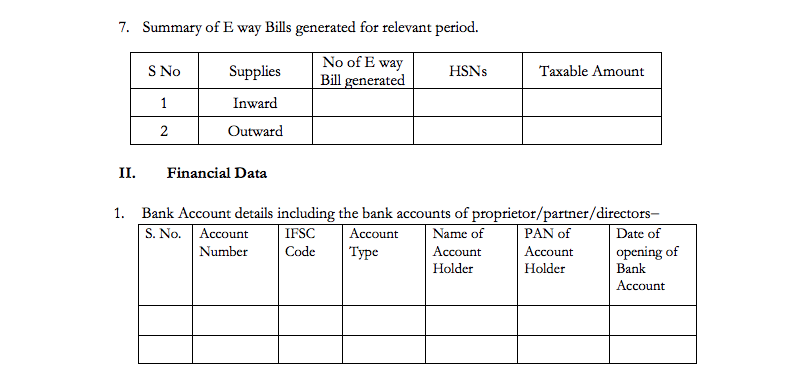

The details to be provided by the exporter for verification:

2. Bank Account statement of past 6 months in respect of the bank accounts provided above.

3. BRCs/FIRCs evidencing receipt of foreign remittances against the exports made in past 1 year.

4. Bank letter for up to date KYC of all bank accounts provided above. 5. Top 5 creditors and Debtors (with GSTIN) from account(s) where refunds are proposed to be received and from which major business transactions (payments for supplies and receipts) are carried out.

III. Additional Data

1. Copy of PAN.

2. Copy of IEC

3. Certificate of Incorporation or partnership deed

4. Rent agreement of all premises along with geo-tagged photos

5. Telephone Bill of past 3 months for all premises

6. Electricity Bill of past 3 months for all premises

7. Number of employees and the statement of PF evidencing employees

8. Copy of the following schedules of the latest Income Tax Return:

(i) Computation of depreciation on plant and machinery under the Incometax Act

(ii) Computation of depreciation on other assets under the Income-tax Act

(iii) Summary of depreciation on all the assets under the Income-tax Act