Summary of GST provisions notified from 1.01.2020

Table of Contents

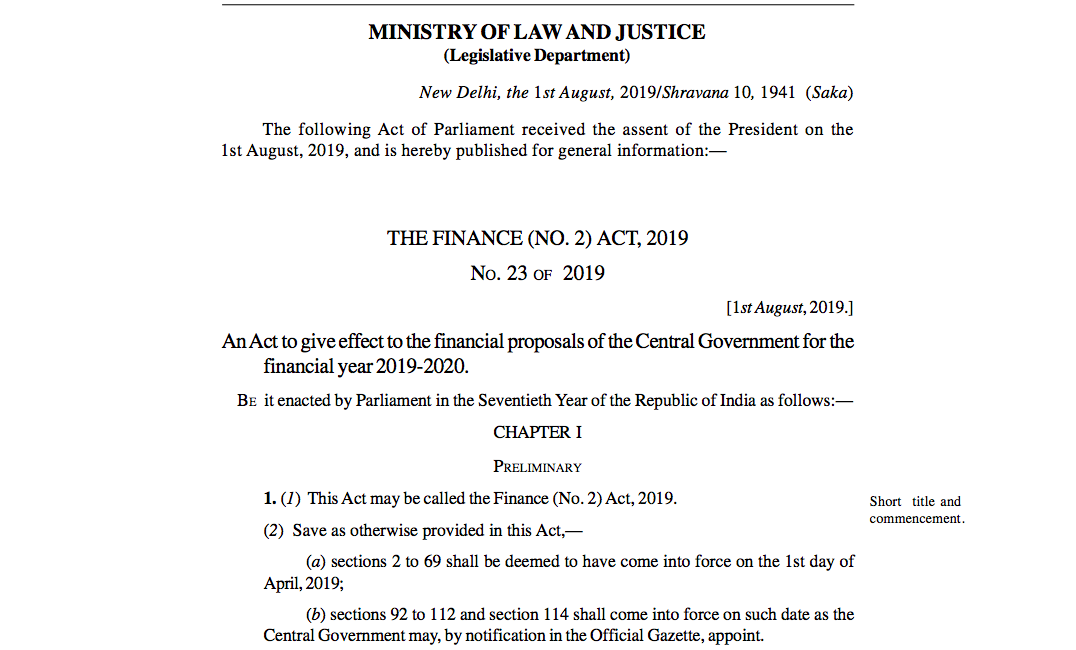

GST provisions notified from 1.01.2020: Notification No. 01/2020 – Central Tax

Notification No. 01/2020 – Central Tax has notified the date of applicability of some provisions of GST from 01012020. Let us have a look at its summary.

Summary of important provisions notified:

|

92 |

Amendment of section 2 |

|

Not yet notified |

|

93 |

Amendment of section 10 |

– NRTP and CTP cant opt for composition. – Interest will not be a part of taxable turnover and aggregate turnover to determine eligibility. – |

Notified from 1st Jan 2020 via notification no. 01/2020 – Central Tax

|

|

94 |

Amendment of section 22. |

– 20 lac limit may extended to 40 lac only in case of supply of Goods. – But interest is allowed meaning thereby that if I am receiving interest only apart from goods I will still be eligible for this 40 lac limit.

|

Notified from 1st Jan 2020 via notification no. 01/2020 – Central Tax

|

|

95 |

Amendment of section 25. |

|

Notified from 1st Jan 2020 via notification no. 01/2020 – Central Tax

|

|

96 |

Insertion of new section 31A. Facility of digital payment to recipient |

Providing modes for digital payment. |

Notified from 1st Jan 2020 via notification no. 01/2020 – Central Tax

|

|

97 |

Amendment of section 39 |

|

Not yet notified |

|

98 |

Amendment of section 44. |

Annual return date extension power. |

Notified from 1st Jan 2020 via notification no. 01/2020 – Central Tax

|

|

99 |

Amendment of section 49. |

– PMT 09 form for shifting tax from one head to another head. |

Notified from 1st Jan 2020 via notification no. 01/2020 – Central Tax

|

|

100 |

Amendment of section 50. |

Interest levy on net not on gross |

Not yet notified |

|

101 |

Amendment of section 52. |

Power to extend time limit of Form 9B to be filed by ECO |

Notified from 1st Jan 2020 via notification no. 01/2020 – Central Tax

|

|

102 |

Insertion of new section 53A. Transfer of certain amounts |

|

Notified from 1st Jan 2020 via notification no. 01/2020 – Central Tax

|

|

103 |

Amendment of section 54 |

|

Not yet notified |

|

104 |

Amendment of section 95. |

|

Not yet notified |

|

105 |

Insertion of new sections 101A, 101B and 101C. Constitution of National Appellate Authority for Advance Ruling |

|

Not yet notified |

|

106 |

Amendment of section 102. |

|

Not yet notified |

|

107 |

Amendment of section 103. |

|

Not yet notified |

|

108 |

Amendment of section 104. |

|

Not yet notified |

|

109 |

Amendment of section 105. |

|

Not yet notified |

|

110 |

Amendment of section 106 |

|

Not yet notified |

|

111 |

Amendment of section 168 |

Commissioner defined |

Notified from 1st Jan 2020 via notification no. 01/2020 – Central Tax

|

|

112 |

Amendment of section 171 |

Anti profiteering penalty |

Notified from 1st Jan 2020 via notification no. 01/2020 – Central Tax

|

Download copy of Finance Act(2) 2019:

CA