38th GST Council Meeting dated 18-12- 2019

Extension of Date of Filing GSTR 9 and 9C

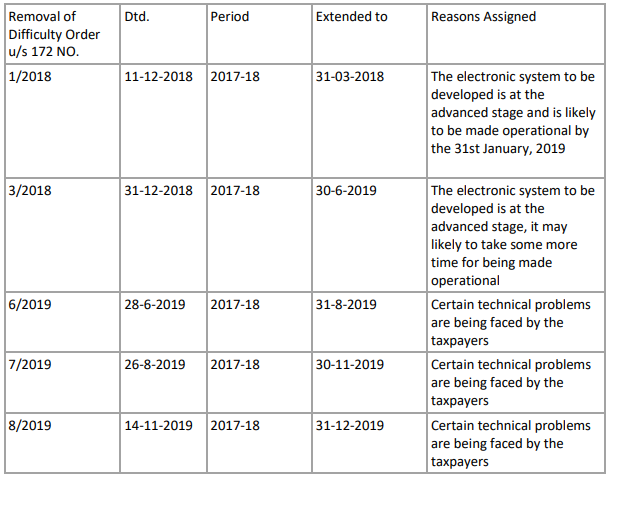

Date for GSTR 9 and 9C for 2017-18 has been extended to 31-1-2020. Earlier Extensions for GSTR 9 and 9C are as under:

GSTR-1

Late Fee Waiver on GSTR-1

1. Notification 4/2018-CT dated 23-01-2018, reduced late fee for delayed filing of GSTR-1 from Rs. 200/- per day to Rs. 50/- per day. For NIL returns it was reduced to Rs. 20/- per day

2. Notification 75/2018-CT dated 31-12-2018 waived late fee for pending GTSR-1 returns from July 2017 to September 2018 provided the GSTR-1 is filed between 22-12-2018 to 31-03-2019.

3. However gstn portal has not been charging any late fee for late filing of GSTR-1.

4. GST Council meeting dated 18-12-2019 has recommended waiver of late fee to be given to all taxpayers in respect of all pending FORM GSTR-1from July 2017 to November 2019, if the same are filed by 10.01.2020 .

E way Bill Blocking extended to GSTR-1

GST Council meeting dated 18-12-2019 has recommended that E-way Bill for taxpayers who have not filed their FORM GSTR-1 for two tax periods shall be blocked

ITC on not uploaded invoices restricted to 10% instead of Earlier limit of 20%

Input tax credit to the recipient in respect of invoices or debit notes that are not reflected in his FORM GSTR-2A shall be restricted to 10 per cent of the eligible credit available in respect of invoices or debit notes reflected in his FORM GSTR-2A.

Blocking of ITC for fraudulent invoices

GST Council meeting dated 18-12-2019 has recommended that suitable action to be taken for blocking of fraudulently availed input tax credit in certain situations.

SOP for non filers of GSTR 3B

A Standard Operating Procedure for tax officers would be issued in respect of action to be taken in cases of non-filing of FORM GSTR 3B returns.

Rates on Woven/Non Woven Bags

In 37th Meeting of GST Council held at Goa pn 20-09-2019, a uniform rate of 12% on Polypropylene/Polyethylene Woven and Non- Woven Bags and sacks, whether or not laminated, of a kind used for packing of goods (from present rates of 5%/12%/18%) was recommended. Notification 14/2019 dated 30-09-2019 w.e.f. 01-10-2019 changed the rate to 12% by inserting Entry 80AA in Schedule II @ 6% as under in schedule II-6%

(i)after S.NO. 80A and entries relating there to,the following S.NO. and entries shall be interested namely:-

![]()

However Council meeting dated 18-12-2019 has recommended that GST rate on Woven and NonWoven Bags and sacks of polyethylene or polypropylene strips or the like , whether or not laminated, of a kind used for packing of goods ( HS code 3923/6305) be raised to a uniform rate of 18%(from 12%) on all such bags falling under HS 3923/6305 including Flexible Intermediate Bulk Containers (FIBC). This change shall become effective from 1st January, 2020.

Tax Rate on Lotteries

1. Lottery run by state government (i.e. lottery not allowed to be sold in any state other than the organising State) is taxable @ 12% as per Entry 242 of Schedule II of Notification 1/2017-CTR dtd 28-6-17

2. Lottery authorized by State Governments (i.e. lottery which is authorized to be sold in State(s) other than the organising state also) is taxable @ 28% as per Entry 228 of Schedule IV of Notification 1/2017-CTR dtd 28-6-17

3. Tax on lottery when supplied by State Government, Union Territory or any local authority is subject to RCM and tax is payable by Lottery distributor or selling agent as per Notification 4/2017-CTR dtd 28-06-2017

4. Valuation of Lottery is done as per Rule 31A as under:

5. Supply of lottery by any person other than State Government, Union Territory or Local authority subject to the condition that the supply of such lottery has suffered appropriate central tax, State tax, Union territory tax or integrated tax, as the case may be, when supplied by State Government, Union Territory or local authority, as the case may be, to the lottery distributor or selling agent appointed by the State Government, Union Territory or local authority, as the case may be is exempt as per Entry 149 of Notification 2/2017-CTR dated 28- 6-176. Now GST Council meeting dated 18-12-2019 has recommended uniform tax rate of 28% for lottery run by state government as well as lottery authorized by state government. Change shall be effective from 01-01-2020.

Exemption for Long Term Lease of industrial/financial infrastructure

Plots to Entities having government ownership

GST Council meeting on 18-12-201 has recommended to exempt upfront amount payable for long term lease of industrial/ financial infrastructure plots by an entity having 20% or more ownership of Central or State Government. Presently, the exemption is available to an entity having 50% or more ownership of Central or State Government. This change shall become effective from 1st January, 2020.

Grievance Redressal Committes at Zonal/State Level

Grievance Redressal Committees (GRC) will be constituted at Zonal/State level with both CGST and SGST officers and including representatives of trade and industry and other GST stakeholders (GST practitioners and GSTN etc.). These committees will address grievances of specific/ general nature of taxpayers at the Zonal/ State level.