Time of Supply with Examples

Need and Meaning of Time of Supply:

For the purpose of paying tax liability, point of taxation is required. Time of supply is nothing but, it is point of taxation.When the supplies have been made at that time, the point of taxation has arisen. To find out that supplies have been made or not, we need to determine the time of supply. Once the time of supply occurred, a supplier is required to discharge his GST liability.

There are some general provisions and some specific provisions for determining the time of supply. The time of supply is different for goods & services. If specific provisions are applied to determine the time of supply then the general provision is irrelevant.

Time of Supply with examples

To determine the time of supply of Goods & Services, Four categories are provided as below:

- Time of Supply of Goods & Services under forward Charge.

- Time of Supply of Goods & Services under Reverse Charge.

- Time of Supply in case of Supply of Vouchers.

- Residuary Clause.

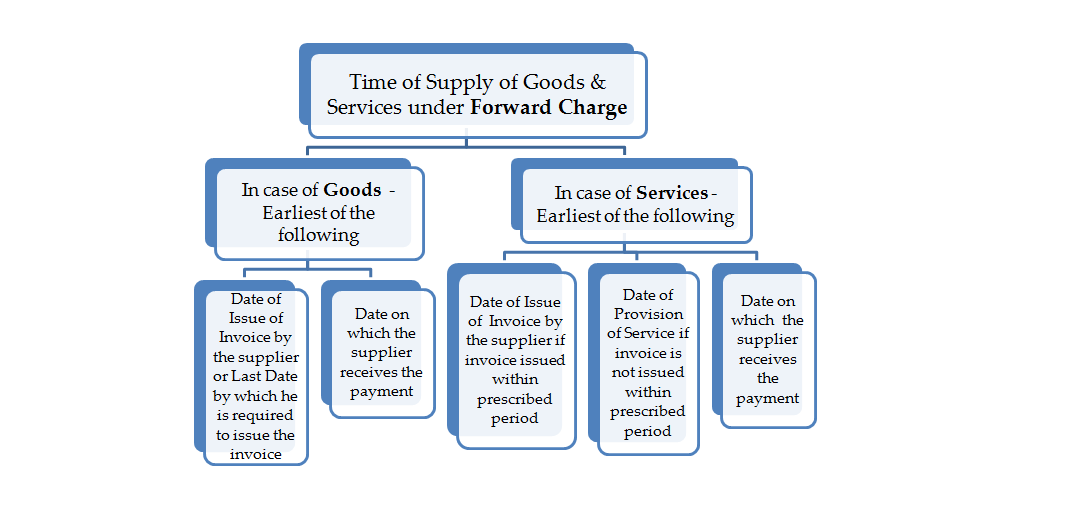

1. Time of Supply of Goods & Services under Forward Charge:

Some Important Points:

- Time of Issue of Invoice for Goods:

i. If the movement of goods involved in supply than before or at the time of removal of goods.

ii. If no movement of goods involved in supply than before or at the time of delivery of goods or making available to the recipient.

iii. If the continuous supply of goods Ex. Supply of Oil etc. than earliest of the following:

- The time when each statement is issued.

- Time when each payment is received.

iv. If goods sent for approval than earliest of the following:

- Time when it becomes known that supply is taken place.

- Six month from the date of removal.

- Time of Issue of Invoice for Services:

i. Before or after the provision of service but within a period prescribed:

- 30 days in all cases except for banking and financial institutions from the date of supply of services.

- 45 days in case of banking and financial institutions from the date of supply of services

ii. In case of continuous supply of services:

- Due date of payment can be identified from the contract : The invoice will be issued before or after the payment is to be made by the recipient but within 30 or 45 days of due date of payment.

- Due date of payment is cannot be identified from the contract : The invoice shall be issued before or after each time when the supplier of service receives the payment but within 30 or 45 days of receipt of payment

- Payment is linked to the completion of an event: The invoice shall be issued before or after the time of completion of that event but within 30 or 45 days of completion of the event.

- Supply of services ceases under a contract before the completion of the supply: The invoice shall be issued at the time when the supply ceases and such an invoice shall be issued to the extent of the service provided before stopping.

- The supply shall be deemed to have been made to the extent it is covered by the invoice or, as the case may be, the payment.

- Date of Receipt of the payment by supplier: Payment is entered into the books of the account or credited in his bank account whichever is earlier.

- Optional Time of supply: If amount up to Rs. 1,000 in excess of the invoice amount is received then the supplier may take the time of supply is the date of invoice issued for such excess or advance received.

- If invoice is not issued and date of payment or date of completion of provision of service are also not ascertainable, than the time of supply shall be the date on which the recipient shows the receipt of services in his books of accounts.

Examples:

Q.1

Mr. A, a manufacturer, sold goods to Mr. B, wholesaler, and issued invoice for the sale on 01st August 2017. Now, determine the time of supply of goods for the following cases:

a. Mr. A removes the goods for delivery to Mr. B on 16th August 2017.

b. Mr. B collects the goods from premises of Mr. A on 10th August 2017.

c. Mr. B made full payment on 26th July 2017.

d. Mr. B credited the payment in bank account of Mr. A on 28th July 2017 for 3/4th of goods, Mr. A recorded the same as receipts in his books on 3rd August 2017. The goods were dispatched on 5th August 2017 from the warehouse.

A.1

a. 1st August 2017 is the time of supply of goods

i.e. Earlier of the following:

Date of Invoice – 1st August 2017 or

Date on which invoice is required to be issued – 16th August 2017.

b. 1st August 2017 is the time of supply of goods

i.e. Earlier of the following:

Date of Invoice – 1st August 2017 or

Date on which goods is delivered – 10th August 2017.

c. 26th July 2017 is the time of supply of goods

i.e. Earlier of the following:

– Date of Invoice – 1st August 2017 or

– Date of Payment – 26th July 2017.

d. The time of supply of goods for 3/4th of the goods will be 28th July 2017 as the payment has been made prior to the date of invoice and the time of supply of goods will be 1st August 2017 for remaining 1/4th goods. The late recording of receipt in the books by Mr. A will have no impact.

Q.2

Mr. A entered into a contract with Mr. B to supply of oil throughout the year. Mr. A issues monthly statement for the oil supplied to Mr. B. Now, determine the time of supply of goods in following cases:

a. Mr. B made payment for the month of July on 31st July 2017 and Mr. A issued statement for the month of July on 8th August 2017.

b. Mr. A issued statement for the month of August on 5th September 2017, the payment of which not received till 30th September 2017.

A.2

a. 31st July 2017 will be the time of supply.

Earliest of the following:

Date of Invoice: 8th August 2017

Last date on which invoice has to be issued: Date of payment or statement whichever is earlier i.e. 31st July 2017.

b. 5th September 2017 will be the time of supply.

Earliest of the following:

Date of Invoice: 5th September 2017.

Last date on which invoice has to be issued: Date of payment or statement whichever is earlier i.e. 5th September 2017.

Q.3

ABC Consultancy services issued invoice for services rendered to Mr. P on 5th August 2017. Determine the time of supply in following cases:

a. The provisions of services were completed on 1st July 2017.

b. The provisions of services were completed on 15th July 2017.

c. Mr. P made the payment on 3rd August 2017, where provisions of services were remaining to be completed.

d. Mr. P made the payment on 15th August 2017, where provisions of services were remaining to be completed.

A.3

a. 1st July 2017 will be the time of supply of services as invoice is not issued within the time frame of 30 days.

b. 5th August 2017 will be the time of supply of services as invoice is issued within the time frame.

c. 3rd August 2017 will be the time of supply of services as payment received before invoice date.

d. 5th August 2017 will be the time of supply of services as invoice is issued before the completion of provisions of services.

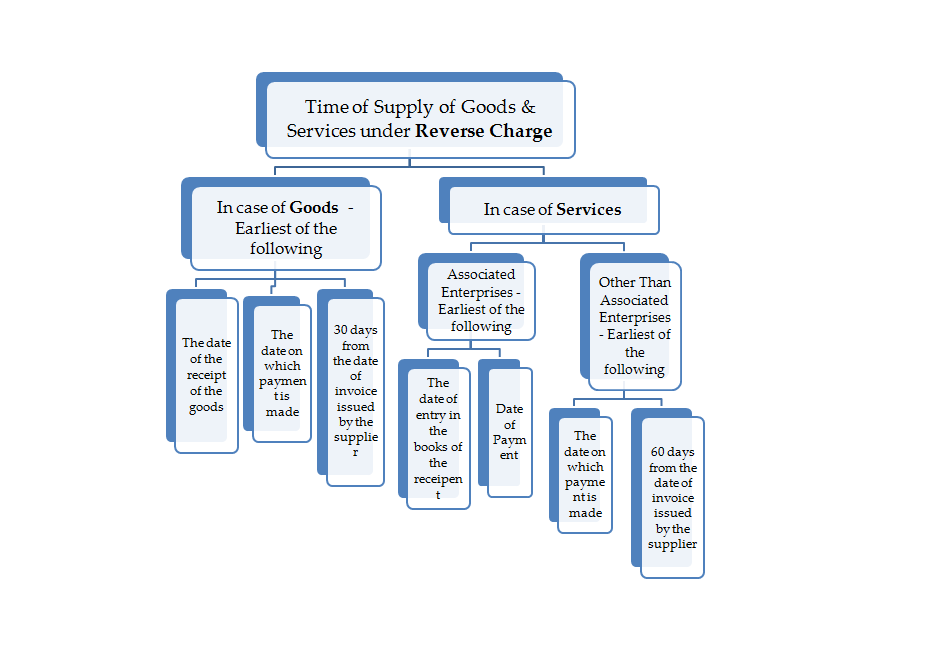

2. Time of Supply of Goods & Services under Reverse Charge:

- If time of supply cannot be determined with the help of above provisions then the time of supply shall be the date on which entry in the books of the recipient of goods & services is made.

Example:

Q.4

Mr. A, a registered dealer received goods from Mr. B, an unregistered dealer. Mr. B issues invoice on 1st July 2017. Now, determine time of supply of goods in following cases:

a. Mr. A received goods on 15th July 2017, payment of which is not made yet.

b. Mr. A received goods on 3rd August 2017 & made payment for the same on 4th August 2017.

c. Mr. A made payment on 8th July and received goods on the same date.

d. Mr. A received goods on 10thJuly 2017 & made payment for the same on 9thJuly 2017.

A.4

a. 15th July 2017 will be the time of supply of goods.

Earliest of the following:

Receipt of Goods = 15th July 2017

Date of Payment = NA

30 days from the date of invoice = 30th July 2017

b.30thJuly 2017 will be the time of supply of goods.

Earliest of the following:

Receipt of Goods = 3rd August 2017

Date of Payment = 4th August 2017

30 days from the date of invoice = 30th July 2017

c. 8th July 2017 will be the time of supply of goods.

Earliest of the following:

Receipt of Goods = 8th July 2017

Date of Payment = 8th July 2017

30 days from the date of invoice = 30th July 2017

d. 9th July 2017 will be the time of supply of goods.

Earliest of the following:

Receipt of Goods = 10th July 2017

Date of Payment = 9th July 2017

30 days from the date of invoice = 30th July 2017

Q.5

ABC Ltd., a registered firm received services from PQR Ltd.,an unregistered firm. PQR Ltd. issued invoice to ABC Ltd. on 1st July 2017. ABC Ltd. & PQR Ltd is not associated enterprises. Determine the time of supply of services:

a. ABC Ltd. made the payments to PQR Ltd. on 15th August 2017.

b. ABC Ltd. made the payments to PQR Ltd. on 11th September 2017.

A.5

a. 15thAugust 2017 will be the time of supply of services as payment made earlier than the date immediately following 60 days from date of issue of invoice.

b. 30stAugust 2017 will be the time of supply of services as payment made after the date immediately following 60 days from date of issue of invoice.

Q.6

XYZ Ltd. & MNT Ltd. is associated enterprises. XYZ Ltd., a registered firm received the services of MNT Ltd., a unregistered firm. Determine the time of supply in following cases:

a. XYZ Ltd. recorded the liability in the books on 15th July 2017 and payment will be made in the next month.

b. XYZ Ltd. made advance payment to MNT Ltd. on 10th July and recorded liability in the books on 15th July 2017.

A.6

a. 15th July 2017 will be the time of supply of services as the date of entry in the books is prior to the date of payment.

b. 10th July 2017 will be the time of supply of services as the payment is made earlier to the date of entry in the books.

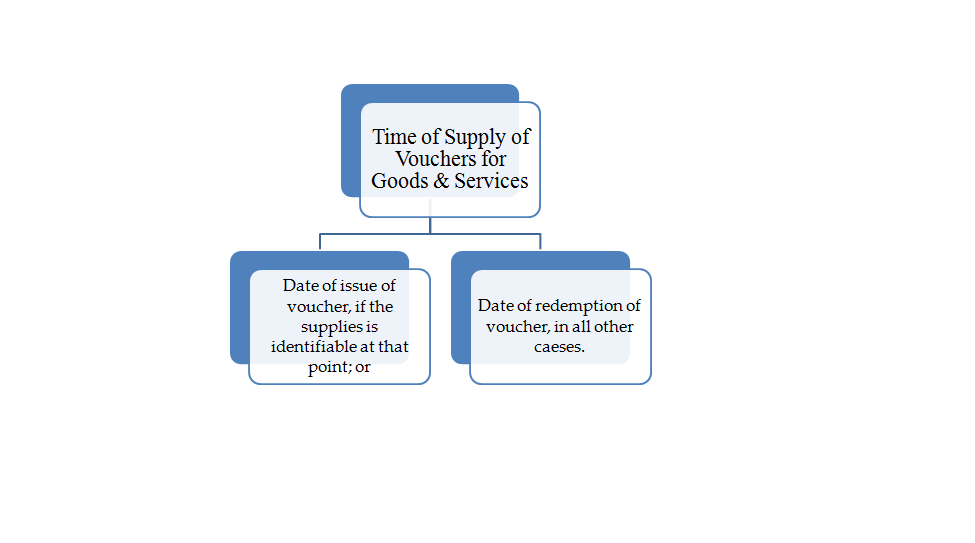

3. Time of Supply of Vouchers for Goods & Services:

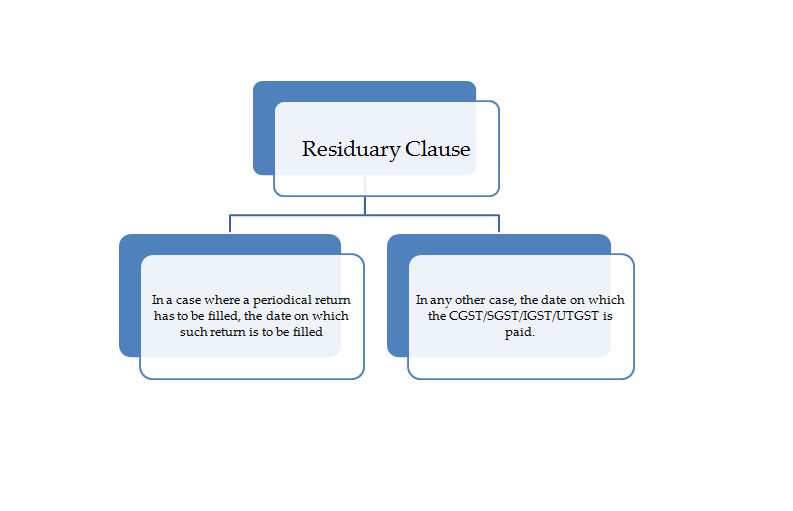

4. Residuary Clause

Time of Supply in case of Change in Rate of Tax:

|

Case |

Events before change in effective rate of tax |

Events after change in effective rate of tax |

Time of supply if goods & services are supplied before change in effective rate of tax |

Time of supply if goods & services are supplied after change in effective rate of tax |

|

1. |

Invoice Issued/Payment Received |

No activity. |

Whichever is earlier |

NA |

|

2. |

Invoice Issued/Payment Received |

Supply of Goods & Services |

NA |

Whichever is earlier |

|

3. |

Invoice issued |

Payment Received |

Date of Invoice |

Date of receipt of Payment |

|

4. |

Payment Received |

Invoice Issued |

Date of receipt of Payment |

Date of Invoice |

- The date of receipt of payment shall be the date of credit in the bank account if such credit in the bank account is after four working days from the date of change in the rate of tax.

- Date of Receipt of the payment by supplier: Payment is entered into the books of the account or credited in his bank account whichever is earlier.

Example:

Q.7

Mr. A is supplied goods to Mr. B on 28th December 2017. The GST rate on goods is changed from 12% to 5% w.e.f. 1st January 2018. Mr. A issued invoice on 28th December 2017 and payment is credited in his bank account on 30th December 2017. What is the time of supply in this case?

A.7

Following Event have been done before change in effective rate of tax:

- Goods Supplied

- Invoice Issued

- Payment Received

Time of supply will be earliest of the following:

- 28th December 2017

- 30th December 2017

Time of Supply will be 28th December 2017.

Q.8

Mr. A is supplied goods to Mr. B on 28th December 2017. The GST rate on goods is changed from 12% to 5% w.e.f. 1st January 2018. Mr. A issued invoice on 2ndJanuary 2018 and payment is credited in his bank account on 29thDecember 2017. What is the time of supply in this case?

A.8

Following Event have been done before change in effective rate of tax:

- Goods Supplied

- Payment Received

Time of supply will be Date of receipt of payment i.e. 29th December 2017.

Q.9

Mr. A is supplied goods to Mr. B on 28th December 2017. The GST rate on goods is changed from 12% to 5% w.e.f. 1st January 2018. Mr. A issued invoice on 28th December 2017 and payment is credited in his bank account on 4thJanuary 2018. What is the time of supply in this case?

A.9

Following Event have been done before change in effective rate of tax:

- Goods Supplied

- Invoice Issued

Time of supply will be Date of Invoice i.e. 28th December 2017.

Q.10

Mr. A is supplied goods to Mr. B on 2ndJanuary 2018. The GST rate on goods is changed from 12% to 5% w.e.f. 1st January 2018. Mr. A issued invoice on 28th December 2017 and payment is credited in his bank account on 30th December 2017. What is the time of supply in this case?

A.10

Following Event have been done before change in effective rate of tax:

- Invoice Issued

- Payment Received

Time of supply will be earliest of the following:

- 28th December 2017

- 30th December 2017

Time of Supply will be 28th December 2017.

Q.11

Mr. A is supplied goods to Mr. B on 2ndJanuary 2018. The GST rate on goods is changed from 12% to 5% w.e.f. 1st January 2018. Mr. A issued invoice on 29thDecember 2017 and payment is credited in his bank account on 4thJanuary 2017. What is the time of supply in this case?

A.11

Following Event have been done before change in effective rate of tax:

- Invoice issued

Time of supply will be Date of receipt of payment i.e. 4th January 2018.

Q.12

Mr. A is supplied goods to Mr. B on 2ndJanuary 2018. The GST rate on goods is changed from 12% to 5% w.e.f. 1st January 2018. Mr. A issued invoice on 2ndJanuary 2018 and payment is credited in his bank account on 29thDecember 2017. What is the time of supply in this case?

A.12

Following Event have been done before change in effective rate of tax:

- Payment Received

Time of supply will be Date of invoice i.e. 2nd January 2018.

Q.13

Let’s say there was increase in tax rate from 18% to 20% w.e.f. 1.6.2017. What is the tax rate applicable when services provided and invoice issued before change in rate in April 2017, but payment received after change in rate in June 2017?

A.13

The old rate of 18% shall be applicable as services are provided prior to 1.6.2017.

Time of Supply with Examples

Test