Ppt on Finalization of Books and Accounts

Ppt on Finalization of Books and Accounts (GST Audit)

The Finalization of Books and Accounts for FY 2017-18 is close and it will be done as soon as soon. The following is the ppt on Finalization of Books and Accounts FY 2017-18:

Challenges in Finalization of Books of Accounts FY 2017-18:

- Year divided between old and new regime

- No Pending balance of Old liabilities

- Transitional entries to be reviewed properly – Special focus on C/F balance, stock as on 30 June, Job Work etc.

- Anti-profiteering – Benefit to be pass on

- Cannot Contradict own Statutory Report, Tax Audit Report, and GST Audit Report

- GST Refund – Recoverability to be check

- Capital Expenditure charged in P&L

- Eligible ITC Reco with GSTR 2A

- Ineligible ITC to be reversed with Interest

- RCM Sec 9(4) applicability

- Credit Note – GST Impact

- Supply against LUT

- Show Cause Notice

- Reversal of Common credit in case of Taxable and Exempt supply

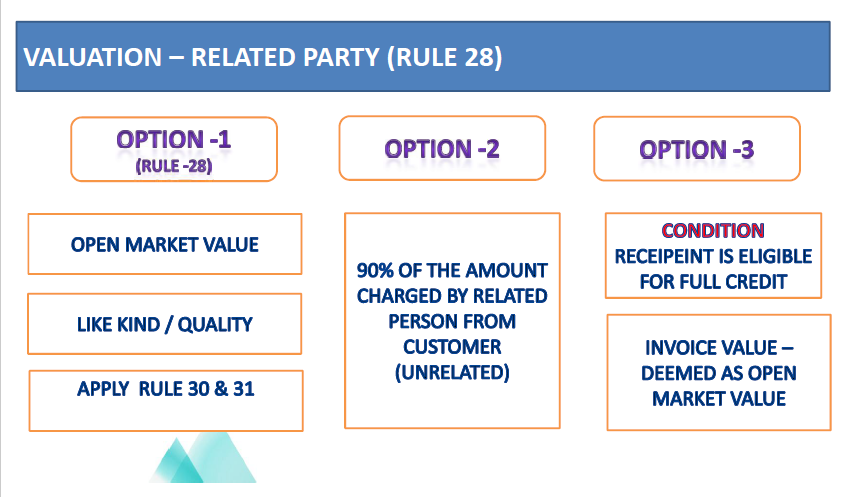

Overview of GST Audit

- Audit Means – Section 2(13)

- Audit of A/c by Chartered/Cost Accountant – Section 35(5)

- The audit by Tax Authorities – Section 65

- Special Audit – Section 66

- Annual Return with Audited A/c with Reco statements – Rule 80(3)

- Annual Return Composition – Form 9A

- Annual statement- e-commerce operator – Form 9B

- Annual Return with Audited Accounts & Reco – Form 9C

- Statement of Particulars – Form 9D

Download the full Ppt on Finalization of Books & Accounts GST Audit, by clicking the below Image:

The audit by Tax Authorities

Power to Conduct Audit U/S 65(1)

- The Commissioner or any other officer authorized by him may undertake Audit

- Through general or Specific order

- Financial year or Multiples thereof [rule 101]

General Order

- on the basis of pre‐defined parameters for audit

Special Order

- a particular person may be required to be audited in the context of certain transactions/class of transactions

- At Place of Business of the registered person or in their office

- Registered person shall be informed by notice not less than 15 working days (ADT01)

- Complete within 3 Months from Date of G. S. Bhullar & Co. Commencement – Extended 6 Months