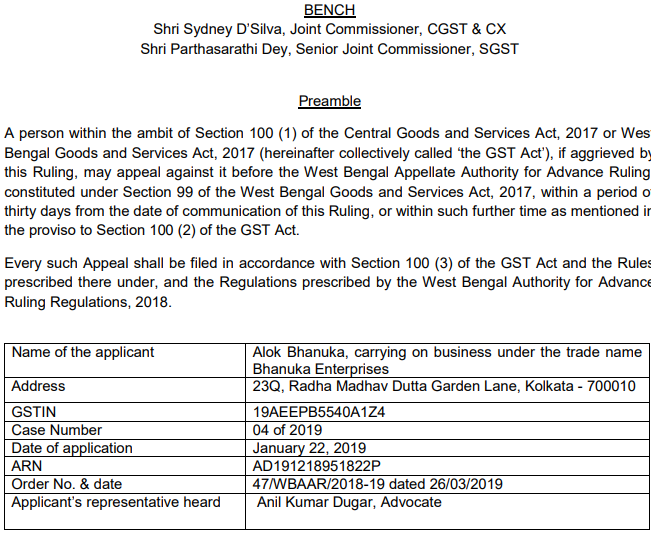

Original copy of GST AAR OF Alok Bhanuka

In the order of GST AAR OF Alok Bhanuka, the applicant has raised the query regarding the mentioned service being job work or not. Following is the copy of GST AAR OF Alok Bhanuka:

Order:

1. Admissibility of the Application

1.1 The Applicant is stated to be engaged in repairing and servicing of transformers owned by WBSEDCL. He seeks a ruling on whether the said repair/servicing is job work as defined under section 2(68) of the GST Act, and whether it is composite or mixed supply. If it is composite supply, the Applicant wants to know what should be the principal supply and the rate of tax thereon. He also wants to know whether the repaired transformers can be delivered to WBSEDCL against challans without raising tax invoices.

1.2 This Authority is not empowered to pronounce ruling on the documentation required for transportation of goods. However, the other questions that the Applicant has raised involve classification of the supply for the purpose of ascertaining entries specified under notifications on applicable tax rate. These questions are, therefore, admissible for advance ruling under section 97 (a) & (b) of the GST Act.

1.3 The Applicant states that the questions raised in the Application have neither been decided by nor are pending before any authority under any provision of the GST Act. The officer concerned from the Revenue has raised no objection to the admission of the Application.

1.4 The Application is, therefore, admitted.

2. Submissions of the Applicant

2.1 The Applicant, according to the Application and the written submission made at the time of Hearing, transports the defective and damaged transformers from WBSEDCL, dismantles them, and removes the burnt coil and other damaged parts and accessories that require replacement/repair. The repaired transformers are tested and delivered to WBSEDCL. Being the principal insurer, WBSEDCL reimburses the expense on account of transport, fire and burglary insurance.

2.2 The Applicant argues that repair/servicing of transformers is job-work as defined under section 2(68) of the GST Act, and should to be treated as supply of service in terms of para 3 of Schedule II to the GST Act.

2.3 The Applicant refers to Notification No. 5050-F(Y) dated 16/08/2017 of the Government of West Bengal. It has clarified that works involving supply of taxable goods along with labour to any movable property (e.g. servicing of motor vehicles with motor parts, AMC for computers or AC machines or generator, repair of furniture etc.) are composite supplies, as the supply of goods and labour are naturally bundled and made in conjunction with one another. The principal supply, according to the said notification, is determined by the pre-dominant nature of the contract. For example, in the case of servicing of motor vehicles or AMCs the principal supply is ‘service’. On the other hand, in a contract for supply-cum-installation of an AC machine the principal supply will be the AC machine.

2.4 Following the above notification, the Applicant argues that repair/servicing of transformers is a composite supply, where the pre-dominant nature of the contract remains that of ‘service’, classifiable as under SAC 9987, and taxable under Sl No. 25(ii) of Notification No. 11/2017 – CT (Rate) dated 28/06/2017 (corresponding State Notification No. 1135 – FT dated 28/06/2017), as amended from time to time, and hereinafter collectively called the Rate Notification. 3. Observations & Findings of the Authority

Download the full Original copy of GST AAR OF Alok Bhanuka, by clicking the below image:

3.1. Job work has been defined under section 2(68) of the GST Act as any treatment or process undertaken by a person on goods belonging to another registered person. Rule 2(h) of the Cenvat Credit Rules, 2004 defines job work as processing or working upon raw materials or semi-finished goods supplied to the job worker, so as to complete a part or whole of the process resulting in the manufacture or finishing of an article or any operation which is essential for the afore-mentioned process.

3.2 In course of repairing the defective transformers the Applicant replaces the worn out or burnt materials. The process, therefore, involves transfer of property in goods. The Applicant’s contribution is, therefore, not limited to labour and skill done with the help of his own tools, gadgets or machinery. In his own admission, supply of goods constitutes major portion of the value of the supply. The process is not, therefore, job work, as defined under section 2(68) of the GST Act.

3.3 Para 6(a) of Schedule II of the GST Act refers to works contract as a composite supply. Although limited to immovable properties only, the activity of repairing is included in the definition of works contract under section 2(119) of the GST Act. In fact, repairing was treated as works contract under both Service Tax and Value Added Tax, and the treatment under the GST Act differs only so far asthe movable properties are excluded from the domain of works contract. Composite nature of the activity of repairing remains unaltered when applied to movable properties. It is a supply of goods and services in conjunction and as naturally bundled in the ordinary course of business. Unless the contract specifies that the goods and the services supplied are to be separately charged, the nature of the supply remains a composite supply. The principal supply, however, depends upon the dominant element of the composite supply.

3.4 In this connection, attention may be drawn to the order dated 19/12/2018 of Maharashtra AAR in Cummins India Ltd. While examining the nature of the supply in annual maintenance contracts (hereinafter AMC), the AAR correctly points out that the predominant intention in such AMC is to provide maintenance service for the proper upkeep of the machines belonging to the clients. Hence supply of maintenance service is the dominant intention of the contracts and can be considered as the ‘principal supply’.

3.5 Repairing and servicing of defective transformers signify working on something which is already in existence. It involves supply of goods, but not as chattels. The goods, namely the spare parts that have replaced the defective ones, are embedded or fixed to the transformer already in existence so that the defects get removed. The contract is not for the supply of the spare parts, but for the treatment or process for maintenance and removal of the defects from the transformers that belong to WBSEDCL. The predominant element of the supply, therefore, is not transfer of title to the goods, but service in terms of para 3 of Schedule II to the GST Act, and supply of spare parts is ancillary to such supply. The service so supplied is classifiable under SAC 998719, being repair of transformers, and taxable under Sl No. 25(ii) of the Rate Notification, as amended from time to time.

Ruling:

In view of the foregoing, we rule as under.

Repairing and servicing of transformers owned by another person is not job work as defined under section 2(68) of the GST Act. It is composite supply unless the contract specifies that the goods and services are to be separately charged. The principal supply is the service of repair of transformers classifiable under SAC 998719 and taxable under Sl No. 25(ii) of Notification No. 11/2017 – CT (Rate) dated 28/06/2017 (corresponding State Notification No. 1135 FT dated 28/06/2017), as amended from time to time.

This Ruling is valid subject to the provisions under Section 103(2) until and unless declared void under Section 104(1) of the GST Act.

Consultant