GST -Goods and Services Tax , learn basics

GST implementation on July 1st, 2017:

GST was implemented in India in 2017, 1st July. It is the biggest tax reform in India. GST subsumed a number of indirect taxes. Earlier our constitution allowed levy of tax either by center or state. 101st Constitution amendment Act was introduced to allow both center and state to levy tax. It is levied on every supply of goods and/or services. It was introduced to simplify indirect taxes in India. After the implementation of GST there are only two main indirect taxes.

- Customs (on import and export transactions)

- GST

- State VAT and excise on some products not subsumed into GST. (only on limited items)

There are many amendments in the CGST Act also. You can download the updated documents from here.

Taxes Subsumed by GST

GST replaces these taxes currently levied and collected by the Centre:

(a) Central Excise Duty,

(b) Duties of Excise (Medicinal and Toilet Preparations),

(c) Additional Duties of Excise (Goods of Special Importance),

(d) Additional Duties of Excise (Textiles and Textile Products),

(e) Additional Duties of Customs (commonly known as CVD),

(f) Special Additional Duty of Customs(SAD),

(g) Service Tax,

(h) Cesses and surcharges, in so far as they relate to the supply of goods and services.

Related Topic:

GST LEVY ON TOUR OPERATOR

State taxes that get subsumed within the GST are:

(a) State VAT,

(b) Central Sales Tax,

(c) Purchase Tax,

(d) Luxury Tax,

(e) Entry Tax (All forms),

(f) Entertainment Tax and Amusement Tax (except those levied by the local bodies),

(g) Tax on advertisements,

(h) Tax on lotteries, betting and gambling,

(i) State cesses and surcharges in so far as they relate to the supply of goods and services

Related Topic:

Monthly End to End Indirect Taxes Updates

How tax is levied in GST?

GST levy is based on the nature of the transaction. There are two types of supplies.

- Intra-state

- Inter-state

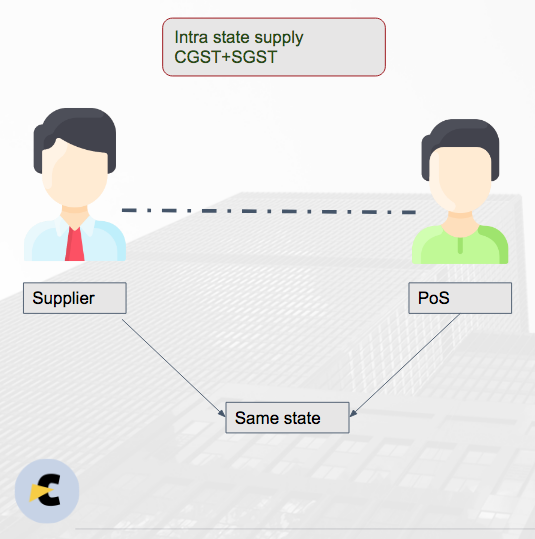

When the location of the supplier and place of supply both are in the same state. It is called intra-state supply. In this case CGST and SGST are levied. Generally the rate of CGST and SGST is half od IGST. They combine equate IGST. CGST is a portion of the center’s share in the tax of a particular transaction. SGST is the state’s share in tax for a transaction. You can see in the image how it works.

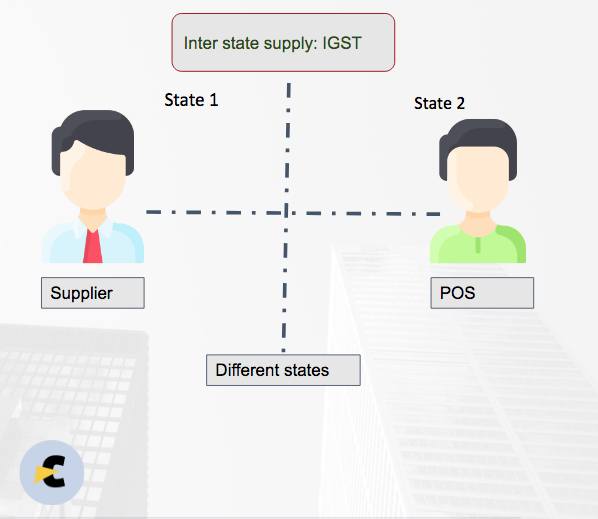

In the case of Inter- state supply only one tax is levied. But IGST covers some other scenarios also. In the following cases IGST is levied:

- When the location of the supplier is in different state fro the state of the place of supply

- Exports from India are always treated as inter state supply

- Import into the territory of India are also treated as inter state supply

- Supply to SEZ unit or developer is also treated as inter-state supply

In all of the above cases, IGST is levied.

How to decide the amount of tax payable under GST?

GST is charged on the transaction value. Now what is transaction value? section 15 of the CGST Act provides that the price actually paid for a particular transaction is transaction value. Thus in your case the tax will be charged on the actual amount recovered for the purpose of supply.

Illustration 1

M/s Chow min Sold a packet of noodles to Mr. Chilli sauce at Rs. 32. The price written on the packet of noodles is Rs. 30. Here the taxable value is Rs. 30 and tax are chargeable at Rs. 30 at applicable rates.

How tax is paid in GST?

It is also a value-added tax. It means that a person is liable to pay tax only on his value addition. This is ensured by way of an input tax credit. When a person purchases a supply and pays tax. He can adjust that tax at the time of sales.

Illustration 2

Mr. Tik purchases a mobile phone for Rs. 30000 and paid tax of Rs.5100. Now if he sells this mobile it is Rs. 50,000 plus tax of Rs. 9000. He is required to deposit only Rs. 3900 to the government. He can adjust the tax of Rs. 5100 paid at the time of purchase.

As you know there are three types of taxes. You can adjust any tax on purchase with any tax on sales. But you cant adjust CGST with SGST or SGST with CGST.

Illustration 3

Mr. Tik purchases have the following input tax credit for the month of March.

CGST: Rs. 500

SGST: Rs. 300

Now he makes sales of Rs. 10000 with IGST of Rs. 1800. He can adjust both CGST and SGST against it.

He needs to pay Rs. 1800-500-300= Rs. 1000

Now let us assume he sale the Goods in the same state for Rs. 2000 and tax of Rs. 360 CGST and Rs 360 SGST. Now let us see the adjustment.

CGST: Rs. 360 can be adjusted with the CGST of Rs. 500. Thus in CGST he doesn’t need to pay anything.

SGST: Rs. 300 can be adjusted with SGST on purchase but Rs. 60 cant be adjusted with the balance of CGST. He is liable to pay Rs. 60 in SGST.

Generally, we make payment of tax for all transactions during the month by 20th of next month. We need to file a return for that. When we file a return of a month, a challan is created after filing all basic details. Then we can pay that challan via bank and can file the return. You also need to file a return of sales or outward supply. The return for the payment of tax is GSTR3b and sales is GSTR 1. Apart from this an annual return is also filed. It is called GSTR 9 or annual return.

When to take registration in GST?

Now you may think, whether all of us are required to pay GST. We do but not directly to the government. Levy section of the CGST Act prescribes the people who are liable to collect and pay tax on behalf of the government. Accordingly following are liable to register:

- When the turnover crosses Rs. 20 Lac. In case of a supply of Goods only the turnover limit is Rs 40 lac.

- Where a person is liable to pay tax under reverse charge

- A casual taxable person or non-resident taxable person.

- Inter-state supply of Goods (even for a single transaction)

- Electronic commerce operator

- A person covered under reverse charge

- An ISD

Filing of returns in GST:

There are only two main returns in GST. GSTR 3b and GSTR 1.

There is a late fee for the late filing of these returns. In case of late filing of GSTR 3b, interest is also leviable. We need to pay tax at the time of filing of GSTR3b. The interest rate is 18%. It is levied on the net tax payable after the adjustment of ITC. Domestic supply is declared in table 3.1.b of GSTR 3b. Zero-rated supplies like Export and supply to SEZ developer or unit are to be declared in table 3.1.b of GSTR 3b.

Annual return, GSTR 9: Other than this an annual return is also required to be filed by a registered person. But for the first two years requirement of annual return is waived off for the taxpayers having turnover up to 2 crores. But for the future years this may be required to be filed by every taxpayer.

GSTR 9C, GST Audit: Every taxpayer having turnover more than Rs. 2 crores is required to file GSTR 9C. This is a reconciliation statement and audit report of GST.

Composition scheme of GST for the small taxpayer:

There is a scheme for small taxpayers. It is called the composition scheme. In this scheme fewer compliances are required There is no eligibility of ITC. The taxpayer can pay tax at a reduced rate of 1% in the case of a supply of Goods. In the case of the services tax rate is 6%. This tax is not collected from the buyer There is no tax invoice for this supply. You can opt for it at the GSTN portal at the time of registration or later on. The threshold limit for this levy in 1.5 Cr.

Return: A composition dealer can file their return in form CMP 08. They need to file it quarterly. A return in form GSTR 4A is also required to be filed annually. They are also required to file annual returns. But for the initial two years are exempted from filing an annual return.

Exports in GST:

Exporters are provided specific benefits in GST. They can export the goods without payment of tax. A LUT is required for export without payment of tax. In case of export with payment of tax they can claim the refund of tax paid. In the case of LUT export also they can claim the refund of an input tax credit.

A form in RFD 1A is available on the GST portal. This form can be used to file a refund in GST. Now the refund process is completely online. there is no need to visit the department. Once the form is filed, the officer can issue a Deficiency memo. The taxpayer can file the details required in the deficiency memo. An acknowledgment is issued. In 7 days after this acknowledgment refund is issued.

Important changes in GST since inception:

Every day starts with something new in GST. We have compiled various changes in the law since its inception.

Registration in GST:

Important changes in registration provisions of GST since inception.

- Voluntary registration can also be canceled by the taxpayer.

- E-commerce vendor is not required to take registration up to a turnover of 20lac.

- The Interstate supply of services is not mandatory registration criteria anymore.

Input tax credit

Rule 36(4)

Non-availability of the input tax credit when it is not reflecting in GSTR 2A of the taxpayer. Only 10% of ITC reflecting in GSTR 2A can be taken in excess of what is reflecting.

Illustration: 4

There was an ITC of rs. 32000 in the GSTR 2A of X ltd. But they have invoices for purchases having a tax of Rs. 44000. They can take ITC of Rs. 32000+10%= Rs. 35,200 rupees. The rest of the ITC is available once it is also reflected in GSTR 2A.

Rule 88A:

Manner of the utilization of ITC. This provision is inserted from 29th March 2019 and amended on 28th June 2019. ITC of CGST or SGST can be utilized only when the ITC of IGST is exhausted.

Illustration: 5

Syska Ltd has the following input tax credit in their ledger.

- IGST Rs. 30000

- CGST Rs. 40,000

- SGST Rs. 40,000

They have the following output tax liability.

CGST: Rs. 50,000

SGST: Rs. 50,000

Now we need to adjust the IGST first.

Rs. 50,000- IGST ITC of Rs. 30,000=Rs. 20,000. This Rs. 20,000 can be adjusted by CGST ITC.

Now for SGST, we can utilize the ITC of SGST= Rs. 50,000-Rs. 40000(SGST ITC). They need to pay Rs. 10000 via cash ledger.

This provision saw a lot of opposition. Then it was clarified that proportionate adjustment of ITC is also possible.

Thus in the same case, ideal utilization is:

CGST liability Rs. 50,000 Adjust Rs.10000 out of IGST and balance Rs. 40,000 from CGST input tax credit balance.

Now SGST Rs. 20,000 can be adjusted from IGST and balance from SGST. No tax payment in cash is required,

But still, IGST shall be fully exhausted before the ITC utilization of CGST and SGST.

Refund

Refund provisions are changed multiple times. The current position in major issues is:

- Apply for LUT and Export without payment of tax. See here how to apply for LUT?

- A refund of the input tax credit is available when you export without payment of tax under LUT. But refund of tax on capital goods is not allowed. capital goods are the goods capitalized in books of accounts.

- Refund when ITC is accumulated because the tax rate on inputs is less than the tax rate on output. This is called an Inverted rated structure. But in this case refund of ITC on capital goods and services is not available.

Recent amendments

- In the case of export of goods the value of export shall be up to 1.5 times of value in the domestic market.

- A refund application can be filed online.

- All the documents can also be filed online on the GSTN portal.

- Other than an export refund will be given in same ledger from where the tax was paid.

- If ITC is not reflecting in 2A, no refund of ITC is eligible.

- HSN code of items is mandatory in refund applications.

Interest

It was a huge dilemma since the inception of GST. The department was of the view that interest shall be charged on the gross liability. GST experts were of the view that it should be on net tax. What is gross tax and what is Net tax?

Illustration 6

M/s Delta skipped their GSTR 3b for the month of March 2019 for 30 days. Their outward tax liability was Rs. 10 lac and they had Rs. 8 lac in ITC ledger. Now, this Rs. 10 lac is their gross liability and Rs. 2 lac is a net liability. Thus the liability after adjustment of the input tax credit is called net tax liability.

After long litigation in case of Reflex industries it was held that interest should be on net liability. Then the GST council also recommended that it should be on net liability only.

Transitional provisions

Career opportunities in GST

Consultant