Tax and penalty on Cash Deposit due to Demonetization

The Union Finance Minister Arun Jaitley yesterday introduced the Taxation Laws (Second Amendment) Bill, 2016 with a view to tax unaccounted black money deposited in bank accounts pursuant to demonetisation. The government has introduced Chapter IXA: ‘Taxation and Investment Regime for Pradhan Mantri Garib Kalyan Yojana, 2016′ (PMGKY) consisting of Section 199A to 199R .The salient terms of the proposal to tax the unaccounted cash are as follows:

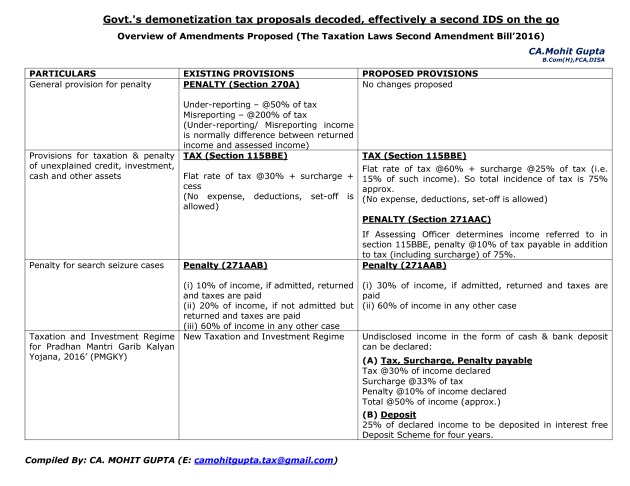

(i) 30 per cent tax on undisclosed income plus 10 per cent penalty as also a 33 per cent surcharge ( Total Tax incidence of around 49.9% of the amount declared );

(ii) 25 per cent of undisclosed income post demonetisation has to be deposited in the Pradhan Mantri Garib Kalyan Deposit Scheme for a lock in period of 4 years (non-interest bearing) ;

The money from the Pradhan Mantri Garib Kalyan Deposit scheme would be used for projects in irrigation, housing, toilets, infrastructure, primary education, primary health and livelihood so that there is justice and equality, states the Statement of Objects and Reasons of the Bill

(iii) In other cases, wherein this opportunity is not availed, undisclosed wealth deposited post demonetisation which is detected by the income-tax authorities will attract 75 per cent tax and 10 per cent penalty.

The copy of the Taxation Laws (Second Amendment ) Bill, 2016 along with a tax rate/penalty analysis sheet is enclosed herewith. Tax and penalty on cash deposit will be calculated accordingly.

Download PDF for the chart

|

PARTICULARS |

EXISTING PROVISIONS |

PROPOSED PROVISIONS |

|

|

General provision for penalty |

PENALTY (Section 270A) |

No changes proposed |

|

|

|

Under-reporting – @50% of tax |

|

|

|

|

Misreporting – @200% of tax |

|

|

|

|

(Under-reporting/ Misreporting income |

|

|

|

|

is normally difference between returned |

|

|

|

|

income and assessed income) |

|

|

|

Provisions for taxation & penalty |

TAX (Section 115BBE) |

TAX (Section 115BBE) |

|

|

of unexplained credit, investment, |

|

Flat rate of tax @60% + surcharge @25% of tax (i.e. |

|

|

cash and other assets |

Flat rate of tax @30% + surcharge + |

|

|

|

15% of such income). So total incidence of tax is 75% |

|

||

|

|

cess |

approx. |

|

|

|

(No expense, deductions, set-off is |

|

|

|

|

(No expense, deductions, set-off is allowed) |

|

|

|

|

allowed) |

|

|

|

|

|

PENALTY (Section 271AAC) |

|

|

|

|

If Assessing Officer determines income referred to in |

|

|

|

|

section 115BBE, penalty @10% of tax payable in addition |

|

|

|

|

to tax (including surcharge) of 75%. |

|

|

Penalty for search seizure cases |

Penalty (271AAB) |

Penalty (271AAB) |

|

|

|

(i) 10% of income, if admitted, returned |

(i) 30% of income, if admitted, returned and taxes are |

|

|

|

and taxes are paid |

paid |

|

|

|

(ii) 20% of income, if not admitted but |

(ii) 60% of income in any other case |

|

|

|

returned and taxes are paid |

|

|

|

|

(iii) 60% of income in any other case |

|

|

|

Taxation and Investment Regime |

New Taxation and Investment Regime |

Undisclosed income in the form of cash & bank deposit |

|

|

for Pradhan Mantri Garib Kalyan |

|

can be declared: |

|

|

Yojana, 2016’ (PMGKY) |

|

(A) Tax, Surcharge, Penalty payable |

|

|

|

|

|

|

|

|

|

Tax @30% of income declared |

|

|

|

|

Surcharge @33% of tax |

|

|

|

|

Penalty @10% of income declared |

|

|

|

|

Total @50% of income (approx.) |

|

|

|

|

(B) Deposit |

|

|

|

|

25% of declared income to be deposited in interest free |

|

|

|

|

Deposit Scheme for four years. |