Impact Of GST On Real Estate Sector

Table of Contents

GST on real estate: A detailed analysis

The Real Estate industry is one of the largest sectors in the country and is a major contributor in the growth of Indian economy. This industry is one of the rapidly growing sectors in India since the factors such as accelerated urbanization, migration, increasing population, emerging nuclear families have increased the requirement of residential houses. Due to such increasing demand of residential houses, demand of commercial places such as offices, malls, factories have also increased. Moreover, after the introduction of “Housing for all” and other similar schemes by the Govt., the real estate sector is expected to grow multifold.

Further, as far as indirect taxes are concerned, prior to 01.07.2017, the builders/contractors were required to comply with the provisions of Finance Act, 1994 (i.e. Service Tax) and relevant VAT Acts while providing the construction services. However, w.e.f. 01.07.2017, such taxes have been substituted with one single tax namely GST wherein CGST + SGST or IGST is required to be paid by the builders/contractors on the services provided by them.

Real Estate Sector was one of the most complex areas of the tax levied by the Centre and States was Works Contract and Sale of Property. Prior to 01.07.2017, such transactions could have been broken into 3 parts:- – Value of goods and materials – Value of services, and – Value of land

1. POSITION OF LAW PRIOR TO GST

(A) WORKS CONTRACT- The Tribunal in the case of Real Value Promoters (P) Ltd. Vs. CCE observed as under:- “The Union Government, for the first time w.e.f. 1.6.2007, decided to tax the service component of composite contract such as “Works Contract” w.e.f. 1.6.2007. Pure Construction Services (not composite contract involving supply of goods) such as Commercial Construction Service or Commercial & Industrial Construction Service, prior to 1.6.2007, liable to service tax. Pure construction services which are not in the nature of Works Contract would be liable to Service Tax prior to 1.6.2007 and even thereafter but CCS/CICS, which involve both supply of goods and services, shall not be liable to Service Tax.”

By virtue of judgment of the Hon’ble Supreme Court in the CCE vs. Larsen & Toubro Ltd. 2015 (39) STR 913 SC, the contract involving

(i) supply of goods and (ii) supply of services i.e. “Works Contract” were not liable to Service Tax prior to 01.06.2007. However, w.e.f. 1.7.2007 onwards, Works Contract was liable to Service Tax only when composite contract is sought to be classified in SCN as Works Contract. However, in case, Works Contract is sought to be classified as Construction of Complex Service (CCS)/Commercial or Industrial Construction Service (CICS), even then no Service Tax could be levied as the proper classification is “Works Contract” and not CCS/CICS.

2. POSITION UNDER GST LAW

Under the GST Law, we find the following the two entries:

As per clause (b) of paragraph 5 of Schedule II of CGST Act, the following shall be treated as Supply of Service: (b) Construction of a complex, building, civil structure or a part thereof, including a complex or building intended for a sale to a buyer, wholly or partly, except where the entire consideration has been received after issuance of completion certificate, where required, by the competent authority or after its first occupation, whichever is earlier.

Para 5 of Schedule III of CGST Act states that activity of sale of land and subject to para 5 (b) of Schedule II, sale of buildings is neither supply of goods nor supply of services. As per Entry No. 49 of List II of 7 th Schedule to Constitution, ‘taxes on lands and building’ is a State subject. Though constitution grants concurrent powers to Union and State to levy GST, these are subject to recommendation of GST Council. Thus, GST on transactions relating to land and buildings can be imposed only to the extent recommended by GST Council.

As per S. 2(119) of the CGST Act, “Works Contract” is defined as a contract for: Building, construction, Fabrication, completion, erection, installation, fitting out, improvement, modification, alteration or commissioning of any immovable property wherein transfer of property in goods (whether as goods or in some other) form is involved in the execution of such contract. There must be transfer of property in goods.

In Skipper Ltd., In Re (2018) 100taxmann.com (AAR-WB), it was held that contract for manufacture, supply, erection and commissioning of transmission towers is works contract. It cannot be split into contract of supply of material, transportation, insurance and supply of services.

The Hon’ble division bench of Orissa High Court in the case of Safari Retreats Pvt. Ltd. & Ors. Vs. CCE, MANU/OR/0332/2019 held that the provisions of S. 17 (5) (d) is to be read down and the narrow restriction as imposed, is not required to be accepted, in as much as keeping in mind the language used in MANU/SC/0051/1999: (1999) 2 SCC 361 (supra), the very purpose of the credit is to give benefit to the assessee. In that view of the matter, if the assessee is required to pay GST on the rental income arising out of the investment on which he has paid GST, it is required to have the input credit on the GST, which is required to pay under S. 17 (5) (d) of the CGST Act.

Related Topic:

Construction Services Under GST – A Detailed Information

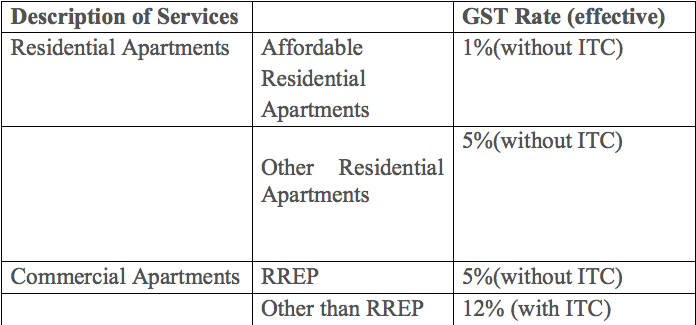

3. POSITION FROM 01.04.2019 OLD GST RATES VS. NEW GST RATES

Till, 31.3.2019, GST for Construction Services of residential and commercial apartment, after abatement of land was 12% with ITC.

However, GST rate on the specified housing scheme was 8% with ITC. From 1.4.2019, Real Estate Industry has undergone complete change and has been divided into two parts: (1) Residential Real Estate Project (RREP) with maximum space of 15% for commercial apartments; and (2) Other Real Estate Project (REP).

Related Topic:

PPT on GST on Real Estate

With effect from 1.4.2019, the effective rate of GST on construction of affordable residential apartments by promoters is 1% without ITC on total consideration and rate of GST on construction of residential apartments other than affordable residential apartments is 5% without ITC on total consideration. The above rates are effective from 01.04.2019 and are applicable to construction of residential apartments in a project which commences on or after 01.04.2019 as well as in on-going projects. However, in case of on-going projects, the promoter has an option to pay GST at the old rates, i.e. at the effective rate of 8% on affordable residential apartments and effective rate of 12% on other than affordable residential apartments and consequently, to avail permissible credit of inputs taxes; in such cases the promoter is also expected to pass the benefit of the credit availed by him to the buyers.

4. FREE SUPPLIES:

Supply of Free of Cost (FOC) material by the contractee to the contractor shall not be included in the value of supply provided the recipient of supply (i.e. contractor) is not liable to pay for such FOC material.

For example: ABC Limited awards contract for construction of 100 electrical towers. Steel is major raw material for these towers. Under the contract, ABC Limited will supply required quantity of steel to the contractor. Contractor will arrange for all other materials and deliver complete tower at designated place and time. Value of steel will not be included in taxable value for GST since the supplier was not liable to pay for the steel as per the contract.

However, where ownership is transferred from the supplier to the recipient, it shall be considered as supply. Similarly, where contract has been entered for a value including FOC material, and the value of the FOC material is deducted afterwards, it would also be included in the value of supply. Therefore, if a contract is entered for the net consideration without including free supply of material by the contractee to the contractor for execution of works contract, no tax is payable by the contractor on such value of goods.

To illustrate: ABC entered into a contract with XYZ contractor for INR 100 Lakhs. Cement and steel, as required, are to be provided by ABC at an agreed price, which will be deducted from the contract value. In this case, suppose ABC supplies steel worth INR 30 lakhs; and after adjusting this value, ABC pays INR 70 lakhs through bank to XYZ. In such case, supply of cement and steel shall be considered as supply by ABC to XYZ; and thereafter, XYZ will be liable to pay GST on entire value of contract of INR 100 lakhs.

The Hon’ble Supreme Court in the case of M/s Bhayana Builders (P) Ltd. & Ors. Vs. CST 2018 (10) GSTL 118 (SC) 3 has dealt with the issue of whether value of goods/materials supplied or provided free by a service recipient and used for providing taxable service of construction of commercial or industrial complex must be included in computation of gross amount for valuation of taxable service U/s 67 of the Act? It was held by the Court that the goods & materials supplied/provided/used by service provider for incorporation in construction, which belong to provider and for which service recipient is charged towards value of such supply/provision/use & corresponding value whereof was received by service provider, to accrue to his benefit, whether independently specified as attributable to specific material/goods incorporated or otherwise, would alone constitute gross amount charged. The value of goods & materials supplied free of cost by a service recipient to provider of taxable construction service, being neither monetary or non-monetary consideration paid or flowing from service recipient, accruing to benefit of service provider, would be outside taxable value or gross amount charged within the meaning of S.67 of the Act.

5. POINTS TO BE CONSIDERED WHILE DRAFTING AN AGREEMENT:

1) The essence of the contract should be of entering into two separate contracts; (i) Supply of goods: and (ii) rendition of Service. Further, breach of one contract should not adversely affect another contract, i.e., there should not be any cross-fall breach clause.

2) The consideration in relation to supply portion and service portion must be clearly stated in the tender as well as contract, and moreover, there should not be any conflicting clause in the tender/ contract;

3) There should be a complete sale in respect of supply portion and all the ingredients specified under the Sales of Goods Act must be satisfied;

4) Consideration of goods in relation to transfer of documents of titles should be separately invoiced;

5) The said goods must be received in stock of the contractee, and thereafter, these should be provided to the contractor as free supply. Care must be taken in maintaining and preserving documentation.

An Affordable residential apartment is a residential apartment in a project which commences on or after 01.04.2019, or in an ongoing project in respect of which the promoter has opted for new rate of 1% (effective from 01.04.2019) having carpet area upto 60 square meter in metropolitan cities and 90 square meter in cities or towns other than metropolitan cities and the gross amount charged for which, by the builder is not more than Rs.45 Lakhs. In an ongoing project in respect of which the promoter has opted for new rates, the term also includes apartments being constructed under the specified housing schemes of Central or State Governments. (Metropolitan cities are Bangalore, Chennai, Delhi NCR [limited to Delhi, Noida, Greater Noida, Ghaziabad, Gurgaon, and Faridabad], Hyderabad, Kolkata and Mumbai {whole of MMR} with their geographical limits prescribed by Govt.).

“Real Estate Project (REP)” shall have the same meaning as assigned to it in S.2 (zn) of the RERA Act, 2016 and means the development of a building or a building consisting of apartments, or converting an existing building or a part thereof into apartments, or the development of land into plots or apartments, for the purpose of selling all or some of the said apartments or plots or buildings and includes the common areas, the development works, all improvements and structures thereon and all easement, rights and appurtenances belonging thereto.

Residential Real Estate Project (RREP) shall mean a REP in which the carpet area of the commercial apartment is not more than 15% of the total carpet area of all the apartments in the REP.

Floor Space Index (FSI) shall mean the ratio of a building’s total floor area (gross floor area) to the size of the piece of land upon which it is built.

CONCLUSION:

In Pre GST regime, the Developer had to deposit several indirect taxes collected from customer. But post GST, it had reduced the cascading effect. GST has significant impact on real estate as it has increased the cost of construction for the builders after its implementation. The CBIC has notified rules and procedures for builders intended to take benefits of reduced rates (1 to 5% on sale of under construction flats commencing on or after 01.04.2019).