Original copy of GST AAR of Ratan Projects & Engineering Co Private Limited

In the order of GST AAR OF Ratan Projects & Engineering Co Private Limited, the applicant6 has raised the query regarding the treatment of the goods sent to job worker. The original COPY OF GST AAR OF Ratan Projects & Engineering Co Private Limited is as below:

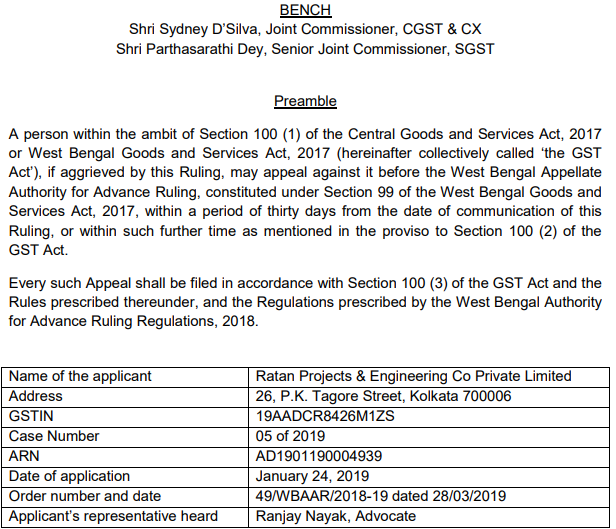

Order:

1. Admissibility of the Application

1.1 The Applicant is stated to be a manufacturer of cable tray, angel ladder tray etc, which are mainly used for electrical works. The Applicant sends steel structures for galvanising to a job worker along with furnace oil, zinc, nickel that are to be consumed in the galvanising process. He seeks a ruling whether dispatch of those consumable materials is to be treated as supply from the principal to the job worker if they are not returned within the time allowed under section 143(1)(a) of the GST Act. An advance ruling is admissible on this issue under section 97(2)(g) of the GST Act.

1.2 The Applicant declares that the issue raised in the application is not pending nor decided in any proceedings under any provisions of the GST Act. The officer concerned from the revenue has raised no objection to the admissibility of the Application. The Application is, therefore, admitted.

2. Submissions of the Applicant

2.1 In his written submission the Applicant elaborates on the proportion in which zinc, nickel and furnace oil are consumed in the galvanizing process, and reiterates what has been stated in the Application.

Download the full original copy of GST AAR of Ratan Projects & Engineering Co Private Limited, by clicking the below image:

3. Observations & Findings of the Authority

3.1 Job work is defined under section 2(68) of the GST Act as any treatment or process undertaken by a person on goods belonging to another registered person, and a job-worker shall be construed accordingly. The Applicant sends steel structures of different names and shapes to a job-worker for the process of galvanising, which effectively means the application of a protective zinc coating to prevent rusting. It is, therefore, an intermediate stage in the Applicant’s manufacturing activity, and the ‘inputs’ mentioned in section 143(1)(a) include the intermediate goods arising from the process of galvanising (refer to Explanation to section 143). Therefore, the return of the galvanised goods to the Applicant satisfies the condition of receiving back the ‘inputs’ in accordance with section 143(1)(a) of the GST Act.

3.2 The ‘inputs’ returned, however, do not include in their original physical forms the goods like furnace oil, zinc etc that have been sent to the job-worker. The Applicant submits that these goods have been consumed in the galvanising process. The most commonly used galvanising techniques require immersion of the steel structure in a bath of molten zinc. The zinc is contained in a galvanising kettle, which is heated to the point when the zinc turns liquid. Furnace oil is consumed in the heating process. Use of nickel, according to the Applicant, is rare and depends on the buyer’s requirement.

3.3 It is, therefore, evident that galvanising involves consumption of zinc, furnace oil, and sometimes nickel – either as raw materials or consumables. Whether the entire quantity of such goods sent to the job-worker has actually been exhausted in the process is a question of evidence and records. The issue this Authority decides is, however, limited to whether the goods that are not returned physically as ‘inputs’, being consumed in the process of galvanising, should be treated as supply in terms of section 143(3) of the GST Act.

3.4 In Rahee Infratech Ltd [2016 (339) ELT 293 Tri – Kolkata)] CESTAT, Kolkata Bench decided a similar question in the context of Cenvat credit. The appeal was filed against the order of the Revenue, refusing to allow Cenvat credit on the zinc sent to the job-worker for galvanising on the ground that the said zinc had not been returned along with the galvanised steel structures. The ld court, being satisfied that the zinc had been exhausted in the galvanising process, rejected the Revenue’s argument and allowed the appeal. Clearly, the idea that what has been used up must be physically returned does not find favour with the judiciary.

3.5 The goods that are used up in the galvanising process cannot be separated from the galvanised goods. The meaning attributed to ‘inputs’ in the Explanation to section OFtakes care of the difference between the inputs sent to the job-worker and the goods returned after some intermediate treatment/process like galvanisation that may exhaust some of the inputs sent out. It expands the meaning of ‘inputs’ to the intermediate goods that include, as embedded, attached or consumed, the inputs that are exhausted in the process of manufacturing the intermediate goods. So, the zinc, furnace oil or nickel exhausted in the process of galvanising need not be physically returned. If the galvanised structures are returned that will be sufficient compliance of section 143(1)(a) of the GST Act.

Ruling:

In view of the foregoing, we rule as under.

Return of the galvanised goods to the Applicant satisfies the condition of receiving back the inputs in accordance with section 143(1)(a) of the GST Act. As the goods like furnace oil, zinc etc – consumed in the process of galvanising – are inseparable from the galvanised goods, they should not be treated as supply in terms of section 143(3) of the GST Act, provided they have been entirely used up in the process of galvanising.

This Ruling is valid subject to the provisions under Section 103 until and unless declared void under Section 104(1) of the GST Act

Consultant