Recent Changes in Real Estate

Table of Contents

Opportune Time for Builders & Officials to Enrich Gracefully

Changes in Real Estate: Confusions Galore – Common Man @ Mercy

In the recent times there are Headline News and Flashes in many Electronic Media about GST rate slash to just 1% & 5% from as high as 8% & 12%. It might have enthused the common man before election time.

The GST Council in its 33rd, 34th Council Meetings recommended the reduction in GST rates on residential house properties and accordingly notifications were flashed. There may be some good intention behind it in line with Government’s vision to provide every citizen to afford to own a house by 2022. The measure also may be seen to boost demand so as to ease out the huge pileup of un-sold inventory in the real-estate sector which is somehow denting the growth of economy. However, the Intentions are not seeming to be translated truly to ground level.

Let’s here analyze some of the major issues:

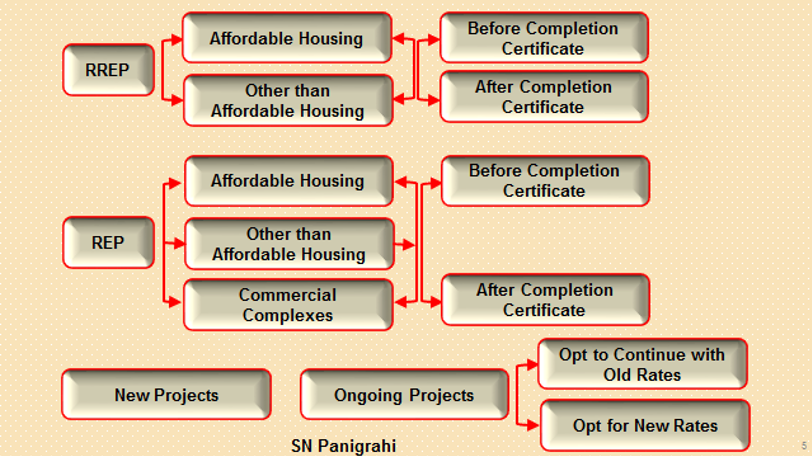

Multiple Schemes – Multiple Rates

The GST Rates applicable depending on multiple factors such as REP, RREP, Affordable Housing, Other than Affordable Housing, Commercial Complex, Completion Certificate Received or Not, New Project or Ongoing Project, Whether Builder has exercised the Option to Continue with Old Rate with ITC or New Rates with ITC etc,.

That means now for the similar flats, multiple rates are applicable depending on various conditions, which may lead to a lot of confusion, even experts in the field unable advice the buyers properly and builders do not disclose all the facts. When Confusion Prevails, Seeds of Corruptions Germinates. Unscrupulous builders may encash this opportunity mislead the public to collect higher rates.

Multiple Definitions / Abbreviations

In a 27 page Notification 03/2019-Central Tax (Rate),dt. 29-03-2019 many Terms are used and provided their definitions, meaning or explanations like apartment, project, affordable residential apartment, promoter, Real Estate Project (REP), Residential Real Estate Project (RREP), ongoing project, commencement certificate, development works, external development works, internal development works, competent authority, carpet area, Real Estate Regulatory Authority, Residential apartment, Commercial apartment, floor space index (FSI) etc and many more explanations, in stroke. One has to understand the relevance and its applicability to determine GST Rates.

Multiple Notifications for Changes in Real Estate

Following Notifications are issued amending various provisions as below

![Confusions Galore – Common Man @ Mercy.docx [Compatibility Mode] - Word (Product Activation Failed) 2019-05-11 13.50.55](https://www.consultease.com/wp-content/uploads/2019/05/Confusions-Galore-–-Common-Man-@-Mercy.docx-Compatibility-Mode-Word-Product-Activation-Failed-2019-05-11-13.50.55-1.png)

With Multiple Scenarios & Options and Multiple & Complex Calculations and Lengthy Descriptions, Definitions, Abbreviations, Notifications with Cross References, every one alike confused and unable to come to any conclusions & decisions.

Common Man – Buyer is Confused of Which Rate is Applicable on Residential Apartments as there are mix of offerings with New Rates of 1% & 5% or Old Rates of 8% & 12% or No GST applicable.

Builders / Developers Confused and unable decide on which option is better and its implications.

Consultants Confused unable advice the Clients properly

Officials are in great mess washing out their hands

Whether Reduction of Rates Benefit the Buyers?

The GST rate for residential houses was reduced to 1% from 8% for affordable housing and to 5% for other than affordable housing from the existing rate of 12% subject to some other conditions. The new rates are applicable from 1st April 2019. The new rates applicable are without availing benefit of the input tax credit which is the crux of the issue.

Though on the face of it seems GST rates are reduced, but since the Non-availability of Input Tax Credit, may compel the Builders to hike up the prices. The quantum of Input Tax Credit is not known. Figures in the books of accounts are mostly manipulated. For home-buyers, the rate change may not lead to a proportionate reduction in housing prices as the developer will not take on the burden of the input tax credit and it would be hence factored in the cost.

Despite clear provisions in the statute, mandating issue of Tax Invoice, Builders never issues such documents to the buyers. There is also no concept like Cost Plus. Generally, the rates are negotiated on inclusive price. The industry always operates on Demand & Supply basis making buyer “Bakry” (scamp goat).

Thus the question is Whether Reduction of Rates Benefit the Buyers?

Question remain as question without clear answer.

Builders too Undecided to Opt for the New Scheme

New Scheme with reduced GST rate comes with gambit of other conditions. Non- availment of ITC, mandatory 80% procurement from registered supplier, otherwise paying tax on reverse charge etc are very stringent conditions, the impact and implications of cost and compliance are still in conflicting mode.

Builders are mostly procuring most of their supplies from unregistered suppliers – sand, building materials, and other items even like steel & cement etc are sourced from unregistered for cost advantage or to avoid / evade tax. Mostly labour Contractors are unregistered. Un-accounted buying and consumption of Cement, Steel and other material are also very difficult to ascertain. Now the new conditions, mean more requirements of compliances and possibly a higher cost of inputs.

Undecided to Excise the Option of Continuing with Old Rates or Opt for New Rates, by 10th of May’2019, the extension of date come as a sigh of relief to the Developers. The Date is now Extended by another 10 Days ie upto 20th May’2019. Notification yet to be published. (God Knows still how many such extensions shall be granted)

Confusing Transitional Provisions of the Input Tax Credit

There are multiple methods of allocating input tax credit with complex calculations to provide pro-rata allocation based on credit proportionate to the amount on booking the flat and invoicing done for the booked flat. For mixed projects including commercial space, it would again depend on the proportionate carpet area.

All these calculations are mind boggling to just understand.

TDR, FSI, long term lease (premium) of Land by a Landowner to a Developer : Conditional Exemption

The supply of TDR, FSI, long term lease (premium) of land by a landowner to a developer shall be exempted from GST if the constructed flats are sold before the completion certificate is issued, and tax has been paid on them.

If they have been sold after the completion certificate has been issued, the exemption stands withdrawn, however, the withdrawal is limited to 1% of the value in case of affordable houses and 5% of value in case of other than affordable houses.

Builder shall be Liable to pay tax on TDR, FSI, long term lease (premium) of land under RCM in respect of Flats sold after Completion Certificate. This will add up tax expense, which may not get passed on to the buyers and have to be borne themselves, as GST is not applicable on completed properties.

However, in cases where this exemption applies, it could solve the cash-flow problem that is currently being faced.

Simplification to Complication

In the Name of Simplifying the Provisions and pass on benefits of reduction of rates, it’s now more Complicated the Matter with Bureaucratic Intelligence Forcefully Imposed on Public & the Builders who unable to Digest Complexities Still Struggling to make their Buying or Selling Decisions.

It is believed that new provisions are brought hurriedly just before elections to lure common man for voting benefits. Some Builders still hoping some Relief as the New Govt. forms in this Month end.

The Crux of the issue is Complexity

The Crux of the issue is Complexity & Complexity & Complexity.

It is well-established fact all over the world that Complexity & Compliance are negatively co-related. With increased Complexity, Laxity of Compliance develops and the “Dhekengeh” (Let’s see What Happens) attitude pervades and infuses into the minds of the Builders & Developers whose credentials are also very Doubtful. The “Dhekengeh” approach has a hidden flow of undue fortune.

With more Complexity and its Consequential increase in non-compliances, bureaucrats too celebrate making money.

In between the Festive Time of unscrupulous Builders and Corrupt Bureaucrats, the Common man suffers, paying higher amounts to Developers, defeating the very purpose of benefiting the Common man by bringing down the GST rates.

Construction and Infrastructural industry being most money spinners and major sources of funding to political parties, in the recent time they are dried and drained of most resources, finds this again an opportune propitious time to quench their money thrust this summer hot days to make nefarious, iniquitous and atrocious acts gracefully to enrich together with mastermind officials who coins new ideas from time and again very frequently to favour the fiendish trade.

Disclaimer: The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST & Foreign Trade Consultant, Practitioner, Corporate Trainer & Author

Can be reached @ snpanigrahi1963@gmail.com