Original Copy of GST AAR of Avantika Industries

Original Copy of GST AAR of Avantika Industries

In the GST AAR of Avantika Industries, the applicant has raised the query regarding the classification of the Springs of Iron and Steel for supply to the Railways. Following is the GST AAR of Avantika Industries:

Order:

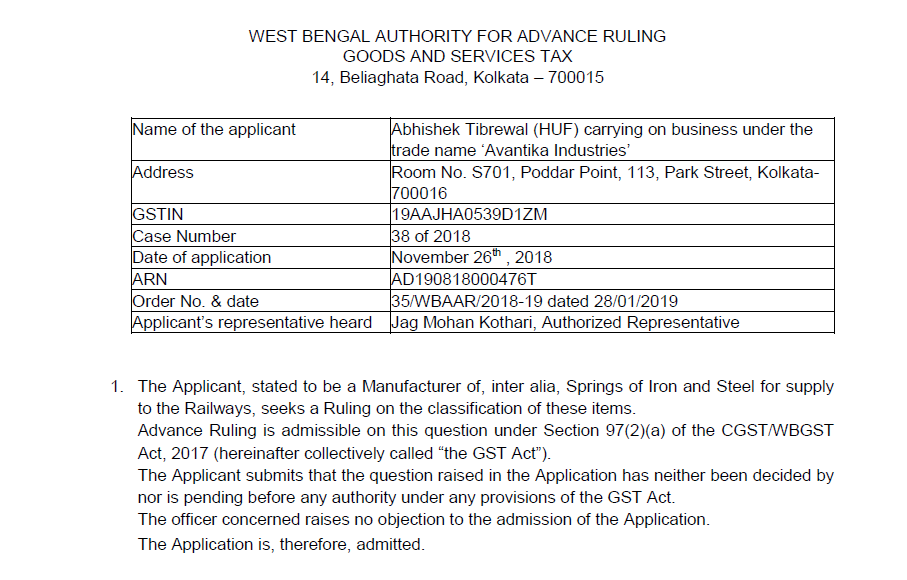

1. The Applicant stated to be a Manufacturer of, inter alia, Springs of Iron and Steel for supply to the Railways, seeks a Ruling on the classification of these items.

Advance Ruling is admissible on this question under Section 97(2)(a) of the CGST/WBGST Act, 2017 (hereinafter collectively called “the GST Act”).

The Applicant submits that the question raised in the Application has neither been decided by nor is pending before any authority under any provisions of the GST Act.

The officer concerned raises no objection to the admission of the Application.

The Application is, therefore, admitted.

2. The Applicant submits that all the items/parts supplied to the Railways are classified under HSN Code no. 8607 of Chapter 86 of First Schedule to the Customs Tariff Act, 1975, (hereinafter referred to as “the Tariff Act”), to which the GST Act is aligned for the purpose of classification [as per Explanations (iii) and (iv) to Notification No. 01/2017- CT (Rate) dated 28/06/2017].

Springs of Iron and Steel for Railways, however, are classified separately under HSN Code no.7320 of Chapter 73 of the Tariff Act.

The Applicant, therefore, has sought a clarification regarding appropriate classification of Springs of Iron and Steel supplied for use in Railways.

Download the GST AAR of Avantika Industries by clicking the below image:

3. The two Chapters under which classification of Springs of Iron and Steel for supply to Railways are being considered, fall under two different Sections of the Tariff Act. Section XV, which covers “Base Metals and Articles of Base Metal”, is relevant to items classified under Chapters 72 to 83, whereas Section XVII, which covers “Vehicles. Aircraft, Vessels and Associated Transport Equipment”, is relevant to items classified under Chapters 86 to 89.

Note 2 to Section XVII states that “parts” and “parts and accessories” do not apply to parts of general use as defined in Note 2 of Section XV, of base metal whether or not they are identifiable as for the goods of Section XVII.

Note 2(b) to Section XV defines the expression “parts of general use” to mean, ”springs and leaves for springs, of base metal, other than clocks or watch springs”

Hence, as per Note 2 to Section XVII, Springs of Iron and Steel are excluded from the parts and accessories that are identifiable as specifically for the goods of Section XVII, namely, in the present context, parts of Railways.

Again, Chapter Heading 8607 does not anywhere clearly classify Springs of Iron and Steel. It only refers to parts of the railway (such as bogies, Bissel-bogies, axels and wheels and parts thereof) in a general way; whereas, Chapter Heading 7320 clearly classifies springs of Iron and Steel for Railways. “Leaf-springs for Railways” are classified under Tariff Item No. 73201012 and “Coil-springs for Railways” are classified under Tariff Item No. 73209010.

In terms of Rule 3(a) of the Rules for Interpretation of Customs Tariff, as applicable to the GST Tariff, “the heading which provides the most specific description shall be preferred to headings providing a more general description”.

In the light of the above discussion, since Springs of Iron and Steel, are specifically classifiable under Chapter Heading 7320, the general description under Chapter Heading 8607 is not applicable. Springs of iron and steel for railways are classifiable under HSN Code no. 7320 and taxable @ 18% under Serial No. 234 of Schedule III of Notification No. 1/2017- CT (Rate) dated 28.06.2017 (also refer to Circular No. 30/4/2018 dated 25/01/2018, issued by CBIC for further clarification in this regard).

Ruling:

Springs of Iron and Steel for Railways are classifiable under HSN Code no. 7320 (taxable @ 18%) under Serial No. 234 of Schedule III of Notification No. 1/2017- CT (Rate) dated 28.06.2017.

This Ruling is valid subject to the provisions under Section 103(2) until and unless declared void under Section 104(1) of the GST Act.

Source: http://gstcouncil.gov.in/sites/default/files/ruling-new/WB_35_2018-19%20-AT(HUF)AI.pdf

Consultant