01

Sign Up with Your Phone Number

Just enter your number and log in with an OTP — no password needed.

India's fastest on-demand expert calls — talk to verified CAs, lawyers, and tax consultants instantly. Pay per minute, stop anytime.

Rated 4.9/5 from over 600 reviews

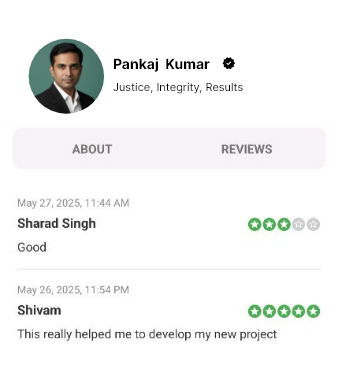

Talk to trusted experts who are verified and experienced in their respective fields.

Connect instantly via high-quality audio or video calls for private consultations.

No subscription fees. Pay only for the exact duration of your call.

Your conversations are encrypted and private. Your data is safe with us.

Read real reviews from other users to choose the right expert for your problem.

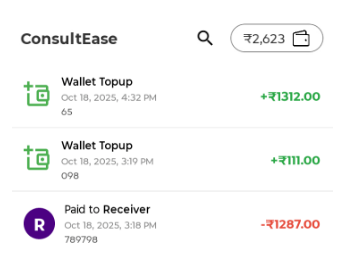

Businesses can enter their GST details and claim input tax credit on every consultation.

No long forms or ticket numbers. Just open the app, pick an expert and start talking.

Just enter your number and log in with an OTP — no password needed.

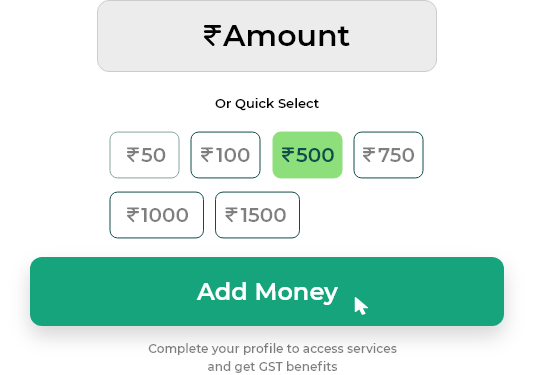

You control how much you spend — pay only for the minutes you talk.

Pick your problem area ( tax, business, property, finance, criminal or personal ) and see the experts who are online. Check their experience, rating and language.

Choose audio or video, talk directly, and get instant guidance. Businesses can claim GST credit on what they spend.

Get personal help without leaving home. Everyday problems need real answers — now you can get them from professionals who know how to help.

Expert advice that keeps your business safe. From registration to returns — talk to professionals who help you make smart business decisions.

WHY PEOPLE LOVE CONSULTEASE

People open Consultease when something is stuck – a notice, a dispute, a tough decision – and walk away knowing their next step.

You talk to a professional who explains what to do — right away.

A property expert tells you your options clearly.

Experts guide you from idea to registration.

A trusted professional listens and helps — privately.

FAQs

Got a tax, money, or legal question? Open the app and connect instantly with trusted professionals on a private audio or video call.